[ad_1]

This opinion piece was submitted to the Investing Information Community (INN) by Darren Brady Nelson, who’s an exterior contributor. INN believes it could be of curiosity to readers and has copy edited the fabric to make sure adherence to the corporate’s model information; nevertheless, INN doesn’t assure the accuracy or thoroughness of the knowledge reported by exterior contributors. The opinions expressed by exterior contributors don’t mirror the opinions of INN and don’t represent funding recommendation. All readers are inspired to carry out their very own due diligence.

By John Newell

It’s fascinating how investor psychology adjustments relying on the place we’re within the cycle. Gold and silver are buying and selling close to document highs, main producers are producing extra free money stream than at any time in historical past, and but the dominant query I hear is: “When ought to we promote?”

That’s a good query, when you consider we’re late within the sport. However what if the sport has simply begun?

When Amazon broke out to new all-time highs in ~2015, nobody was asking when to promote or that the RSI was prolonged. Traders have been making an attempt to know how excessive it might go. Now, with gold and silver quietly constructing momentum and mining shares beginning to outperform, it’s value asking whether or not we’re coming into an analogous long-duration progress section.

While you step again and have a look at the long-term charts, the image adjustments fully. The patterns, the ratios and the basics all level to the identical conclusion: we’re probably within the early innings of a brand new metals bull market, one that might final the higher a part of a decade. As Mr. Ross Beatty, chairman of Equinox Gold (TSX:EQX,NYSEAMERICAN:EQX), mentioned in a current interview, “the actual hazard that buyers are going through is promoting to quickly.”

The basics: Why gold and silver are rising

The macro backdrop has not often been this supportive for treasured metals and the businesses that mine them.

1. Financial coverage and world debt

Governments are trapped in a cycle of deficit spending. Whilst central banks discuss “tightening,” actual charges stay effectively beneath long-term averages. Debt ranges are so excessive that sustained excessive rates of interest would threat destabilizing total economies. That actuality ensures a coverage bias towards simple cash, and that’s traditionally bullish for gold.

2. Forex debasement

Since 2020, the worldwide cash provide has exploded. The buying energy of fiat currencies continues to erode as governments print to cowl deficits. Traders and central banks alike are turning to tangible shops of worth and shopping for gold. Gold stays the anchor asset in a world of floating currencies.

3. Geopolitical instability

Battle, sanctions, commerce fragmentation and the weaponization of economic methods have made world markets far much less predictable. Gold thrives in such environments as a result of it exists outdoors the management of any single authorities or central financial institution.

4. Industrial demand for silver

Silver’s twin position, as each a financial steel and an industrial materials, makes it distinctive. The accelerating demand for photo voltaic power, electronics and electrical automobiles has added a wholly new supply of structural demand. In each main bull cycle, silver ultimately outperforms gold, and that cycle seems to be organising once more.

5. Mining corporations are depleting their very own companies

Day-after-day a miner operates, it consumes a finite useful resource. As manufacturing continues, reserves decline, forcing corporations to both purchase or uncover new deposits to outlive. With document earnings and money stream, the majors now face a alternative: substitute ounces by means of acquisition or face a long-term manufacturing cliff. That dynamic creates a strong incentive to spend money on juniors, the invention pipeline of the trade.

The technical case: Charts inform the actual story

The ratio and index charts reveal what worth motion alone can’t: we’re seeing early-stage breakouts throughout a number of timeframes.

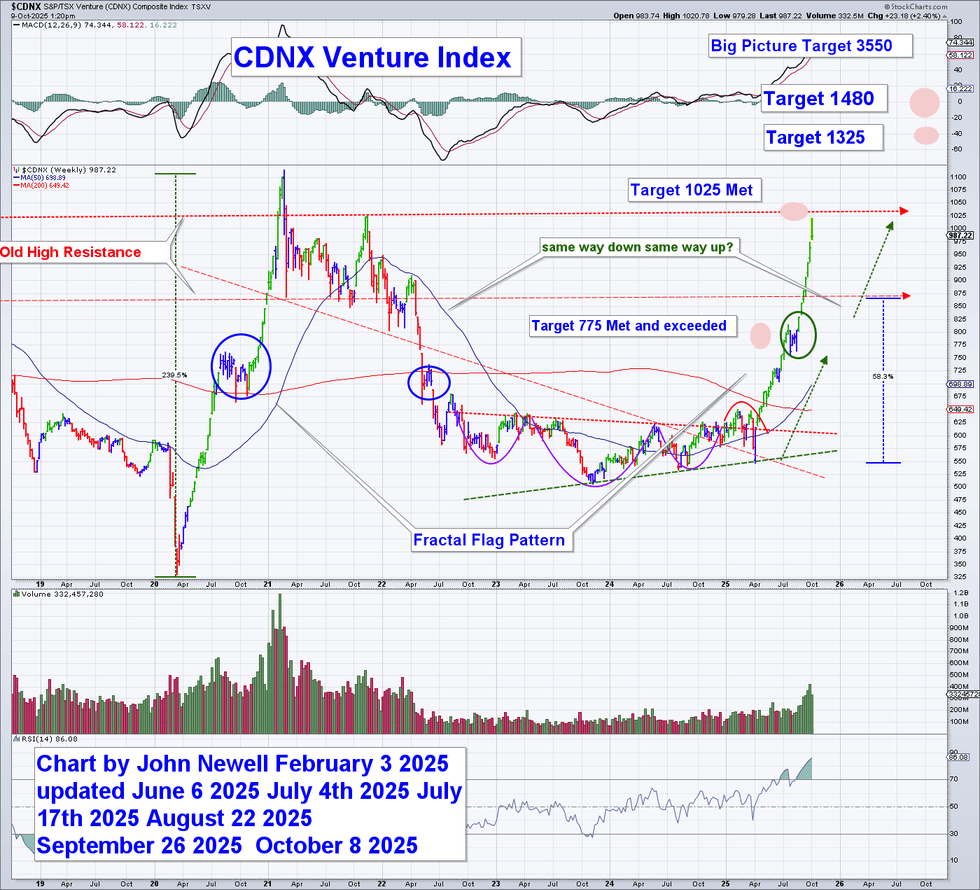

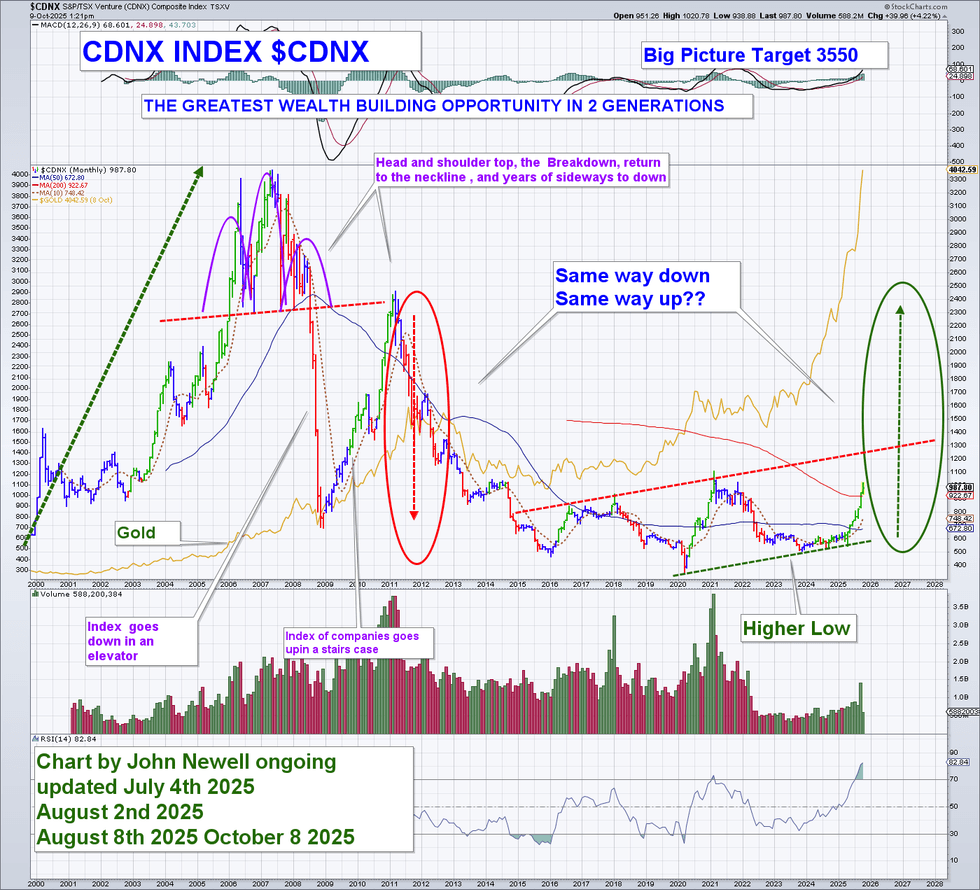

1. CDNX Enterprise Index: The junior renaissance

The TSX Enterprise (CDNX) has spent years in a deep base, mirroring the early levels of previous bull cycles. It has now damaged by means of main resistance ranges, assembly and exceeding its first two targets. Traditionally, as soon as the index clears these ranges, it alerts renewed urge for food for high-risk, high-reward discovery tales.

In prior cycles, this setup led to multi-year advances the place the CDNX outperformed each gold and the broader fairness markets by broad margins.

2. CDNX vs. gold: A deep low cost ready to revert

The Enterprise Index as soon as traded at a premium to gold. Immediately, it trades at a steep low cost. If historical past is any information, this imbalance gained’t final. As capital rotates again into the exploration stage, that relationship might normalize, driving the index, and the businesses inside it, considerably larger.

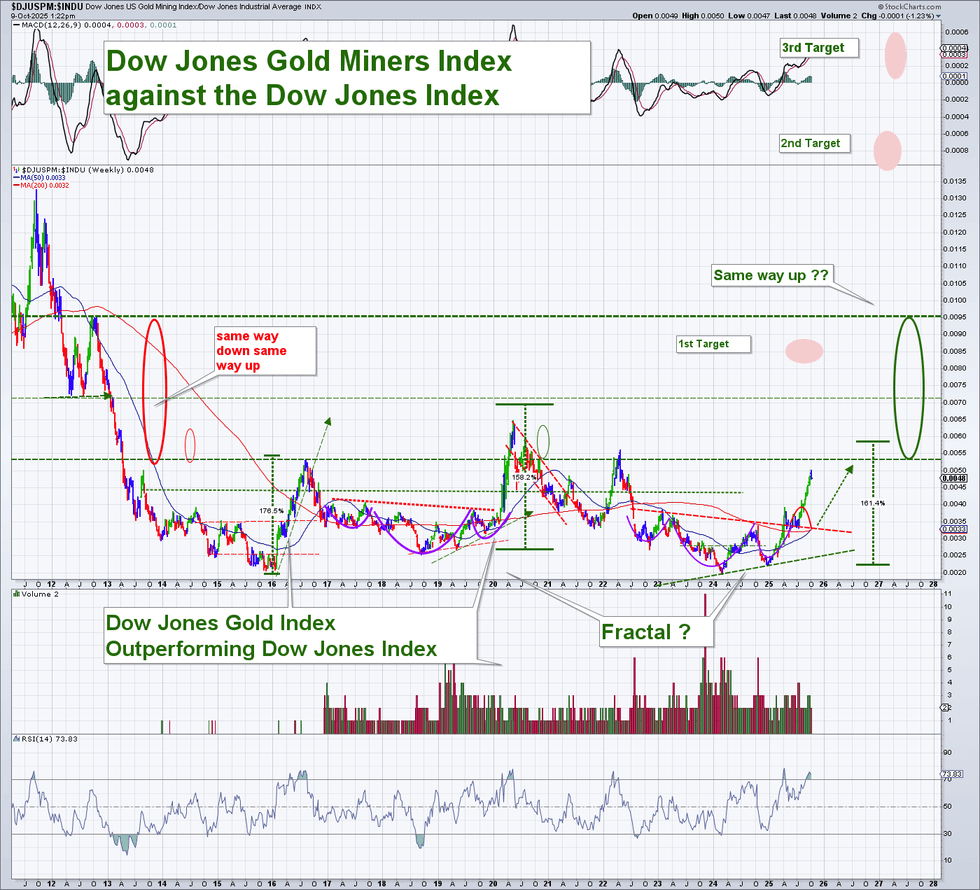

3. Dow Jones Gold Miners Index vs. Dow Jones Industrial Common

This ratio has turned decisively larger for the primary time in years. It exhibits that miners are starting to outperform the overall market, a key hallmark of each previous bull market in treasured metals. The fractal nature of the sample suggests the transfer could possibly be substantial, with targets projecting a number of legs larger.

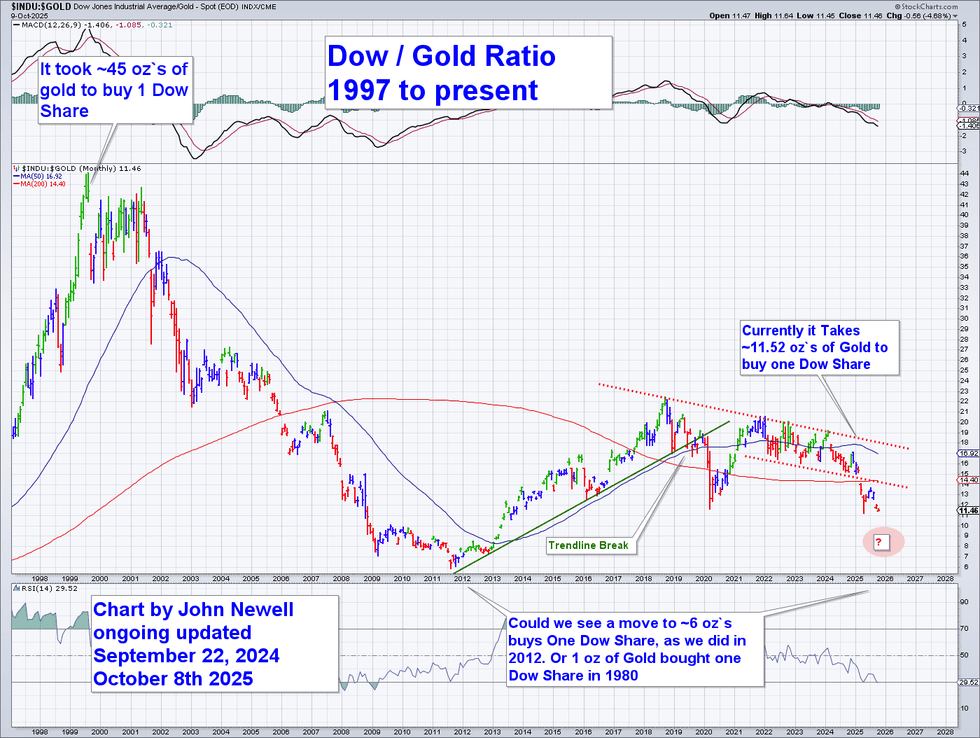

4. Dow/gold ratio: A decade-long turning level

It at present takes about 11.5 ounces of gold to purchase one Dow share. At gold’s 1980 peak, that quantity was 1:1. In 2012, it dropped to about 6:1. The present stage sits close to the midpoint of the long-term vary, not close to a prime. If this ratio revisits earlier lows, gold might commerce far larger even when the Dow merely holds its floor.

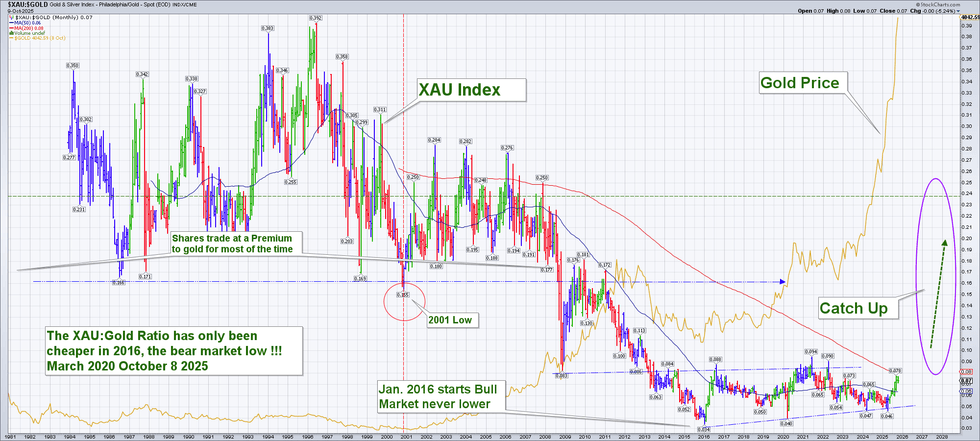

5. XAU/gold ratio: The catch-up commerce

The XAU Index (a basket of gold, silver and copper corporations) stays close to historic lows relative to gold itself. Traditionally, when this ratio reverses, the transfer is sharp and highly effective as equities “catch up” to the steel. That catch-up section is the place the most important positive aspects are inclined to happen.

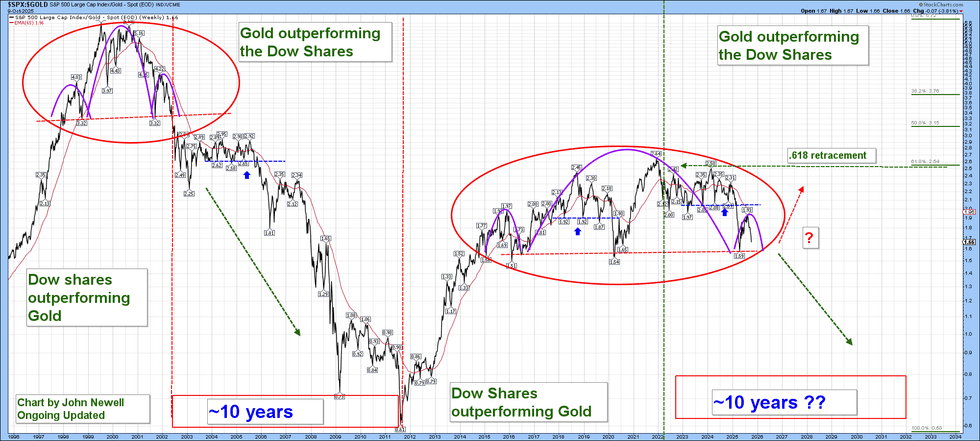

6. The S&P 500 vs. gold: A ten yr rotation cycle

The long-term ratio between the S&P 500 and gold reveals a hanging rhythm: roughly each decade, management flips between paper property and laborious property.

Within the late Nineteen Nineties by means of 2000, gold started outperforming shares for almost ten years. Then from 2012 to 2022, the pendulum swung again as equities dominated. Now, because the chart exhibits, that cycle seems to be reversing as soon as once more.

The sample is obvious, a broad topping construction has accomplished, marked by a .618 Fibonacci retracement that always defines the exhaustion level of an equity-dominant section. If the sample repeats, we could possibly be coming into one other 10-year interval the place gold outperforms the S&P 500.

For buyers, this rotation isn’t about short-term trades, it’s about understanding the secular shift underway. In previous cycles, those that acknowledged the flip early captured extraordinary positive aspects as capital flowed out of overvalued equities and into undervalued tangible property like gold, silver and the mining shares that leverage them.

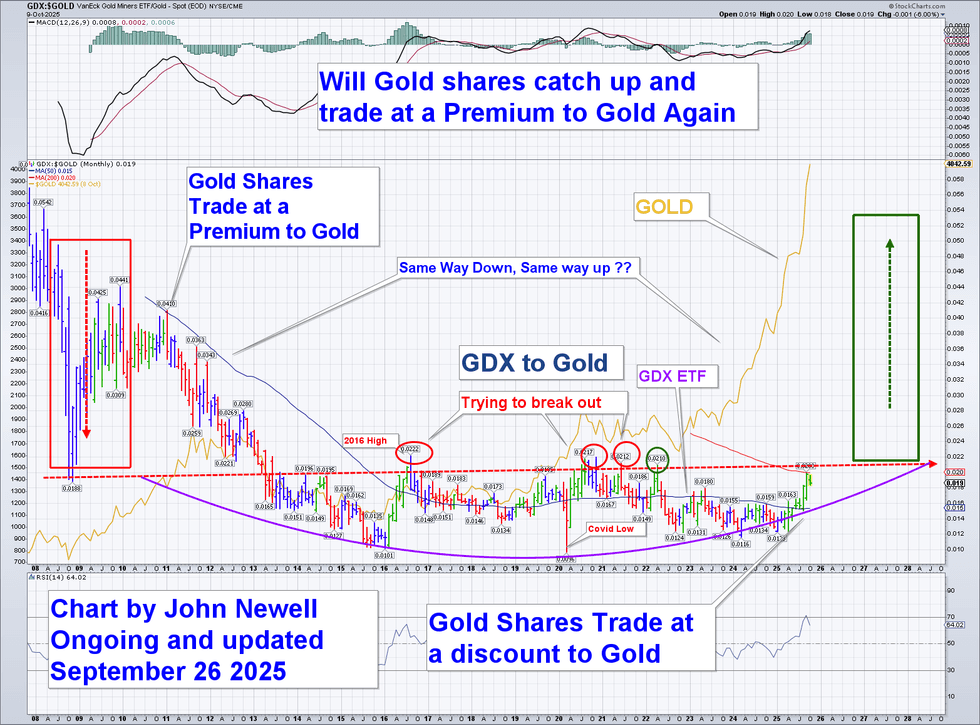

7. GDX to gold: The senior miners’ breakout

The GDX-to-gold ratio compares the efficiency of gold mining shares to the worth of gold itself. Traditionally, gold equities have traded at a premium to gold as a result of they provide leverage to rising steel costs.

Immediately, they commerce at a deep low cost. The ratio has primarily based for almost a decade and is now urgent in opposition to key resistance ranges.

The query is easy: Will gold shares catch up and commerce at a premium once more?

Every time this ratio has turned larger, resembling in 2001 and 2016, it marked the start of a strong multi-year rally for miners. The symmetry is hanging “identical approach down, identical approach up”. GDX is now trying to interrupt out from that base, suggesting that institutional cash is rotating again into the sector.

If this breakout holds, it might affirm the beginning of the “catch-up section,” the place gold equities lastly start to outperform the steel as soon as once more.

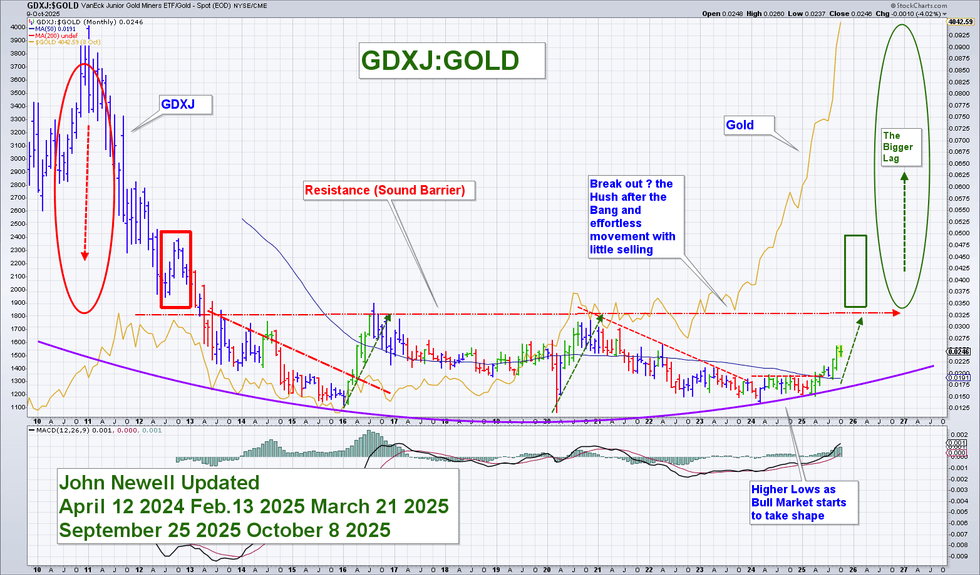

8. GDXJ to gold: The juniors poised to guide

The GDXJ-to-gold ratio tracks junior miners versus gold. This chart captures the heartbeat of the speculative cycle.

After years of decline and an extended basing sample, GDXJ has begun making larger lows, a traditional signal {that a} bull market is taking form beneath the floor. The ratio is now approaching its “sound barrier”, a resistance line that, as soon as cleared, has traditionally unleashed sharp, low quantity strikes larger.

I name this the “hush after the bang”, that easy motion when sellers are exhausted and consumers start to chase.

The setup seems just like the early 2000s, simply earlier than juniors exploded in worth as capital flowed down the ladder from producers to explorers.

If this breakout confirms, it would mark the transition from disbelief to recognition, the second when retail and institutional buyers lastly return to the exploration commerce.

9. The US greenback: Dropping energy on the finish of a 15 to 16 yr cycle

The ultimate piece of the puzzle is the US greenback itself. Each main gold bull market has coincided with a multi-year decline within the US greenback, and the chart means that one other one could also be beginning now.

During the last 5 a long time, the greenback has moved in 15 to 16 yr cycles, peaking roughly each decade and a half earlier than present process vital multi-year declines. The peaks in 1985, 2001 and 2017 all led to main rallies in gold.

We now look like finishing one other related cycle. The chart exhibits a repeating fractal sample, robust greenback rallies ending in exhaustion, adopted by years of gradual weak point. The latest cycle has lasted about 15 years, inserting us proper on schedule for the subsequent main flip decrease.

If this sample repeats, the implications are clear: the greenback could possibly be coming into a interval of long-term structural weak point, which traditionally corresponds with highly effective strikes larger in gold, silver and mining equities.

It’s not nearly short-term fluctuations; it’s concerning the finish of a foreign money cycle. When the world’s reserve foreign money weakens, capital seeks refuge in laborious property. That’s when gold doesn’t simply outperform, it re-prices the complete system.

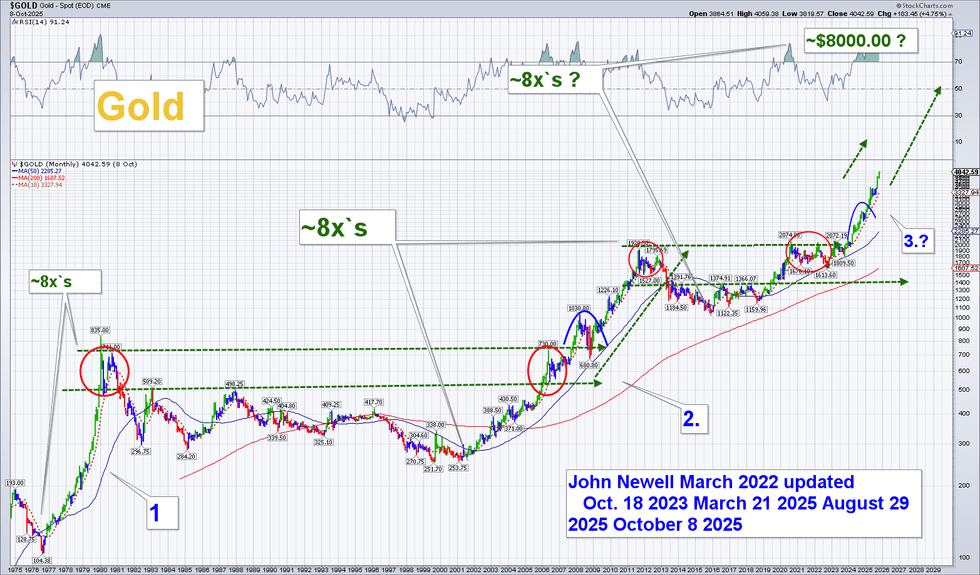

10. Gold’s massive image: A believable path to US$8,000

The long-term month-to-month gold chart gives historic perspective. Because the Seventies, each main bull cycle in gold has produced roughly an eightfold enhance from its base.The Seventies bull noticed gold rise from ~$100 to ~$850. The 2001–2011 cycle took it from ~$250 to ~$1,900, once more, about eight occasions larger.

Utilizing the identical logic, the present transfer that started round $1,000 in 2015 initiatives to roughly $8,000 per ounce over the approaching years. Which will sound daring, however it’s merely the historic rhythm of the steel, repeating throughout a long time of inflation, financial enlargement and geopolitical stress.

If we’re certainly in the beginning of a 10-year cycle the place gold outperforms shares and currencies, $8,000 just isn’t an outlier. It’s the logical extension of the identical long-term fractal sample that has performed out twice earlier than.

Why timing issues

Markets are pushed by psychology as a lot as fundamentals. The perfect alternatives not often seem comfy.

After years of neglect, the mining sector has turn out to be deeply undervalued. Institutional possession is low, sentiment is muted and but the backdrop might hardly be extra favorable. These are the circumstances which have preceded each main bull run within the useful resource area.

The technical breakouts we’re now seeing, throughout the CDNX, the Dow/Gold ratio and the miners vs. market indices, sign a profound shift in capital flows. It’s not nearly gold hitting new highs; it’s about the place the subsequent wave of cash goes as soon as buyers understand the sector’s relative undervaluation.

In the meantime, the biggest mining corporations are making document earnings and document free money flows however all the time face declining reserves. They’ll purchase progress and /or merge. They usually’ll probably purchase it from the juniors, the businesses that may nonetheless create ounces within the floor.

For buyers, this implies timing isn’t about calling the highest; it’s about recognizing when a brand new multi-year cycle is beginning. The proof suggests it already has.

Conclusion: The early innings of a generational bull market

Each main gold bull market begins in disbelief. The early levels are quiet, outlined by sluggish accumulation and skepticism. Then momentum builds, ratios flip and capital begins to stream.

Immediately, each the basics and the technicals level in the identical path. Gold and silver are coming into a section of renewed energy, whereas the equities that mine them are nonetheless priced for a bear market that ended way back.

Traders ready for a prime could also be lacking the beginning of one thing a lot greater. If previous is prologue, this could possibly be the start of a brand new chapter the place the mining sector leads world markets for the primary time in a long time.

About John Newell

John Newell is the president and CEO of Golden Sky Minerals (TSXV:AUEN) and serves as president and CEO of Thunderbird Minerals (TSXV:BIRD). A seasoned market skilled, John has been writing about treasured metals and exploration corporations since 2001. He has labored as a portfolio supervisor and treasured metals fund supervisor and now takes a management position within the exploration sector, the place his firm not too long ago accomplished an earn-in three way partnership with a serious mining agency. John blends technical evaluation with on-the-ground expertise to offer a singular perspective on the evolving treasured metals markets.

Remember to observe us @INN_Resource for real-time updates!

[ad_2]