[ad_1]

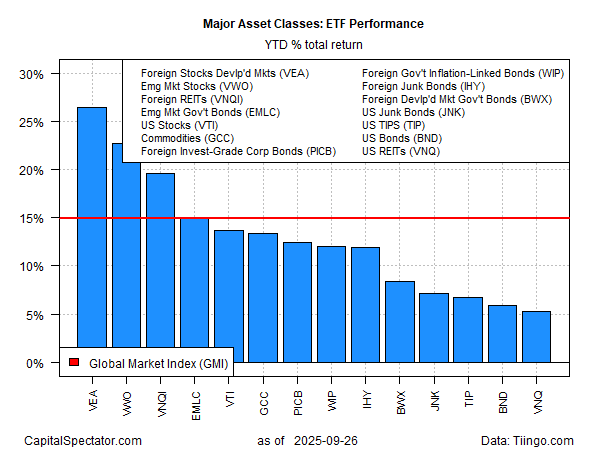

Decide an asset allocation. Any allocation. All the probabilities have been successful mixtures thus far in 2025. In consequence, the most-striking side of world markets because the third quarter winds down: across-the-board features proceed to prevail for the foremost asset courses, based mostly on a set of ETFs by Friday’s shut (Sep. 26).

Main the rally: overseas equities in developed markets ex-US (VEA), posting a robust 26.4% year-to-date acquire. In second place: shares in rising markets (VWO), that are up practically 23% in 2025. US shares (VTI), by comparsion, are a middling performer with a 13.6% rise this yr.

Each of the overseas equities funds, together with offshore property (VNQI), are outperforming the International Market Index (GMI), which is having an excellent yr of its personal. GMI is an unmanaged benchmark (maintained by CapitalSpectator.com) that holds all of the main asset courses (besides money) in market-value weights through ETFs and represents a aggressive benchmark for multi-asset-class portfolios.

The laggard this yr: US actual property funding trusts (VNQ); the fund us posting a comparatively modest 5.2% whole return for 2025.

If the ultimate print for this yr’s efficiency ended right here, the general outcomes would examine favorably with the historic document. Cue up the outlook for This fall, nonetheless, and issues begin to look difficult.

The rapid query: Will animal spirits be examined this week because the US authorities grapples with the potential of a shutdown beginning Oct. 1? President Trump is scheduled to fulfill with Congressional leaders at this time to maintain Washington open.

In the meantime, the group continues to be attempting to determine if tariff-related inflation is threat. Hanging within the stability: the bullish aura of late that springs from expectations that the Federal Reserve will proceed to chop rates of interest, because it did on Sep. 17.

Fed funds futures are nonetheless pricing in excessive odds that the central financial institution will ease coverage once more on the subsequent FOMC assembly on Oct. 29.

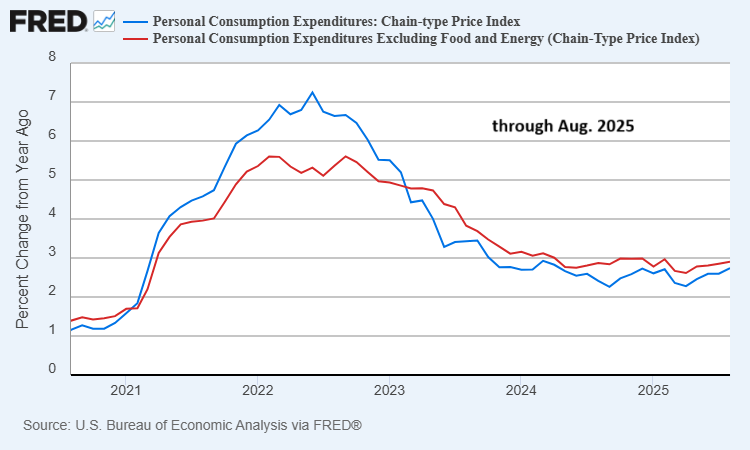

The outlook, nonetheless, could also be extra difficult than the futures market suggests. Notably, the Fed’s most popular measure of inflation – the private consumption expenditures value index – rose in August to 2.7% yr on yr, the very best since April 2024. Core PCE inflation was regular, albeit at the next 2.9% tempo.

Is that this an indication that tariffs-related inflation is beginning to spill over into the broader economic system? There’s nonetheless room for debate, which is why the September shopper value index report in just a few weeks will probably be a high-stakes launch to observe.

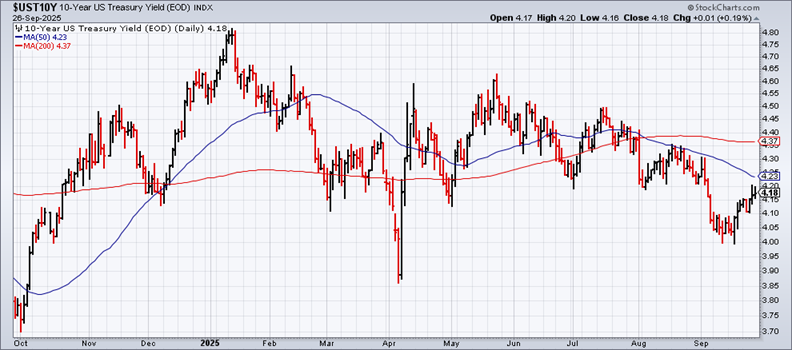

For now, markets are buying and selling on the idea that any pickup inflation will probably be gentle and temporary. For a real-time gauge that confirms or denies that assumption the US 10-year Treasury yield deserves shut consideration this week and past.

The benchmark fee is up 14 foundation factors because the central financial institution diminished its goal fee. That’s a trivial change and so the pop could possibly be noise. Alternatively, if the yield continues to development up, it’s going to get more durable to dismiss the bond market’s obvious issues on the inflation outlook.

[ad_2]