[ad_1]

Yves right here. Liberation Day weirdly appears extra distant in time than it truly is, and with that, a number of the reactions to its instant affect have additionally light. Market-oriented readers might however recall the shock on the selloff of the greenback. The economists beneath clarify that through the affect of retaliation, one thing many fashions don’t consider.

Nonetheless, they appear extra mystified by the autumn in Treasuries to. One wonders why. It cane about in no small measure resulting from an unwind of a hedgie buying and selling technique (the equal of selecting up pennies earlier than a steamroller). However one other issue not broadly sufficient acknowledged is that the US underneath Trump is a a lot riskier proposition for international cash managers. Extra threat means a better required return. Costs have to regulate downward to replicate greater low cost charges.

By Giancarlo Corsetti, Pierre Werner Chair and Joint Professor, Division of Economics and Robert Schuman Centre for Superior Research European College Institute, Simon Lloyd, Analysis and Coverage Advisor Financial institution Of England, and Daniel Ostry, Analysis Economist Financial institution Of England. Initially printed at VoxEU

To many, the US greenback depreciation following the ‘Liberation Day’ tariff announcement on 2 April 2025 defied typical knowledge. Nonetheless, open-macro fashions predict that the affect of tariffs on trade charges will depend on how commerce companions reply. Accounting for retaliatory threats, this column explores the consequences of tariffs on the US greenback by revisiting the affect of US tariffs introduced or levied between 2018 and 2020, compared to these in 2025. When tariffs are met with retaliation, the US greenback weakens, according to the expertise after Liberation Day. The spike in long-maturity US Treasury yields since 2 April is, nevertheless, extra unprecedented.

The sharp depreciation of the US greenback (USD) following the ‘Liberation Day’ tariff bulletins on 2 April 2025 appeared to mark a break from previous patterns. The US greenback weakened considerably, each towards the euro and in efficient phrases throughout a basket of currencies (see Determine 1). Many argued that this response goes towards the standard knowledge (Hartley and Rebucci 2025, Cardani et al. 2025), which holds that, by shifting international demand, tariffs ought to respect a rustic’s forex. Others have interpreted the greenback depreciation, coupled with a spike in long-maturity US Treasury bond yields, as a ‘reserve-currency shock’ (Jiang et al. 2025) – a shift in investor perceptions concerning the security premium historically related to US property and the US greenback.

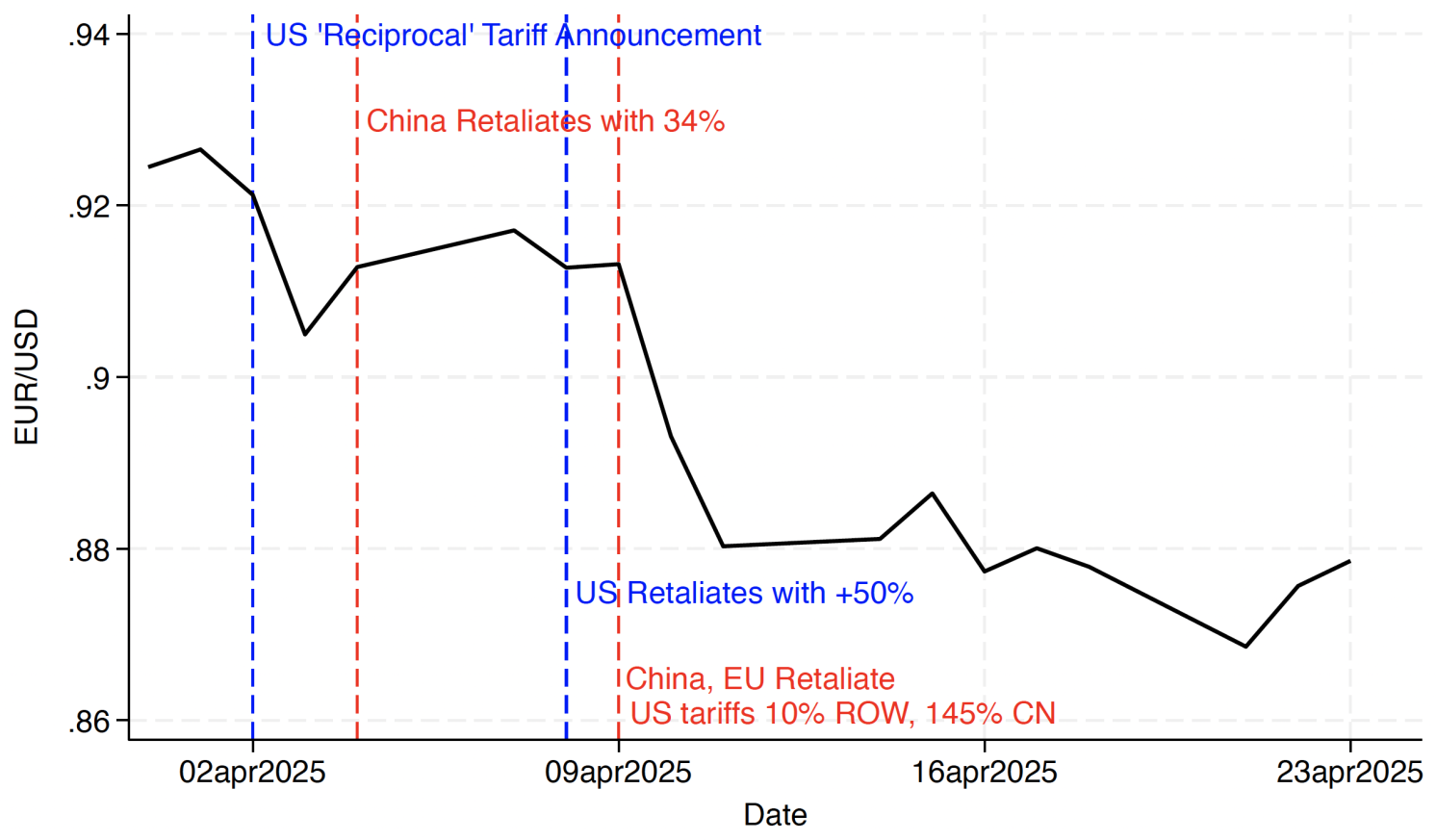

Determine 1 The US greenback depreciated considerably towards the euro (and different currencies) within the days after Liberation Day

Supply: Ostry et al. (2025)

Nonetheless, open-macro principle predicts that the affect of tariffs on trade charges will rely upon how commerce companions reply to such measures. That’s, the US greenback’s response to tariffs relies upon crucially on whether or not tariffs are met with retaliation, appreciating when tariffs are imposed unilaterally however depreciating in any other case. As Bergin and Corsetti (2023, 2025) present, this outcome can emerge from the mixed results of commerce coverage and optimum financial stabilisation – each within the US and overseas – when exports are invoiced in {dollars}. By that lens, the post-Liberation Day US greenback depreciation will not be so stunning in spite of everything.

In a latest paper (Ostry et al. 2025), we take a look at whether or not this theoretical prediction is borne out within the knowledge.

Revisiting 2018-2020

To do that, we revisit tariff exchanges from the 2018-2020 interval and use these to ask: do tariffs essentially result in a stronger forex? Relative to the present literature, our innovation lies in distinguishing between tariff shocks that do and don’t characteristic overseas retaliation.

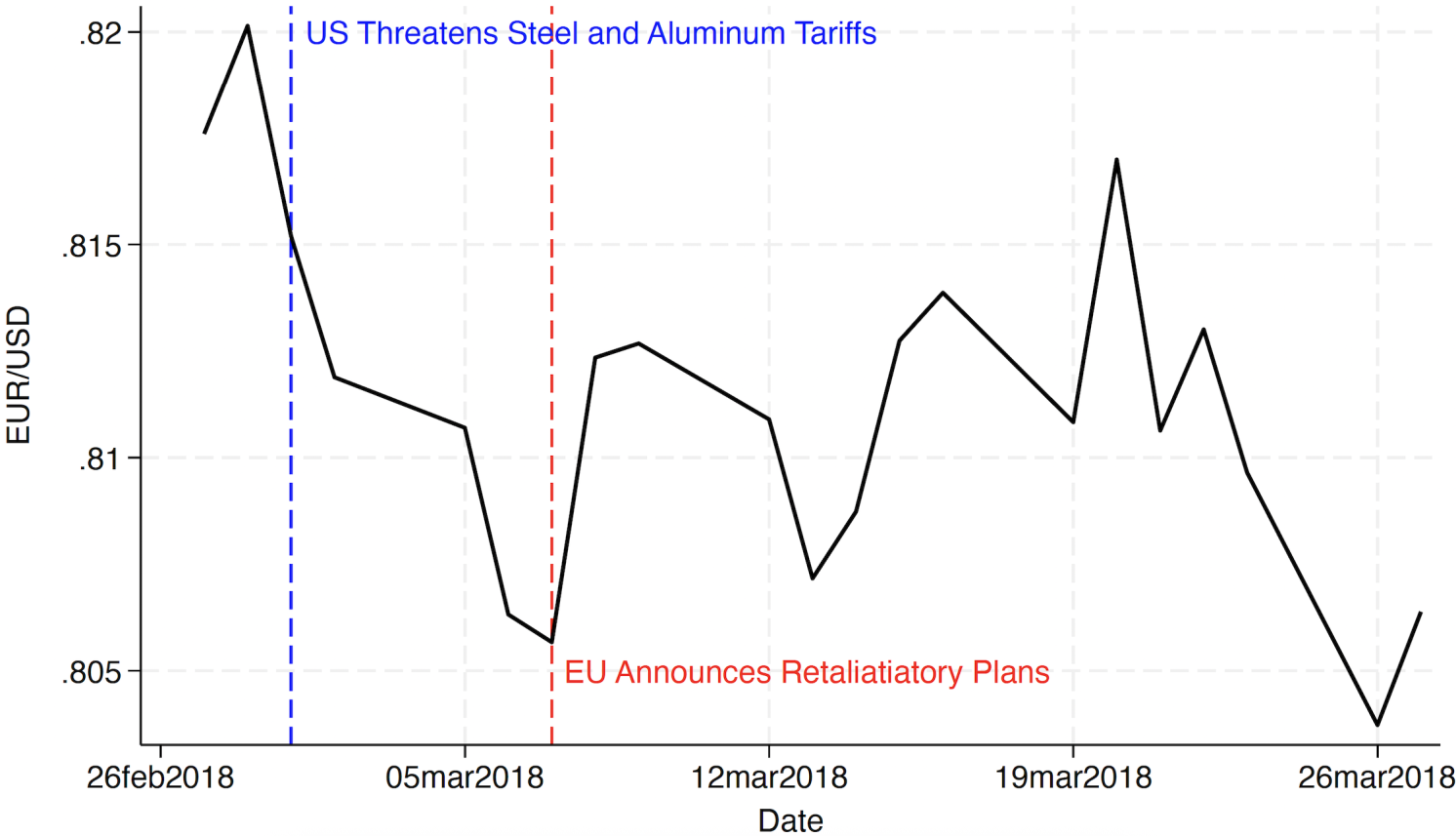

An illustrative instance from 1 March 2018 greatest motivates our evaluation. On this date, the US introduced tariffs on metal and aluminium imports from the EU. A retaliatory response was rapidly anticipated. For instance, a Monetary Instances headline on 2 March learn: “EU considers imposing ‘safeguard’ import tariffs in response to US”. And, on 7 March, the EU formally introduced retaliatory measures. As was the case after Liberation Day, the US greenback weakened instantly after the US announcement and remained decrease all through March (see Determine 2).

Determine 2 The US greenback additionally depreciated towards the euro after 1 March 2018 tariff bulletins

Supply: Ostry et al. (2025)

Our econometric evaluation, utilizing every day knowledge, confirms that this sample is systematic. The important thing takeaway is that US tariff bulletins should not essentially related to a stronger US greenback. In actual fact, a depreciation is frequent when markets anticipate overseas retaliation.

A Novel Dataset

To hold out our research, we constructed a novel database of US tariff bulletins, threats and implementations from 2018-2020 and, for comparability, from 2025. This additionally consists of corresponding responses from the EU, China, and Canada. We relied on detailed occasion timelines compiled by the Peterson Institute for Worldwide Economics, supplemented with real-time information protection.

The ensuing dataset consists of 35 US and 15 overseas tariff occasions from 2018-2020, and 13 US and ten overseas occasions from 2025. We quantify the financial dimension of every motion with an ‘efficient tariff charge’ – a weighted common combining advert valorem tariff charges and import shares. This captures the financial relevance of every occasion.

Every US tariff occasion is handled as a ‘shock’ – containing data largely unanticipated by markets, by way of tariff charge, sector, and protection. Since rest-of-the-world occasions characterize retaliations, the unanticipated nature of those occasions is much less clear. We subsequently use the overseas responses to tell apart between US tariff shocks that have been and weren’t retaliated towards. In our baseline, a US tariff shock is labelled as ‘retaliated towards’ if one other nation threatens or imposes a tariff inside seven days (we take a look at the robustness of this definition).

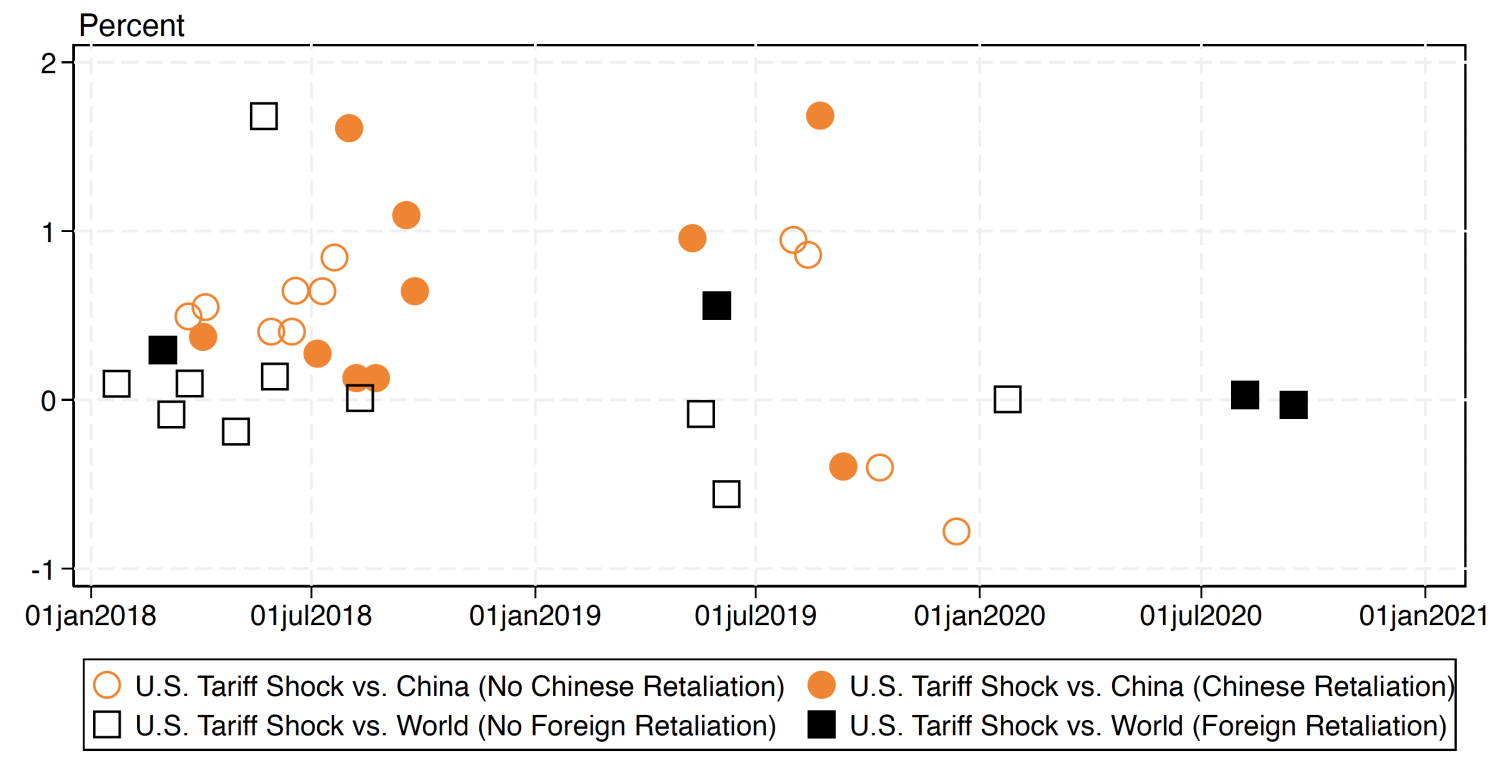

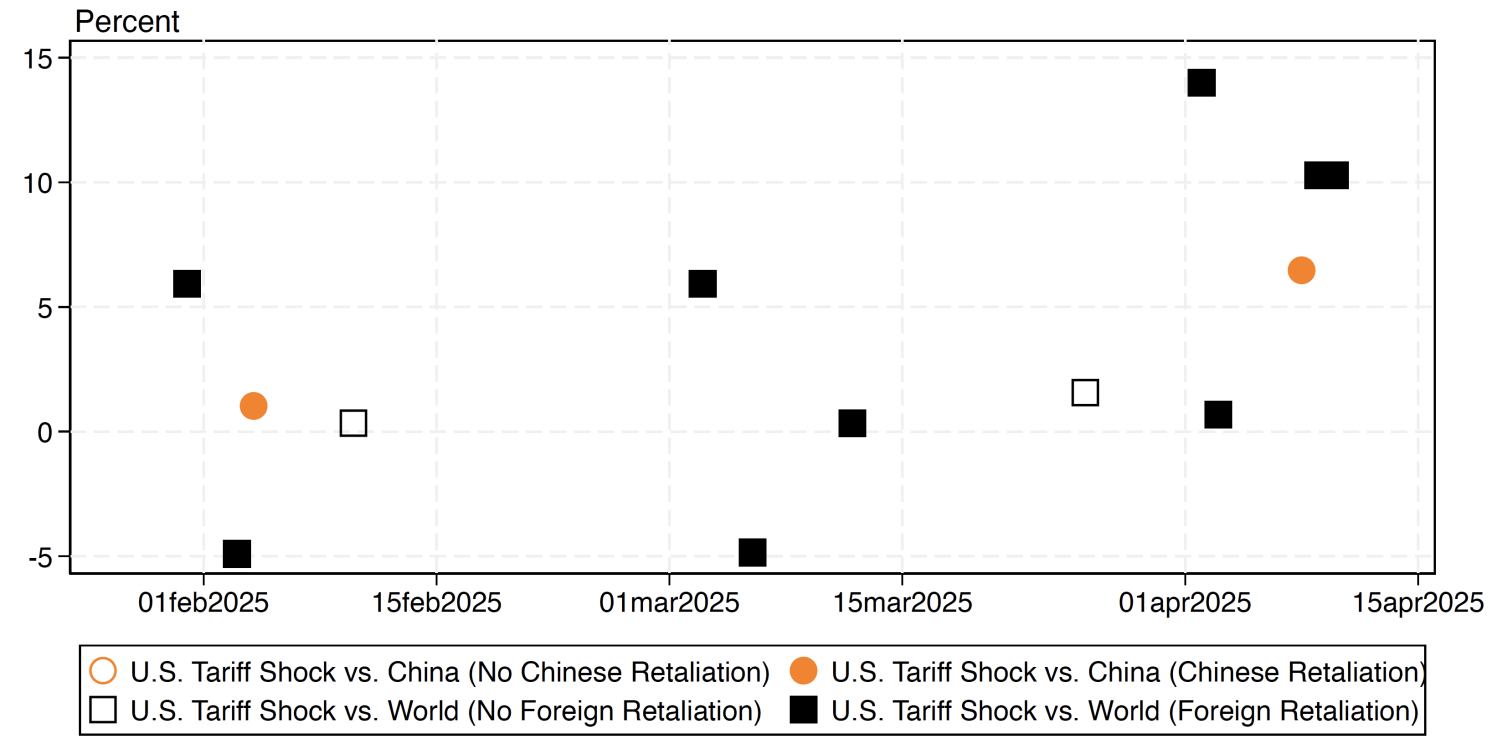

The tariff occasions in our dataset are illustrated in Determine 3, which plots efficient US tariff shocks over 2018-2020 (high panel) and in 2025 (backside panel). Orange circles characterize tariffs that focused China solely, whereas black squares denote tariffs aimed toward a wider set of nations, usually along with China. These principally replicate tariffs on particular merchandise akin to metal and aluminium, autos, photo voltaic panels, and washing machines in 2018-2020. Stuffed markers point out actions that have been retaliated towards. For example, the primary crammed black sq. on the left marks the 1 March 2018 metal/aluminium announcement. The calculated shock is about 0.3 share factors, accounting for the 25% and 10% tariffs on metal and aluminium, respectively, and their share in complete imports.

Determine 3 Efficient tariff charge shocks in 2018-2020 and 2025

a) 2018-2020

b) 2025

Supply: Ostry et al. (2025).

Notice: Shocks constructed by combining tariff information timeline from PIIE with narrative proof on the dimensions and financial relevance of every occasion.

Two key variations are evident between the US tariff shocks in 2018-2020 and people in 2025, along with the truth that US tariff actions have been an order of magnitude bigger in 2025 (the two April 2025 announcement was a 14 share level shock). First, nearly all 2025 US tariff actions are retaliated towards, in comparison with fewer than 50% in 2018-2020. Second, most 2025 US actions apply to a broad set of nations and have international retaliation, whereas most 2018-2020 actions focused China solely.

Tariffs and Alternate Charges

Armed with our dataset, we use native projections to estimate how the US greenback and different variables reply to US tariff shocks. Determine 4 presents the important thing outcomes for the 2018-2020 interval.

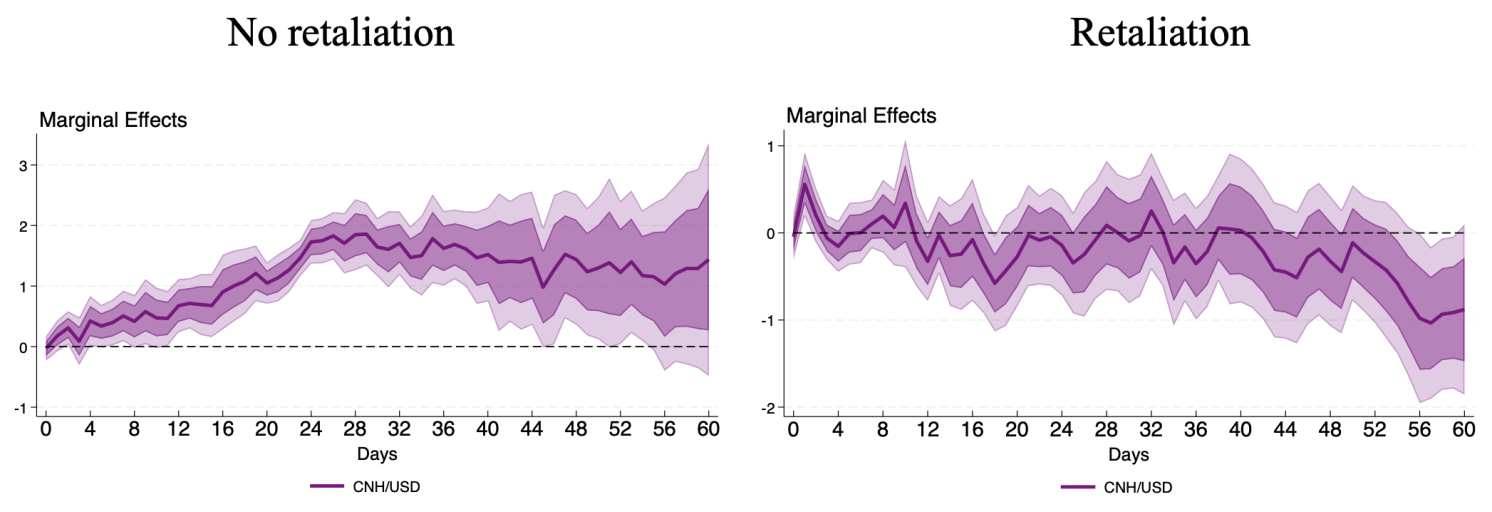

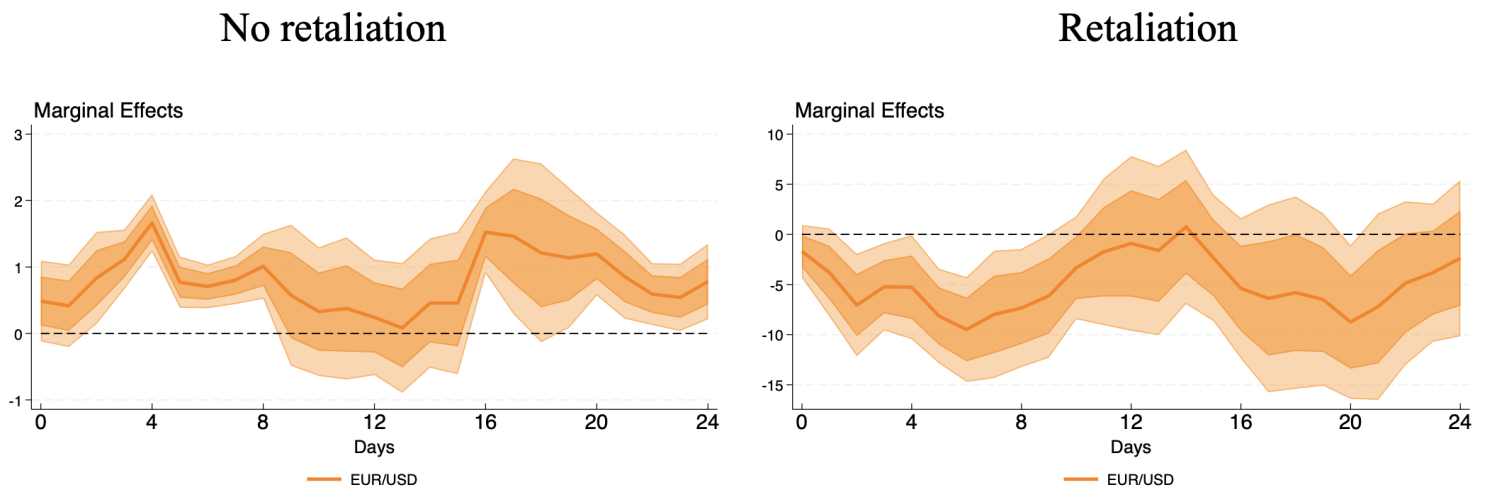

Determine 4 The affect of US tariffs on the US greenback conditional on retaliation or not

a) All US tariffs

b) US ‘international’ tariffs

Supply: Ostry et al. (2025)

Panel A reveals the response of the bilateral CNH/USD trade charge (the place a rise implies US greenback appreciation) to a one share level US tariff shock with no retaliation (left determine) and with retaliation (proper determine). Within the absence of retaliation, US tariff actions generate a big US greenback appreciation towards the CNH – according to the standard knowledge – with a one share level tariff shock projected to understand the US greenback by 2% after 4 weeks, on common. However within the presence of retaliation, the preliminary appreciation of the US greenback is totally reversed, with the CNH/USD trade charge remaining unchanged.

Remarkably, retaliatory responses to US ‘international’ tariffs – people who apply not solely to China – result in a pronounced US greenback depreciation. That is illustrated in Panel B, which traces the response of the EUR/USD trade charge to the subset of US tariff shocks that apply to a wider set of US buying and selling companions – particularly, the EU, Canada, and Mexico, usually along with China. These international tariff shocks are extra akin to the 2025 ‘Liberation Day’ tariffs, which utilized to all US buying and selling companions.

As earlier than, conditional on no overseas retaliation, US international tariffs respect the US greenback, on this case towards the euro. Nonetheless, when met with retaliation, the US greenback depreciates strongly, falling by as much as 8% towards the euro per one share level efficient US tariff.

What Is Completely different in 2025?

As argued above, principle and proof recommend that when a rustic initiates a tariff trade, prompting widespread expectations of retaliation, its forex might not strengthen. On this sense, the US greenback’s depreciation in April 2025 is no surprise.

However there are key variations between the sooner pattern and 2025, significantly within the scale of the depreciation and its co-movement with different asset costs. To discover this, we lengthen our empirical mannequin to check the response of US bond yields at totally different maturities.

In each samples (2018-2020 and 2025), the US greenback depreciation is accompanied by a decline in short-maturity Treasury yields, according to principle. However, as we focus on in additional element within the paper, solely in 2025 will we observe a pointy rise in long-maturity yields.

Conclusion

The ‘Liberation Day’ US greenback depreciation is according to earlier findings: when tariff actions, particularly widespread ones, are met with threats of retaliation, the greenback weakens. The decline in short-term yields can be according to previous episodes. What’s new, nevertheless, is the sustained rise in long-term Treasury yields – an unprecedented transfer in our dataset.

See authentic put up for references

[ad_2]