[ad_1]

Along with deaths and destruction in Ukraine, the Russian invasion introduced a number of vital shocks to the worldwide economic system. Along with the geopolitical penalties of the struggle, reinforcing the downward development in commerce globalization and monetary integration, new rounds of disruptions in provide chains and better commodity costs have already led to downward revisions in financial progress projections, accompanied by greater inflation.

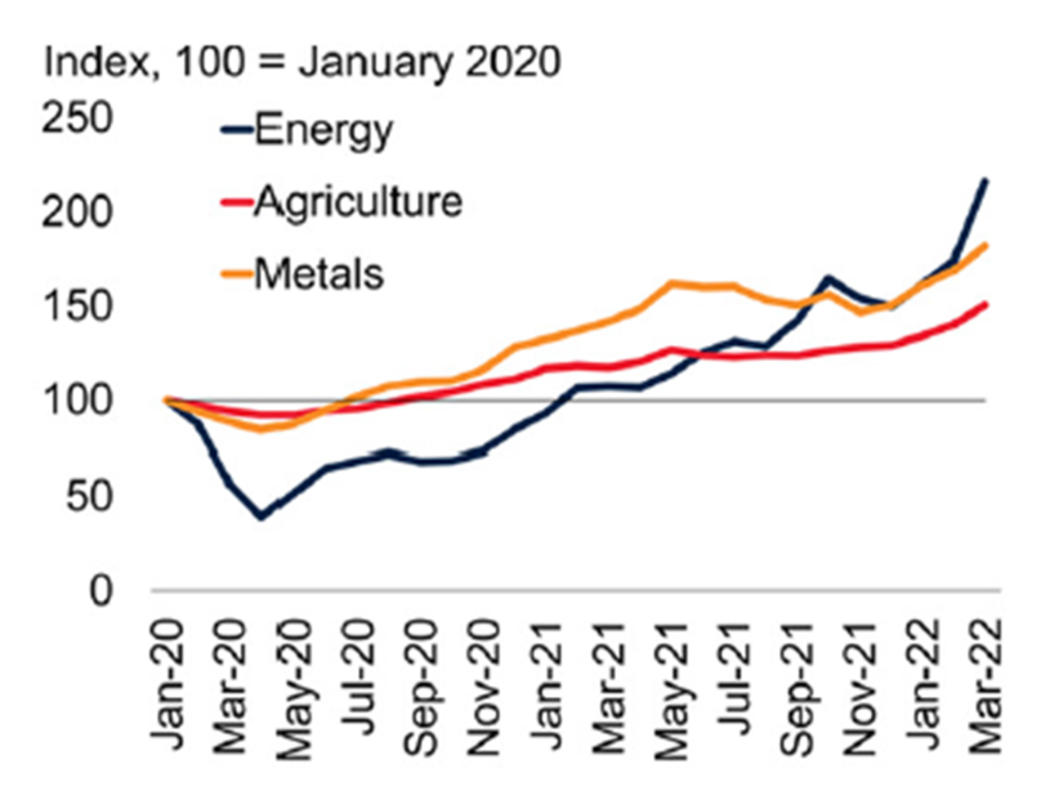

Commodity costs stabilized in April. Nevertheless, the earlier commodity value shock, intensifying tendencies which were current since mid-2020, have already led to considerably greater value ranges in 2022, and will stay there within the medium time period, in keeping with the World Financial institution’s Commodity Markets Outlook report launched on April 26 (Determine 1).

Determine 1 – Commodity Costs

Supply: World Financial institution (2022). Commodity Markets Outlook, April.

The outlook for commodity markets will rely upon the size of the struggle in Ukraine, sanctions on Russia and the severity of disruptions to commodity flows. The 2 nations are vital suppliers of power, fertilizers, some forms of grains and metals. Russia is the world’s largest exporter of pure gasoline, nickel, and wheat, whereas Ukraine is the most important exporter of sunflower oil. Not coincidentally, these commodities skilled significantly sharp will increase after the beginning of the struggle in Ukraine.

A number of nations – together with america, Canada, and the UK – have already introduced bans or phasing out Russian oil imports, whereas personal consumers have additionally pledged to chop purchases of Russian oil. What about provide alternate options? One downside is the actual fact noticed in a examine by the Federal Reserve of Dallas, in keeping with which manufacturing capability restrictions in OPEC+ member nations are stopping them from even fulfilling their quotas assigned by the group.

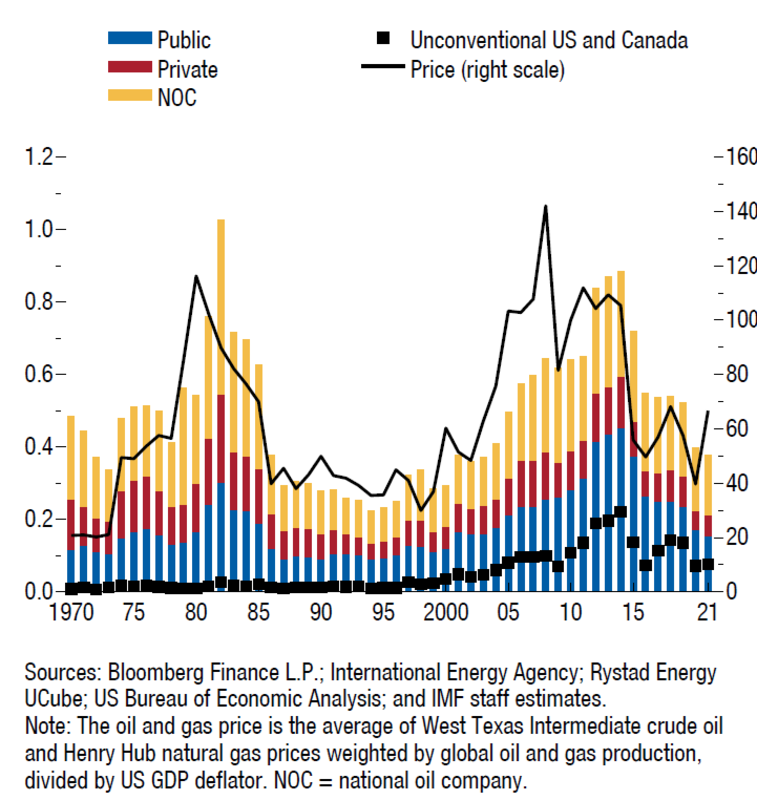

A particular function of the IMF’s World Financial Outlook report, launched on April 19, recommended that the anticipation of falling demand for fossil fuels – due amongst different issues to the power transition – has diminished international funding in oil and gasoline by about 20% within the final 3 or 4 months. After spiking in the course of the “shale revolution”, international upstream oil and gasoline funding peaked at 0.9% of world GDP in 2014, falling to lower than 0.5% of world GDP in 2019, and additional down in the course of the pandemic (Determine 2).

Determine 2 – Oil and Gasoline Funding as Share of World GDP (%, US$ a barrel)

The worth of Brent crude reached a mean of $116 a barrel in March, one thing not seen since 2013. The World Financial institution forecasts common oil costs to common $100 a barrel this yr, earlier than declining easily to US$92 a barrel in 2023.

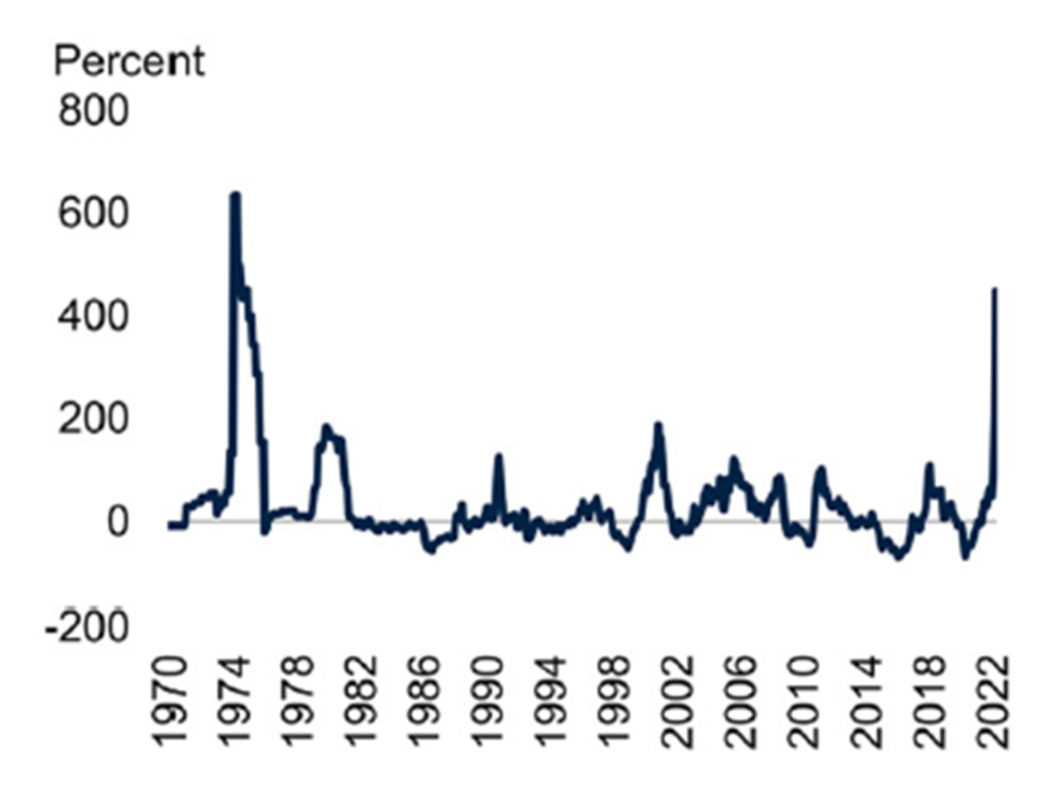

In March, European pure gasoline costs had been virtually seven occasions greater than one yr earlier than. Coal costs in a number of components of the world have additionally tripled on account of anticipated disruptions to Russian pure gasoline and coal exports. The post-pandemic demand restoration and restricted provide circumstances had been already having an upward impact, however the brand new jumps made the rise in power costs within the final two years the most important within the final fifty years, because the oil shock in 1973 (Determine 3).

Determine 3 – Vitality Value Development

Supply: World Financial institution (2022). Commodity Markets Outlook, April.

The permanence of costs at greater ranges will likely be bolstered by two components. First, as value will increase are occurring throughout all fuels, there may be not a lot scope to switch essentially the most affected power commodities with different fossil fuels. Second, power commodities have a robust affect on the costs of others. For instance, pure gasoline costs have already pushed up fertilizer costs, placing stress on agricultural costs.

Within the case of meals, commerce disruptions and excessive enter prices have additionally had a major impression. The UN meals value index positioned them on the highest degree because the starting of its monitoring 60 years in the past. It isn’t simply wheat costs due to the struggle. Frustration with wheat and soybean crops in South America has additionally negatively affected their international availability.

Greater costs and dangers of fertilizer shortages are a supply of concern relating to meals costs subsequent yr. Meals safety and doable social upheavals have turn out to be central points in components of the world, together with the poorest and food-importing nations in Africa, Center East, and Asia.

Costs of some metals additionally reached unprecedented ranges in March, resulting from dangers of provide disruption, whereas inventories had been at traditionally low ranges. Ukraine and Russia are substantial sources of palladium and platinum, each of that are used within the manufacture of catalytic converters for the car trade. Platinum, copper, and nickel are essential inputs for electrical car batteries. Ukraine can be the supply of fifty% of the world’s neon gasoline, used for lasers used to fabricate semiconductor chips.

The struggle in Ukraine has been the primary driver of aluminum and nickel value actions, whereas excessive power costs have in flip affected zinc. These metals are key inputs in renewable applied sciences equivalent to photo voltaic panels and wind generators. Because of this, additional value will increase or interruptions within the provide of those metals might make the power transition dearer.

Within the quick time period, the macroeconomic impacts of the commodity value shock will differ amongst rising economies, relying on whether or not they’re exporters or importers. In Latin America, as an example, there’s a new inflationary spike, whereas, within the case of exporters, GDPs, commerce balances and public sector accounts have a tendency to learn. Brazil had its progress projection barely elevated by the IMF to 0.8% and 1.3%, respectively, in 2022 and 2023.

Strictly talking, the struggle in Ukraine and the shock of power commodity costs haven’t been favorable to the power transition, as seen within the race for coal and new sources of oil. This after the pandemic, not but over, as will likely be seen within the international penalties of the lockdowns in China, ensuing from its quest for zero-Covid, within the coming weeks. For the current mixture of pandemic plague, struggle, and deaths to not assume apocalyptical proportions, we should forestall local weather change led to by additional delays within the power transition.

Otaviano Canuto, primarily based in Washington, D.C, is a senior fellow on the Coverage Heart for the New South, a professorial lecturer of worldwide affairs on the Elliott Faculty of Worldwide Affairs – George Washington College, a nonresident senior fellow at Brookings Establishment, a professor affiliate at UM6P, and principal at Heart for Macroeconomics and Growth. He’s a former vice-president and a former government director on the World Financial institution, a former government director on the Worldwide Financial Fund and a former vice-president on the Inter-American Growth Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics at College of São Paulo and College of Campinas, Brazil.

[ad_2]