[ad_1]

The delayed third-quarter GDP report will, presumably, be printed ultimately, nevertheless it’s historical historical past at this level. The main focus has turned to an array of knowledge from numerous sources for October and November. A consensus view remains to be evolving, however the primary takeaway in the mean time is that recession danger nonetheless seems low to date in This fall.

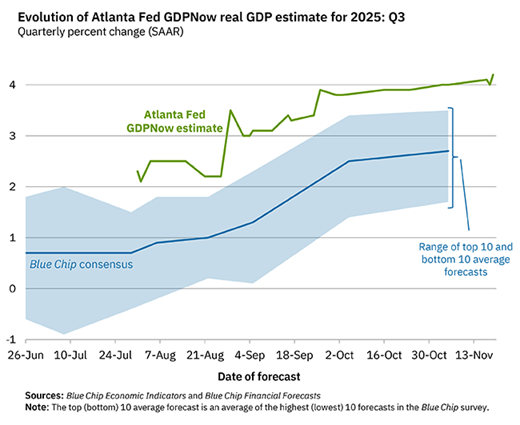

On a GDP degree, the tailwind in Q3 nonetheless seems to be sturdy, primarily based on the Atlanta Fed’s GDPNow mannequin. Final week’s replace reveals development accelerated to 4.2% in Q3, up barely from Q2’s sturdy 3.8%. Different numbers level to a slowdown in Q3, however even in case you favor the decrease GDP estimates it appears seemingly that the worst you may say in regards to the July-through-September interval is that the economic system slowed, however solely reasonably.

The same debate is shaping up for This fall. The principle query: How a lot is the economic system slowing within the last quarter of the yr?

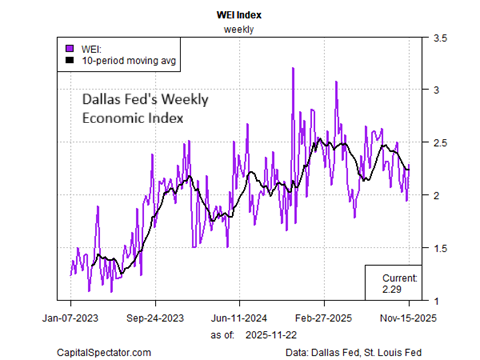

Utilizing the Dallas Fed’s Weekly Financial Index (WEI) as a information highlights a transparent downshift, primarily based on knowledge by means of Nov. 15. The present estimate signifies four-quarter GDP development at 2.3%, up barely from Q2’s 2.1%. The pattern has softened lately for WEI estimates, however recession danger stays low by this measure.

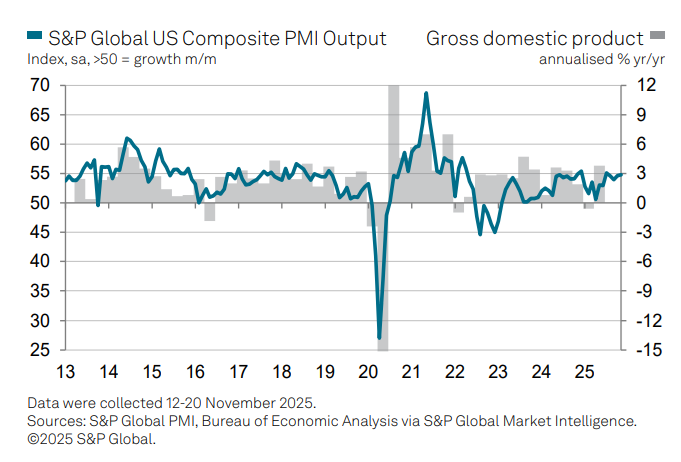

One other early have a look at November financial exercise additionally paints a comparatively upbeat profile. US enterprise exercise accelerated for a second successive month in November, in keeping with the US Composite PMI Output Index, a survey-based GDP proxy. “The upturn seems to be encouragingly broad-based for now, with output rising throughout each manufacturing and the huge companies economic system,” mentioned Chris Williamson, chief enterprise economist at S&P World Market Intelligence. “A marked uplift in enterprise confidence about prospects within the yr forward provides to the excellent news.”

But some analysts see bother approaching. Neil Dutta, head of economics at Renaissance Macro Analysis, lays out a worrisome situation, explaining that whereas “the economic system appears OK on the floor” in the mean time, “there are critical risks lurking beneath the floor of our economic system, and it’s higher to obviously determine them than to disregard them in favor of broad combination measures.”

The principle concern is payrolls, Dutta advises, with “essentially the most worrying indicators,” warning that “the labor market stays a supply of draw back danger for the broader economic system.”

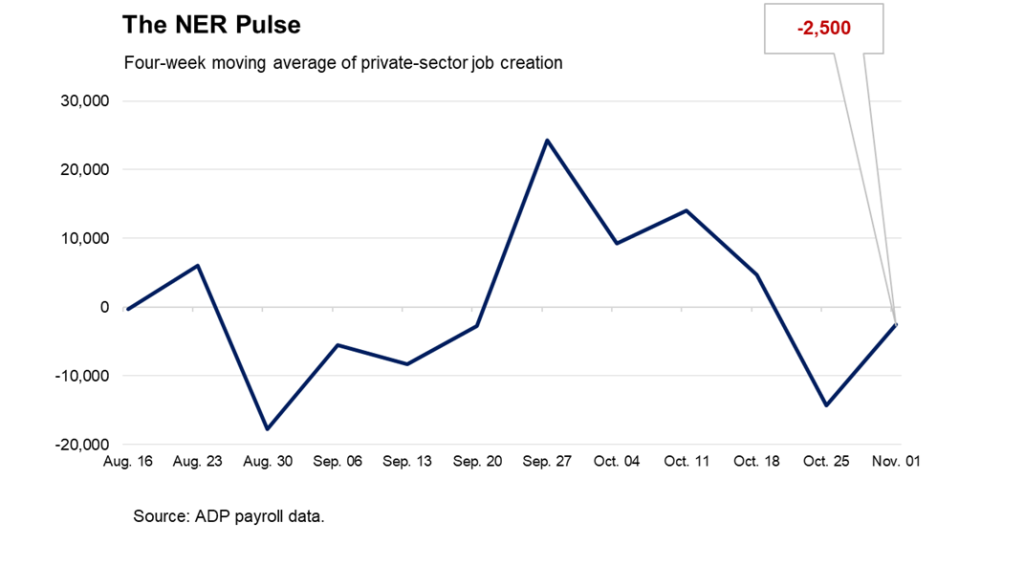

A number of personal sources recommend as a lot. Revelio Labs estimates that the payrolls contracted in October whereas ADP experiences that “personal employers shed a mean of two,500 jobs every week as employment losses slowed heading into November.”

The important thing query for the near-term financial outlook facilities on how the labor market evolves. The payrolls knowledge cited above suggests the die has been forged, however weekly jobless claims – a number one indicator for the labor market – have but to verify the darker forecasts. New filings for unemployment advantages fell 8,000 to a seasonally adjusted 220,000 for the week ended November 15, the Labor Division reported final week. Within the context of historical past, that’s a low degree and means that the labor market isn’t but signaling elevated recession danger.

All of that is topic to vary, after all. As the federal government numbers proceed to reappear on key points of the economic system, a number of the thriller will elevate on This fall. For now, it’s untimely to imagine {that a} recession has began or is imminent.

How is recession danger evolving? Monitor the outlook with a subscription to:

The US Enterprise Cycle Danger Report

[ad_2]