[ad_1]

The Monetary Instances’ lead story is Prime US financiers sound alarm on lending requirements. As we’ll clarify, this piece, which takes the tone “Errors have been made however we don’t see catastrophic outcomes in retailer,” follows a sequence of warnings about US fairness market dangers.

Yours really doesn’t give monetary recommendation and doesn’t like doing one thing that is perhaps mistaken for market prognosticating. Nonetheless, the proof is powerful that many markets are priced in order that the chance/return tradeoff of an extended place appears awfully doubtful.

However the present state of affairs is vastly harder to judge than the runup to the 2008 disaster. There, the exposures have been in dangerous US mortgage loans and associated derivatives. The knowledge on the underlying loans was excessive; for example, yours really picked aside a granular evaluation by CoreLogic of subprime mortgage resets which claimed nothing horrible would happen.1 Our remodeling instructed the reverse, which proved to be right.

Not solely do those that need to make sense of what’s going no longer solely lack that degree of transparency, however as well as many extra monetary asset sorts are implicated, and there are additionally much more worldwide elements to contemplate. For example, we identified that in 1987, specialists have been fixated on the Japanese actual property and inventory market bubbles and didn’t have a US crash on their bingo playing cards. The basics in Europe are horrible and getting worse, but the euro and European inventory markets are peppy, apparently as a consequence of undue optimism that army Keynisianism will ship blissful financial outcomes….whilst attempting to implement these priorities has led to the dearth of a authorities in France and stunningly low approval rankings for nationwide leaders in Germany, the UK, and Italy.

An extra obstacle to prognosis now in comparison with the pre-Lehman interval is the dearth of an econoblogosphere. There, an lively group, together with Tanta at Offended Bear, Ed Harrison,Felix Salmon, Barry Ritholtz, Nouriel Roubini, Paul Krugman, “Unbiased Accountant,” Steve Waldman and plenty of others posted about what we have been seeing and debated what it meant. There’s no data sharing/sanity checking group now.

Identical to some key factors of the seemingly very properly coated 1987 disaster truly not being properly understood, that it true of some not-distant debt implosions too. The financial savings and mortgage disaster masked a second meltdown in leveraged buyouts. One colleague, answerable for exercises at GE, one of many larger US lenders (the monster suckers had been overseas banks) received two convention rooms for his labors. One he known as Triage, the opposite, Don Quixote. That secondary downdraft elevated harm to banks, main Greenspan to engineer a really steep yield curve in order to help them in rebuilding their stability sheets.

However the larger level of those seeming digressions is that historic analogies might miss key factors, once more even earlier than attending to what number of plates there are within the air now: the AI/tech bubble (which additionally implicates junk lending to AI gamers), the not-well-understood dangers within the personal debt market, the additional layer of leverage in personal fairness due to lending in opposition to the funds themselves through “subscription traces of credit score,” political fractures in most Western states, financial wobbles which will spill into markets from Europe, China (which is present process critical deflationary pressures), and Trump kinetic and commerce struggle mongering. Not a reasonably image!

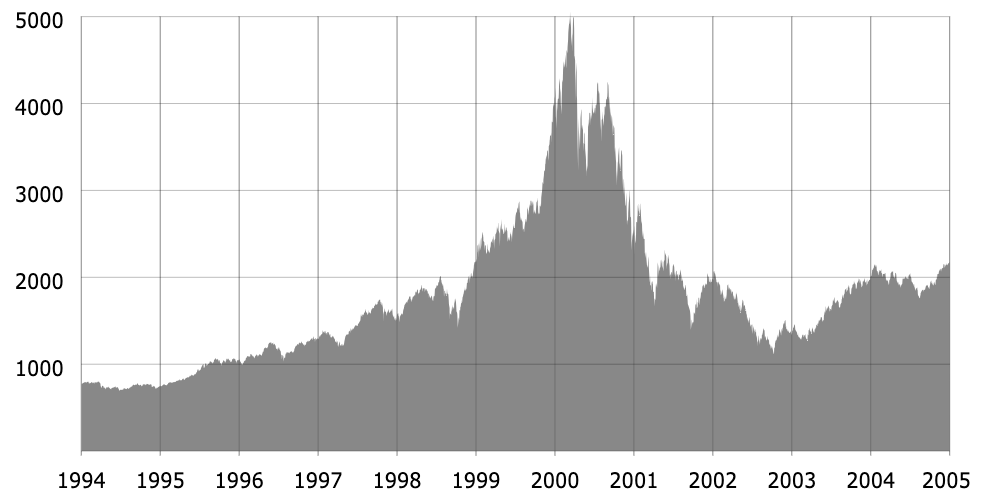

Regardless of how uncommon it’s for monetary agency leaders to difficulty what positive appear to be statements in opposition to curiosity, which might be learn as a sign that unhealthy outcomes are nigh, the prototypical sample for a bull market is for the mania to persist till because the wags put it, the final bear has thrown within the towel. We identified to readers that regardless of the dot-com bubble wanting frothy from a minimum of Greenspan’s “irrational exuberance” comment of late 1996, the much more richly priced market in 2000 has a last three months blowout (see the transfer from 4,000 to five,000 and even the velocity of the rise from 3,000). From Shares to Commerce:

So remembering that it isn’t over till the fats woman sings, let’s first flip to the contemporary monetary high brass warnings within the Monetary Instances about debt:

Prime US financiers have warned of an erosion in lending requirements after credit score markets have been shaken by the collapse of First Manufacturers Group and Tricolor Holdings.

Apollo World Administration chief govt Marc Rowan mentioned the unravelling of the 2 companies adopted years by which lenders had sought out riskier debtors….

Final month’s failure of First Manufacturers and subprime auto lender Tricolor has reverberated throughout credit score markets and left traders comparable to Blackstone and PGIM, in addition to main banks together with Jefferies, nursing heavy losses.

It has additionally prompted additional scrutiny of the personal capital business and the dearth of transparency round debtors, which are typically extremely levered with debt.

“In a few of these extra levered credit, there’s been a willingness to chop corners,” Rowan instructed the Monetary Instances Personal Capital Summit in London.

Each Rowan and Blackstone president Jonathan Grey pointed the finger at banks for having amassed publicity to First Manufacturers and Tricolor, however mentioned the collapses weren’t indicators of a systemic difficulty. “What’s attention-grabbing is each of these have been bank-led processes,” Grey instructed the identical FT convention, rejecting “100 per cent” the “concept that this was a canary within the coal mine” or a systemic downside….

Banks and personal capital corporations have been at odds in recent times as companies have more and more turned to non-public credit score for his or her borrowing wants. Conventional lenders have labelled the shift regulatory arbitrage and complained that non-bank monetary establishments are too flippantly regulated.

However First Manufacturers and Tricolor have uncovered how each side are intertwined by complicated monetary constructions that may obfuscate who holds the underwriting danger, particularly as financial institution lenders purpose to take care of their market share.

JPMorgan Chase chief govt Jamie Dimon echoed a number of the issues on Tuesday because the financial institution reported sturdy earnings that have been marred by a $170mn hit from Tricolor’s collapse.

“My antenna goes up when issues like that occur. I in all probability shouldn’t say this however whenever you see one cockroach there are in all probability extra,” he mentioned. “There clearly was, for my part, fraud concerned in a bunch of these items, however that doesn’t imply we will’t enhance our procedures,” he added, acknowledging that the Tricolor publicity “was not our best second”.

Once more, yours really is old school. First Manufacturers was engaged in what is named factoring, as in getting loans in opposition to receivables. That could be a staple of the garment business. I might regard that in a longtime being an indication of both a need to realize a excessive degree of leverage or misery, that means heightened scrutiny was warranted, However First Manufacturers had the great fortune to go on its borrowing and as Dimon alludes, fraud spree when lending requirements have been gentle and “cov lite” as in offers with lower-than-normal lender protections, have been the norm.

It seems that First Manufacturers double-pledged collateral, right here its receivables. That’s against the law. For example, a few years in the past, Ralph Esmirian, a extremely revered determine in New York’s diamond business, offered collateral he had used to get loans and in addition double pledged collateral after shopping for the storied jewellery retailer Fred Leighton. Esmirian was sentenced to six years in Federal jail. See this part of a Wall Road Journal account, Behind the Collapse of an Auto-Elements Big: a $2 Billion Gap and a Mysterious CEO:

[Patrick] James’s firm, First Manufacturers Group, has filed for chapter, acknowledging that greater than $2 billion is unaccounted for. Newly appointed administrators are probing irregularities within the firm’s financing preparations, and the Justice Division has opened an inquiry, in line with individuals aware of the matter.

First Manufacturers, of which James is chief govt officer and sole fairness proprietor, borrowed greater than $10 billion from some large names regardless of a historical past of lawsuits from enterprise companions who had alleged that James made misrepresentations in his convoluted financing preparations. Main banks together with UBS Group and Jefferies Monetary Group are uncovered.

Unbeknown to most, the corporate raised billions by off-balance-sheet financing, particularly by a type of borrowing in opposition to cash it’s owed by clients comparable to AutoZone….

James’s firm, First Manufacturers Group, has filed for chapter, acknowledging that greater than $2 billion is unaccounted for. Newly appointed administrators are probing irregularities within the firm’s financing preparations, and the Justice Division has opened an inquiry, in line with individuals aware of the matter.

First Manufacturers, of which James is chief govt officer and sole fairness proprietor, borrowed greater than $10 billion from some large names regardless of a historical past of lawsuits from enterprise companions who had alleged that James made misrepresentations in his convoluted financing preparations. Main banks together with UBS Group and Jefferies Monetary Group are uncovered.

Unbeknown to most, the corporate raised billions by off-balance-sheet financing, particularly by a type of borrowing in opposition to cash it’s owed by clients comparable to AutoZone.

In concept, Jeffries, which is essentially the most uncovered, to the tune of $715 million Level Bonita fund, might take the complete loss. However there seemingly will likely be, as occurred in the course of the monetary disaster,2 calls for from traders who participated within the fund, for Jeffries to make them complete. That will entail a wholly completely different degree of harm.

Now to the inventory market alerts, once more courtesy the pink paper:

The leaders of Goldman Sachs, JPMorgan Chase and Citi warned traders that investor exuberance risked driving a recent-run up in monetary markets into bubble territory.

Goldman chief govt David Solomon mentioned: “There isn’t a query that there’s a good quantity of investor exuberance in the meanwhile, with US fairness markets persistently hitting report highs during the last a number of months.”

“A lot of this has been fuelled by an amazing quantity of funding in [artificial intelligence] infrastructure, which has pushed important capital formation. However as college students of historical past, we all know that following durations of broad-based pleasure round new applied sciences, there’ll in the end be a divergence the place some ventures thrive and others falter.”

JPMorgan boss Jamie Dimon mentioned: “We’ve numerous belongings on the market which appear to be they’re coming into bubble territory. That doesn’t imply they don’t have 20 per cent to go. It’s only one extra explanation for concern.”

Citi CEO Jane Fraser mentioned the worldwide financial system has “proved extra resilient than many anticipated”, thanks partly to investments in AI.

“That mentioned, there are pockets of valuation frothiness out there so I hope self-discipline stays,” she mentioned.

And the associated debt publicity shouldn’t be trivial. From Bloomberg on October 7:

The quantity of debt tied to synthetic intelligence has ballooned to $1.2 trillion, making it the most important phase within the investment-grade market, in line with JPMorgan… AI firms now make up 14% of the high-grade market from 11.5% in 2020, surpassing US banks, the most important sector on the JPMorgan US Liquid Index (JULI) index at 11.7%, JPMorgan analysts together with Nathaniel Rosenbaum and Erica Spear wrote… The analysts recognized 75 firms throughout tech, utilities and capital items sectors which might be carefully tied to AI, together with Oracle Corp., Apple Inc. and Duke Power Corp. Many of those corporations are prolific debt issuers and within the case of tech, they’re money wealthy with very low web debt. The cohort trades at 74 bps, 10 bps tighter than the broader JULI index, they mentioned

Take into account that funding grade equals, or is meant to equal, fairly safe. Yours really has additionally learn mentions of AI-related junk debt however has but to see any mixture estimate.

However even for those who think about inventory market froth alone, this bubble is as unhealthy and even by some measures worse than the dot-com affair. And we aren’t alone in considering issues might get much more frenzied. Hoisted from feedback:

FWIW Mark Spitznagel of Universa Investments [engages in Nassim Nicholas Taleb style hedging and has Taleb as an advisor] is asking for a blow off high after which a like 80% crash within the inventory market and thinks we’re presently in the midst of that rally. IIRC he mentioned we, “might see” SPX round 8000 earlier than the huge crash, so possibly 20% larger from here- clearly predicting actual numbers is a idiot’s errand however nonetheless… so if that’s what involves go then getting in now might be profitable quick time period however probably devastating for those who don’t get out in time, so fairly excessive danger…. I feel Spitznagel in contrast what is occurring proper now to the start of 1929, euphoric excessive forward, then huge crash. Good luck man, in all probability don’t let FOMO lizard mind overtake rational mind and make you place all of your chips on the desk at a time of irrational euphoria although, at all times be able the place your gonna have $ to purchase stuff when its low-cost. I consider Spitznagel thinks there are lagging results from the Fed elevating charges so rapidly and for thus lengthy which might be going to be the catalyst that pops the bubble.

Even when the bubble pops at roughly the place we’re, the knock-on actual financial system impact could be appreciable:

⚠️That is really INSANE:

US households now personal a RECORD 52% of their monetary belongings in equities.

This share has greater than DOUBLED for the reason that Nice Monetary Disaster and surpassed the 2000 Dot-Com Bubble by ~5 factors.

The maintain simply 15% in money and 14% in debt belongings. pic.twitter.com/6DRmtxYSze

— World Markets Investor (@GlobalMktObserv) October 13, 2025

These holdings are concentrated in wealthier households, natch, which as we’ve got chronicled for the previous 2 years plus have been the principle drive of what passes for development within the US. In order that group battening down on spending would have an excellent larger impact than regular occasions.

We’ve been mentioning deflation for a while, since it’s clear China is experiencing it and is to a point already exporting it. Its home actual property costs are nonetheless falling. The federal government has admitted it has manner an excessive amount of capability in giant, essential sectors, above all electrical automobiles, resulting in what was as soon as known as ruinous worth competitors. It’s within the strategy of attempting to rationalize them, however the same marketing campaign within the mid-teens took years to resolve the issue. And it’s over my pay grade, however specialists say that the present overcapacity will likely be more durable to treatment. China a minimum of presently ramping up exports to Southeast Asia is an indication of weak point, not energy. A few of it’s supposed re-export to the US; a few of it’s channel stuffing. We’re already in borderline deflation right here (indicators of pay charges for informal labor falling; no inflation; official forecasts just for 0.5% to 1.0%).

Other than the deflationary impact of an enormous inventory market crash, one other vector is tariffs. I don’t know Lacy Hunt however his reasoning is persuasive. He contends that the preliminary impact of tariffs will likely be to extend inflation, whilst companies additionally attempt to soak up a number of the prices (provided that revenue share of GDP has been at report highs in recent times, there’s some room for larger companies to eat the tariff bills). However the second set of results, as occurred as a consequence of Smoot-Hawley, is that buyers and companies lower spending, and that the impact of the discount within the deficit is to scale back capital inflows, which has a further deflationary impact. Hunt argues central banks wrong-footed what to do then and are seemingly to take action once more:

“The one different time this ever occurred was between 1929 & 1930”

Lacy Hunt sees a deflationary debt spiral unfolding now brought on by tariffs & lack of liquidity in worldwide markets.

That is how the Federal Reserve & President Hoover deliberately collapsed the system in 1929 https://t.co/5D925EiJ3l pic.twitter.com/KJVOn5vrop

— Financelot (@FinanceLancelot) October 9, 2025

None of that is cheery, however with a light-weight like Bessent at Treasury and Trump extra involved with dominating the Fed than having sound coverage, anticipating good emergency responses if issues begin going south is wishful considering. Keep alert.

____

1 No joke. From the March 2007 put up, quoting the Wall Road Journal:

[Author] Christopher Cagan, director of analysis on the real-estate-information concern [CoreLogic] primarily based in Santa Ana, Calif., mentioned these foreclosures are prone to happen over six to seven years and received’t be sufficient to break the nationwide financial system.

2 This occurred with the gross sales of bank card receivables, which have been by their express phrases non-recourse to the vendor. However then the patrons successfully mentioned, “Dream if we’ll purchase one other deal for those who don’t present some kind of restitution.”

[ad_2]