[ad_1]

Coverage Heart for the New South

In its Might 15th assembly, the Federal Open Market Committee (FOMC) of the U.S. Federal Reserve (Fed) lifted its benchmark coverage fee by 0.75% to 1.50%–1.75%, probably the most important improve since 1994. The central financial institution additionally signaled an extra improve of 0.75% forward. FOMC members additionally raised the median projection for the Fed funds fee to a variety between 3.25% and three.50% subsequent 12 months.

Along with hikes in primary rates of interest, liquidity circumstances within the US financial system can even be affected by the shrinking of the Fed’s steadiness sheet beginning this month. The “quantitative easing” (QE) that resumed vigorously in March 2020, in response to the monetary shock initially of the pandemic, will now give option to a “quantitative tightening” (QT).

How complementary – or substitute – will likely be these actions in rates of interest and steadiness sheet downsizing? What are their probably penalties on capital flows to rising markets (EM)?

From QE to QT

QE corresponds to large-scale asset purchases by central banks, sometimes of long-term authorities debt but in addition personal belongings, equivalent to company debt or asset-backed securities. QE has primarily occurred in unconventional circumstances, when short-term nominal rates of interest are meager, zero, and even destructive. It has been carried out during times of disaster to offer liquidity and keep a clean market functioning.

The Financial institution of Japan started a QE in 2001. Then, throughout and after the 2008 international monetary disaster, QE turned far more widespread, with central banks within the U.S., the U.Ok., the euro space, Switzerland, and Sweden becoming a member of the band. QE aligns with ahead steering and destructive nominal rates of interest as an unconventional financial coverage motion. .

Typical financial coverage corresponds to establishing the goal for the short-term nominal rate of interest, with that rate of interest goal relying on observations concerning combination financial efficiency. Sometimes, the central financial institution’s nominal rate of interest goal is anticipated to go up if inflation exceeds the central financial institution’s inflation goal and to be lowered if combination output – as an illustration, actual gross home product (GDP) – comes down under what’s deemed to be the financial system’s potential.

Nevertheless, limits to how low the short-term nominal rate of interest can go could seem on the best way. Central banks within the euro space, Sweden, Denmark, and Switzerland have gone right down to destructive short-term rates of interest. Within the U.S., this decrease sure has been taken as zero, as was the case within the U.S. on the finish of 2008, in the course of the monetary disaster, when the Fed resorted to unconventional financial coverage, together with a collection of QE applications afterward.

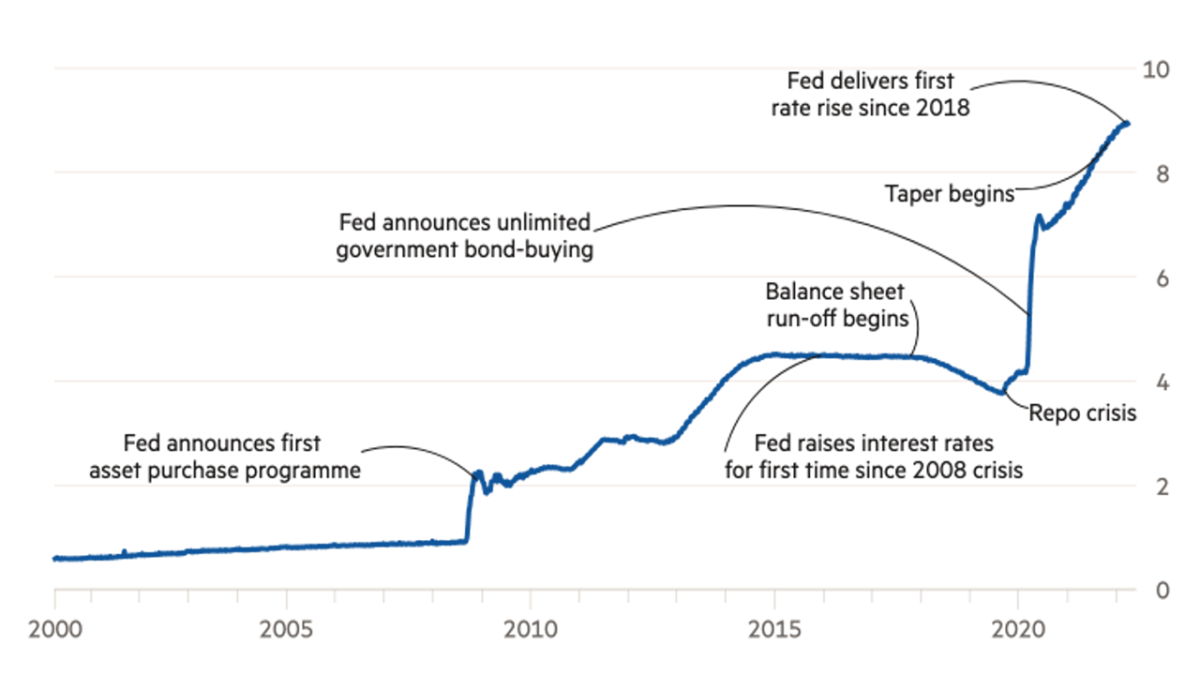

Determine 1 reveals the evolution of complete belongings held by the Fed since then. The magnitude of QE applications will be gauged by noticing that the full Fed belongings elevated from 6.0% of U.S. GDP within the fourth quarter of 2007 to 23.5% of GDP within the first quarter of 2017. It reached round US$ 4.5 trillion on the finish of the Q3 in October 2014, after which the extent was maintained because the Fed reinvested (or rolled over) bonds as they matured.

Then, in September 2017, the Fed introduced an upcoming shift to QT, when it could scale back its steadiness sheet not by promoting bonds however by slowing the reinvestment of maturing bonds. After barely shrinking its steadiness sheet, QE returned in September 2019 as a response to the liquidity disaster occurring within the markets of in a single day repurchase agreements (or “repos”). These are short-term loans between monetary establishments. They skilled a sudden and surprising spike in rates of interest, and the Fed moved in to keep away from contamination of the remainder of the monetary system.

The pandemic monetary shock led to a strong response by the Fed. Between March 2020 and March 2022, the Fed purchased month-to-month US$80 billion of Treasury bonds and US$40 billion of mortgage-backed securities. Asset holdings within the Fed’s portfolio greater than doubled on this interval, from US$3.9 trillion initially of the interval to US$8.5 trillion in Might of this 12 months, similar to 18% and 35% of GDP.

Determine 1 – Property Held by the Federal Reserve (US$ trillions)

In the meantime, the typical maturity of the belongings within the Fed’s portfolio turned a lot increased than earlier than the worldwide monetary disaster, with an elevated share of long-maturity Treasury securities and mortgage-backed securities. In all these QE applications carried out worldwide throughout and after the worldwide monetary disaster, central banks appeared primarily centered on how the sort and amount of asset purchases would have an effect on monetary market circumstances and, finally, inflation and combination financial exercise—however doing it as a direct intervention on longer-term belongings. Through the pandemic disaster, some EM carried out some QE (Canuto, 2020 a).

As proven in Determine 2, U.S. QE applications began at moments when U.S. 10-year authorities bond yields descended drastically. By shopping for medium- and long-term belongings, the Fed aimed to lift their costs and yields. The counterpart of QE acquisitions is bigger internet reserves within the personal sector.

Determine 2 – U.S. 10-12 months Authorities Bond Yield and QE

Now, given the present overheated labor market circumstances and inflation nicely above the goal, the discount within the Fed’s steadiness sheet will correspond to a gradual reversal of that counterpart in liquidity as a reinforcement of rate of interest hikes.

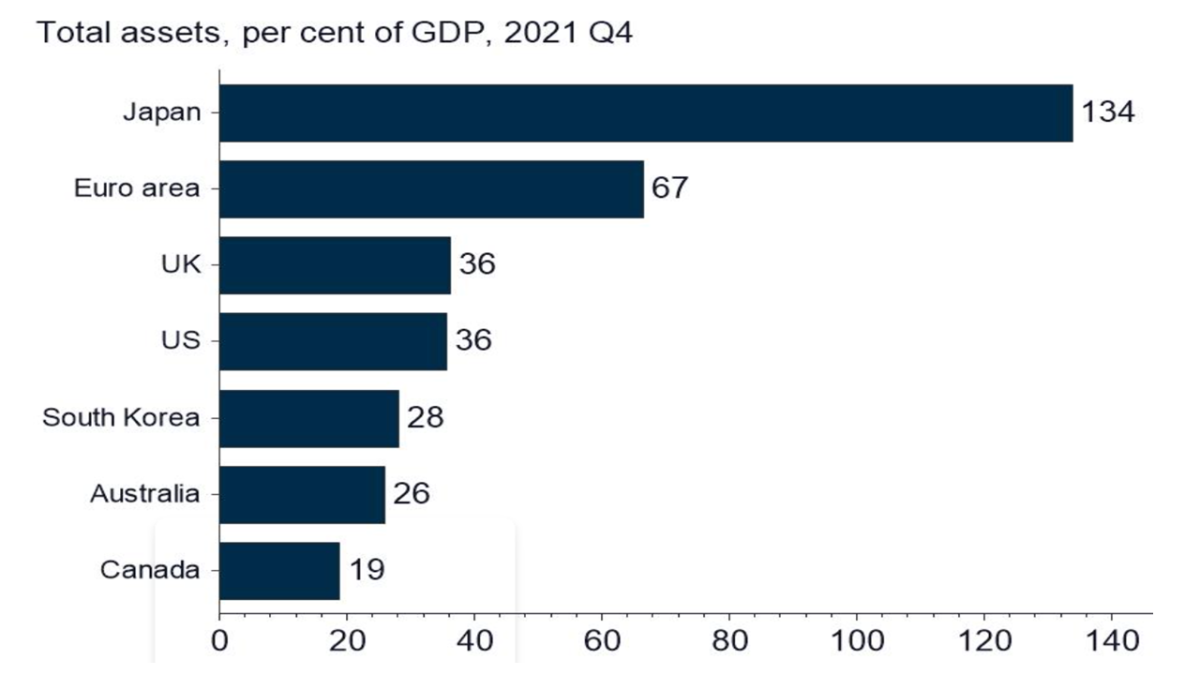

Determine 3 gives a glimpse of the place the a number of QE applications carried out by main developed economies have led their central banks’ steadiness sheets. Central financial institution steadiness sheets of rising economies additionally went up on account of drying out home liquidity impacts of their accumulation of foreign-exchange reserves (Canuto and Cavallari, 2017).

Determine 3 – Central Financial institution Steadiness Sheets of Superior Economies

For the U.S. Fed QT, it’s going to suffice that these funds from maturing securities usually are not reinvested. The Fed set a month-to-month cap of US$60 billion of Treasury bonds and US$35 billion of mortgage bonds for steadiness sheet shrinkage beginning in September of this 12 months, beginning this month till August with half these quantities.

Underneath that plan, the Fed’s steadiness sheet is anticipated to shrink by round $520 billion this 12 months. It is going to nonetheless enter 2023 nicely above the 20% of nominal GDP the place it was earlier than the pandemic. However the fee of lower of US$ 1.1 trillion a 12 months beginning in September can have a corresponding decline within the liquidity – financial institution reserves and deposits – accessible within the financial system.

How complementary – or substitute – can rate of interest and central financial institution steadiness sheet insurance policies be?

How complementary will base fee will increase and QT be regarding longer rates of interest that have an effect on selections underlying combination demand (personal sector funding and consumption) and thus inflationary stabilization? QE and QT are seen to are likely to have a direct impression on longer rates of interest. In precept, they converge with coverage fee selections on short-term rates of interest to handle combination demand, even although totally different channels.

In spite of everything, the coverage fee and steadiness sheet instruments affect the financial system primarily by means of their results on the medium- and longer-term rates of interest that drive financial exercise. Coverage fee actions and communications have an effect on the price of short-term borrowing and expectations concerning the path of short-term rates of interest. Steadiness sheet insurance policies primarily affect the time period premiums embedded in medium- to longer-term yields by altering the availability—present and anticipated—of longer-term securities held by the general public.

As they’re complementary, the 2 instruments may also be taken as substitutes by way of their means to have an effect on medium- and longer-term rates of interest, employment, and inflation when decrease bounds on coverage charges usually are not binding. Put it one other means: might a central financial institution economize on rate of interest hikes (decreases) through the use of QT (QE)?

Crawley et al (2022), from the Federal Reserve, have just lately offered an train of translating steadiness sheet reductions by way of equal will increase within the path of the federal funds fee that might result in comparable macroeconomic outcomes:

“(…) a one-time everlasting discount within the Federal Reserve’s holdings of 10-year equal Treasury securities equal to 1 % of nominal GDP raises the time period premium on a 10-year Treasury safety by about 10 foundation factors, all else equal. Within the mannequin, this quantity of coverage tightening can be achieved by elevating the typical anticipated path of the federal funds fee over the approaching decade by about 10 foundation factors. Collectively, these relationships present a easy rule of thumb for the substitutability between steadiness sheet reductions and coverage fee hikes within the mannequin when the financial system is away from the ELB [Effective Lower Bound]. Nevertheless (…) the interpretation of greenback quantities of steadiness sheet reductions into equal coverage fee hikes depends upon the evolution of the scale and maturity composition of the steadiness sheet. (…) there’s important uncertainty concerning the transmission of steadiness sheet and coverage fee actions to medium- to longer-term rates of interest, in addition to the transmission of the ensuing yield curve actions to the broader financial system (…) Moreover, there’s some proof that will increase in longer-term rates of interest could have smaller results on macroeconomic outcomes once they originate from elevated time period premiums than once they originate from elevated expectations of the coverage fee.”

By their simulations, shrinking the scale of the Fed steadiness sheet by roughly US$ 2.5 trillion over the following few years is equal to lifting the federal funds fee by simply over half a share level.

QE (QT) are anticipated to impression the yield curve flatter (steeper) because the central financial institution purchases (sells, or not purchase) long-term belongings. Finally, all of it depends upon how personal brokers use alerts to challenge future central financial institution selections on rates of interest. In 2013, all it took was a reference by then-president Ben Bernanke {that a} discount within the tempo of QE underway was being thought of, for a taper tantrum to happen, with markets anticipating a pointy rise in primary rates of interest, with instant results on asset costs. In flip, between the start and the tip of the primary QT – mild and transient – in 2017, the premiums on 10-year Treasury bonds fell.

This time, nonetheless, it’s attainable to imagine that the Fed desires the devices working in earnest in the identical course of containing demand. Doubts concern the tempo and extent of the tightening, each about base charges and the scale of the Fed’s steadiness sheet on the finish of QT. In spite of everything, every thing will rely upon how employment and inflation behave alongside the best way, contemplating the inevitable lag between financial coverage selections and their results on the financial system. Nevertheless, as Frederik Ducrozet, head of macroeconomic analysis at Pictet Wealth Administration, has just lately stated, central banks have moved “from no matter it takes to no matter it breaks”.

There’s one other element within the evolution of liquidity that maintains a relative autonomy –and potential riot– about what financial authorities formulate, even when conditioned by them: financial institution credit score. Along with the liquidity created/destroyed by the Central Financial institution, business banks additionally create cash through the financial institution multiplier, relying on how idle or not they resolve to go away their reserves. Banks create cash once they lend or purchase an asset. Central banks act on reserves, however what’s manufactured from them depends upon the banks’ selections on how a lot use them.

Banks in the US have created some huge cash within the current previous. Because the starting of the pandemic, financial institution credit score grew by US$ 1.5 trillion in 2021 and; because it has been increasing at a tempo not seen earlier than the worldwide monetary disaster in 2008. One could count on them to not mitigate the impression of QT, however moderately to reinforce it. However how a lot they may do is an open variable.

One other variable within the equation is the values of monetary belongings. Market-valuation of belongings in financial institution portfolios makes these asset costs transmittable to financial institution credit score through capital restrictions and different choice guidelines concerning the amount of their operations.

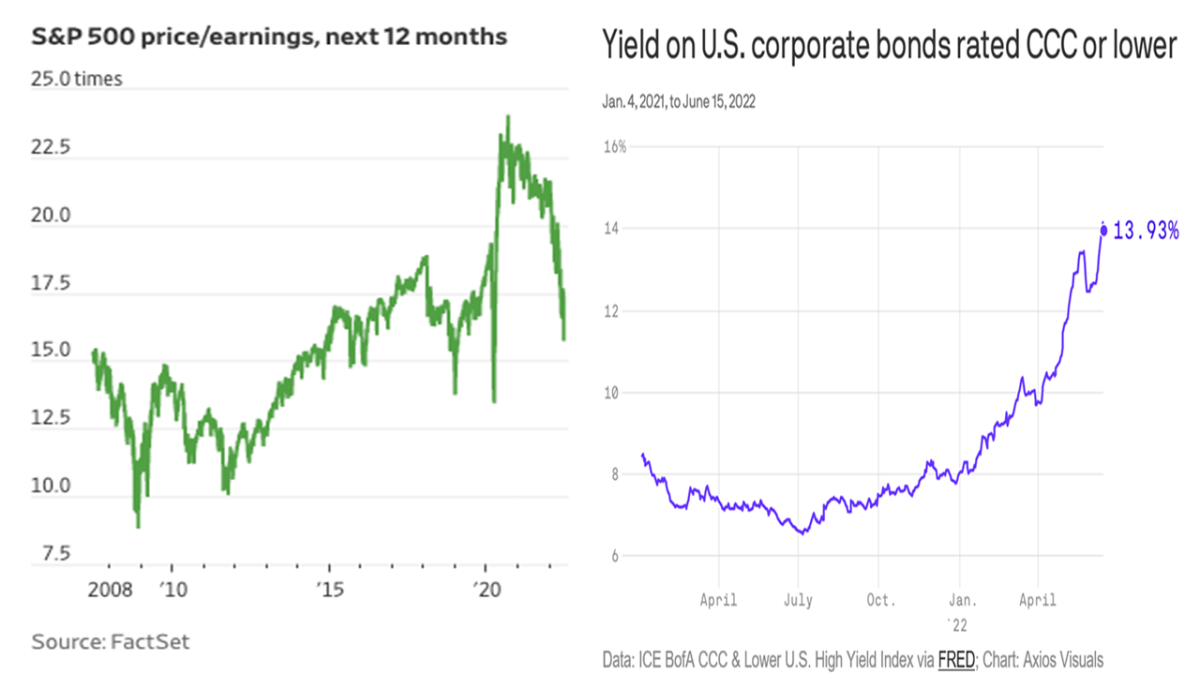

Tighter liquidity circumstances and anticipated rate of interest hikes have underlain the autumn in fairness markets this 12 months, notably within the case of (technology-related) long-duration belongings which have obtained high-prices relative to present earnings due to extraordinary earnings anticipated sooner or later. Larger anticipated rates of interest in the US have elevated reductions on such future earnings.

Share values have melted (Determine 4, left facet), whereas riskier bonds have confronted stiffer threat premiums (Determine 4, proper facet). The selloff in US bond and inventory markets in current months has led to a considerable write down in steadiness sheet values: near US$ 16 trillion, 60% of 2019 GDP. The current deterioration of circumstances in the actual property market, the place a considerable a part of the credit score goes, tends to strengthen a cooling of financial institution credit score as potential reinforcement of QT.

Determine 4 – Costs-to-Earnings and Bond Yields

Monetary asset values additionally have an effect on the goal of financial coverage by means of their so-called “wealth impact” on combination demand. In actual fact, it will probably even be stated that in current a long time the financial cycle in the US and different superior economies has been strongly conditioned by what occurs of their monetary sphere (Canuto, 2021).

Rising rates of interest, QT and falling shares are constantly pointing within the course of financial slowdown and, tentatively, declining inflation. Till then, the worldwide excessive inflation shock has led to a world rate of interest shock (Canuto, 2022a). Even with totally different magnitudes of results, QT provides itself to coverage fee will increase to tighten monetary circumstances, change threat evaluations, and impression capital flows to rising markets.

Capital flows to rising markets

How have tightening international monetary circumstances affected capital flows to rising market economies? How probably is a repeat of the 2013 taper tantrum or the Might storm of 2018? How concerning the greenback appreciation, which is reckoned as painful for rising markets with important shares of US-dollar-denominated liabilities (Canuto, 2020b).

The state of affairs tends to be difficult for rising markets when, like now, the tightening of worldwide monetary circumstances is pushed by issues about inflation or adjustments in threat sentiment. When rates of interest in superior economies go up due to extreme financial progress, the commerce channel of transmission could compensate the monetary one, which isn’t the case now. The character of tightening will make a distinction – whether or not it’s orderly or accompanied by market turbulence, together with episodic tantrums in US greenback funding markets.

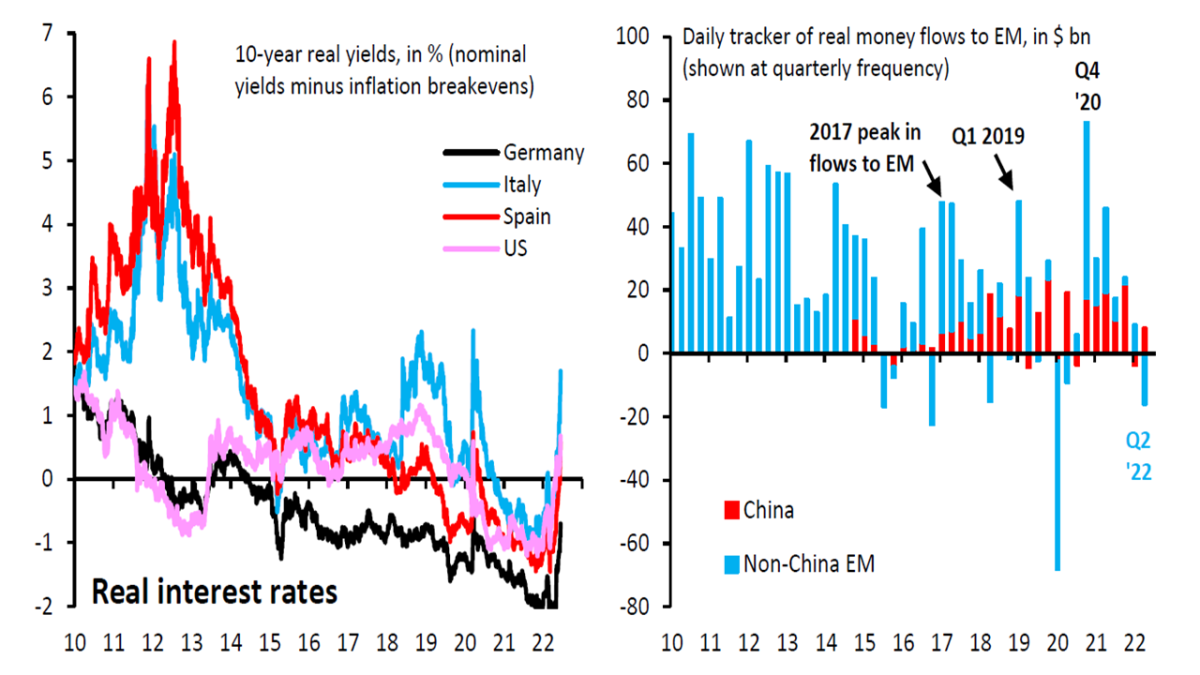

And the worldwide rate of interest shock has been accompanied by capital outflows from rising markets (Determine 5). Whereas long-term authorities bond yields rose throughout superior economies (left facet) due to tightening monetary circumstances and reflecting augmented threat aversion, outflows from rising markets occurred – as captured by the Institute of Worldwide Finance (IIF)’s high-frequency move monitoring internationally’s most vital EM (proper facet). In keeping with Brooks et al. (2022), U.S. 10-year actual Treasury yields moved from -1.1% on the finish of final 12 months to at the moment constructive 0.7%, a better soar than in the course of the 2013 “taper tantrum” (Determine 5, left facet).

Determine 5 – World Curiosity Charges and Rising Market Capital Outflows

By the end-Might, near US$ 36bn had flowed out of rising market mutual and exchange-traded bond funds because the begin of the 12 months. Fairness market flows have additionally gone into reverse because the starting of Might. The image on flows to local-currency bonds has been various and uneven.

Within the case of China, Covid and geopolitics – after the Russian invasion of Ukraine – appear to have triggered a pointy sell-off of shares earlier this 12 months, after rising sharply in 2020-21. However traders have began to return regularly ultimately of Might.

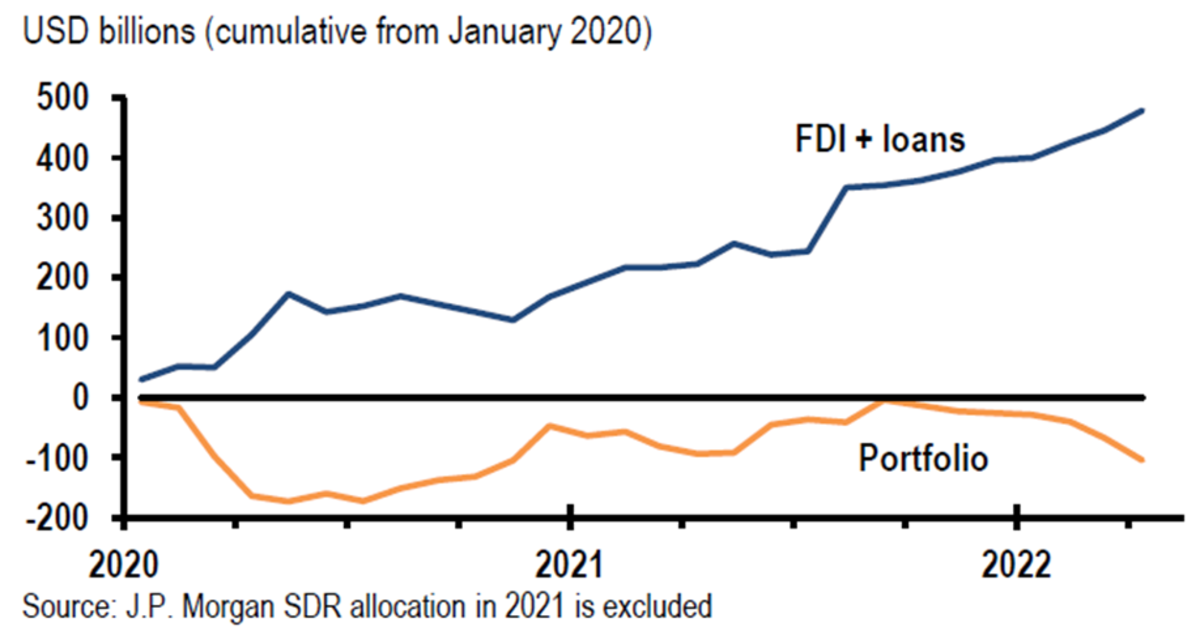

It ought to be famous, nonetheless, that non-portfolio flows (overseas direct funding and loans) have exhibited a better resilience (Determine 6). Moreover, extra broadly, as remarked in a current report by JPMorgan economists wanting solely at internet capital flows could result in a unsuitable underestimation of capital inflows relative to pre-global monetary disaster, as resident outflows have risen since 2013 seeking threat diversification. Portfolio flows to EM have shrunk, in addition to financial institution and company exterior loans, whereas overseas direct investments remained sturdy.

Determine 6 – EMX Month-to-month Internet Capital Flows

Taking a look at these flows from the standpoint of the rising markets’ vulnerabilities, the image seems to be much less gloomy than in earlier conditions of outflows. Projected present account deficits within the 12 months forward are definitely small by historic requirements. Moreover, fiscal deficits haven’t totally normalized but, however many nations have introduced giant cuts quickly.

Many rising markets responded to native impacts of the worldwide inflation shock earlier than superior economies and present rate of interest differentials are likely to mitigate the results of rate of interest will increase within the latter. There are although rising markets the place rates of interest stay exceptionally low – together with destructive actual ranges in some instances.

Right here variety involves the fore, and one must go on a case-by-case foundation. On one excessive, now we have frontier market economies which might be overly indebted and importers of meals and power (Lanaual al.l, 2022). Sri Lanka could have simply been a canary within the coal mine, signaling a wave of incoming debt defaults and restructuring, because the IMF and the World Financial institution have warned about. Over 20% of rising market bond issuers have debt buying and selling within the distressed territory.

On the opposite excessive, extra favorable, a number of rising markets have boosted reserves shares there and strengthened present account positions relative to the previous. On the finish of final 12 months, 58 % of EM have been estimated to have worldwide reserves exceeding 100% of the IMF’s adequacy metric. Commodity exporters have barely improved their commerce balances, GDPs, and public revenues with the commodity worth shock (Canuto, 2022b).

The “authentic sin” of forex mismatch within the case of public debt is just not as a deep sin as up to now, regardless of the outflows from EM native forex debt final 12 months. Elevated personal financial savings in the course of the pandemic have even facilitated a substitution of overseas collectors by home traders in buying home public debt.

Personal non-financial debt in overseas forex relative to the scale of the financial system varies significantly throughout nations, and a few have important exposures, notably on the company facet. Turkey stays like in its “fragile 5” occasions and Argentina has been out since its default. However they don’t seem to be consultant.

General, the purpose is that one should depend on a country-by-country foundation– taking a look at their international commerce and monetary linkages – when analyzing dangers/returns in rising markets together with the ongoing good storm (Canuto, 2022a). Nevertheless, total, the worldwide setting – together with QT and rate of interest hikes in superior economies, accompanied by international financial deceleration – is bringing headwinds to capital flows and financial progress in rising markets.

References

Aziz, J.; Marney, Ok.; and Jain, T. (2022). “EM capital flows: no matter will get you through the night time”, in JPMorgan, World Information Watch, June 17.

Brooks, R.; Fortun, J.; and Pingle, J. (2022). World Macro Views – The World Curiosity Price Shock and EM Outflows, , June 16.

Canuto, O. (2020a). Quantitative Easing in Rising Market Economies, Coverage Heart for the New South, November.

Canuto, O. (2020b). Why a Weaker Greenback May Be Good for Rising Markets? .

Canuto, O. (2021). U.S. Bubble-Led Macroeconomics, PB-21/29, August.

Canuto, O. (2022a). Rising Economies, World Inflation, and Progress Deceleration, Coverage Heart for the New South, PB-30/22, April.

Canuto, O. (2022b). Greatest Commodity Worth Shock in Fifty Years, Coverage Heart for the New South, Might 6.

Canuto, O.; and Cavallari, M. (2017). The Mist of Central Financial institution Steadiness Sheets, Coverage Heart for the New South, PB-17/07, February.

Crawley, E.; Gagnon, E.; Hebden, J.; and Trevino, J. (2022). Substitutability between Steadiness Sheet Reductions and Coverage Price Hikes: Some Illustrations and a Dialogue, FEDS Notes. Washington: Board of Governors of the Federal Reserve System, June 03.

Lanau, S.; Figueroa, M.P.; Fortun, J.; and Hilgenstock, B. (2022). Financial Views – Exterior Threat in Frontier Markets, Institute of Worldwide Finance (IIF), June 7.

Loane, Ok. (2022). QE: Not Trigger, However Symptom, Fathom, June 17.

Smith and Duguid (2022). Can the Fed shrink its $9tn steadiness sheet with out inflicting market mayhem? Monetary Instances, April 7.

[ad_2]