Tej Parikh in FT inquires.

He presents progress charges of key indicators adopted by the NBER’s Enterprise Cycle Relationship Committee (BCDC). Under I present the identical indicators in ranges (the place I’ve changed the official NFP collection with the implied preliminary benchmark NFP utilizing Wells Fargo estimates).

Determine 1: Nonfarm Payroll – estimated preliminary benchmark revision (daring blue), NFP official (skinny blue), civilian employment with smoothed inhabitants controls (orange), industrial manufacturing (pink), private revenue excluding present transfers in Ch.2017$ (daring gentle inexperienced), manufacturing and commerce business gross sales in Ch.2017$ (black), and month-to-month GDP in Ch.2017$ (pink), all log normalized to 2025M04=0. Estimated preliminary benchmark is predicated on midpoint of Wells Fargo vary of downward revision. Supply: BLS by way of FRED, Federal Reserve, BEA 2025Q2 second launch, S&P World Market Insights (nee Macroeconomic Advisers, IHS Markit) (9/2/2025 launch), and creator’s calculations.

I normalize on April 2025 as a result of that’s the height in civilian employment, and there’s some proof that civilian employment peaks earlier than NFP in actual time, simply earlier than recessions.

It’s clear that nonfarm payroll employment progress has slowed to a crawl, a slowdown extra pronounced if one used the official collection. We now have the official preliminary benchmark revision on Tuesday (9/9), and the Philadelphia Fed early benchmark on 9/19.

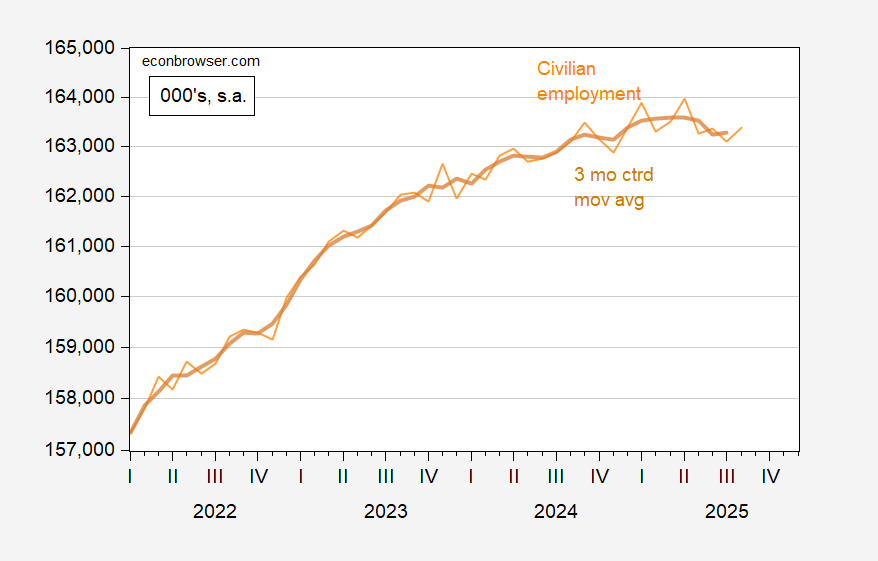

The evolution of civilian employment is proven under.

Determine 2: Civilian employment, smoothed inhabitants controls experimental collection (orange), and three month centered shifting common (darkish orange), in 000’s, s.a. Supply: BLS and creator’s calculations.

For the reason that family survey primarily based employment collection is extra risky than the NFP, it is smart to take a shifting common. This transformation confirms that civilian employment is previous latest peak…