[ad_1]

The legendary investor Sir John Templeton famously warned: “The 4 most harmful phrases in investing are: ‘This time it’s totally different.’” The caveat is as soon as once more topical because the inventory market continues to rise regardless of excessive valuations. The rationale: synthetic intelligence has modified the sport.

The reasoning outlined in some corners is that AI will generate a hefty improve in financial productiveness, forging new markets and ushering a golden age of alternative and earnings. On that foundation, the case for a better market valuation is warranted.

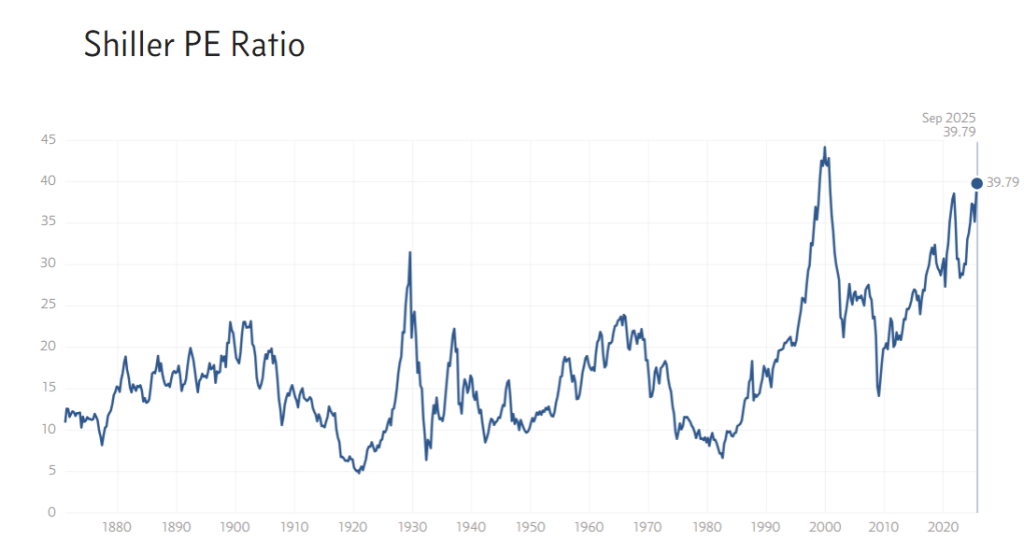

Fairness valuation is definitely lofty. The Shiller CAPE Ratio, for instance, is approaching a report excessive, which isn’t any trivial affair for information that reaches again to 1871.

Federal Reserve Chairman Powell weighed on this week, noting: “Fairness costs are pretty extremely valued.” Lest anybody thought he was issuing a macro warning, he added that “it’s not a time of elevated monetary stability threat.”

We’ve been right here earlier than, in fact, and it often resulted in tears for shares. Reversion to the imply doesn’t function like clockwork, however timber don’t develop to the sky both, or so historical past reminds. One of many extra notable situations of incorrectly arguing that regime change favored the bulls: Yale economist Irving Fisher’s ill-timed 1929 pronouncement that shares had reached a “completely excessive plateau.” A couple of days later, Wall Avenue suffered a devastating inventory market crash.

Let’s be clear: 2025 isn’t 1929, for a lot of causes, and so comparisons between every now and then are skinny, if not completely irrelevant. This time might be totally different, however it might additionally turn into one other bubble. No one is aware of. That’s price repeating: No one, which incorporates you and me, is aware of what’s going to occur. And so the query of whether or not the excessive valuation in shares is defensible, or not, is unquestionably germane.

Financial institution of America analysts, led by Savita Subramanian, argue that equities deserve a better premium. In a analysis word despatched to purchasers yesterday they write: “The index has modified considerably from the 80s, 90s and 2000s. Maybe we must always anchor to in the present day’s multiples as the brand new regular moderately than anticipating imply reversion to a bygone period.”

Unsurprisingly, such pondering is much from the consensus view. Ron Albahary, chief funding officer at LNW in Philadelphia, is among the many skeptics, telling Reuters yesterday:

“With the S&P pricing in 23-24 occasions anticipated earnings and expectations priced into that a number of of about 15% annualized earnings development over the subsequent 5 years, that sounds fairly wealthy to me. So not that we’re market timers in any respect, however the concept that individuals could be utilizing this, utilizing the Fed’s feedback, Powell’s feedback as only a cause to trim again slightly bit is smart to me.”

How ought to buyers navigate between the 21st century monetary model of Scylla and Charybdis? Within the historical Greek delusion, Odysseus should sail by slim, harmful waters and keep away from the monsters lurking beneath. The important thing takeaway: Generally there are few, if any, good choices, and so one of the best plan of action is to go for a lesser evil.

All of which means that the usual recommendation applies close to the inventory market. The long run, in any case, continues to be unsure, which suggests it’s well timed to refocus on what you possibly can management and handle. In case your US fairness allocation is nicely above goal weight, as an illustration, the case for rebalancing again to or close to the goal is compelling. Holding different asset courses and maybe proudly owning a tactical technique or two that may react to adjustments in market situations can also be prudent.

In the end, designing and managing a portfolio that’s custom-made in your specific set of expectations, threat tolerance, time horizon, and so on., are important sides of cash administration. One measurement by no means suits all, even when we’re getting into a brand new, golden age of AI.

Positive, you’ve heard this earlier than, and there’s a cause: Good recommendation transcends the pattern du jour. Or as I like to think about the usual portfolio recommendation: It’s the worst steerage accessible… besides compared with the whole lot else.

[ad_2]