[ad_1]

Yves right here. No less than for now, market motion has confirmed our thesis that although marked weakening of the greenback is baked in long term, it could take a very long time to play out. BRICS followers have touted the GDP degree within the World South as an indicator of future. Nonetheless, monetary markets are dominated by funding flows, not by inhabitants and even GDP weight. Now we have to level out typically that the thrill over international locations slipping the noose of dollar-system US sanctions by buying and selling bilaterally in their very own currencies is just not even remotely sufficient to imperil the greenback. A BIS examine discovered that commerce transactions characterize about 3% of the worth of international alternate transactions. Equally, a current BIS survey discovered that the greenback share of international alternate transactions had elevated since 2022:

Highlights from the 2025 Triennial Survey of turnover in OTC FX markets:

- Buying and selling in OTC FX markets reached $9.6 trillion per day in April 2025 (“net-net” foundation,2 all FX devices), up 28% from $7.5 trillion three years earlier.

- Turnover of FX spot and outright forwards was 42% and 60% greater, respectively. Their shares in world turnover thus elevated, from 28% and 15%, to 31% and 19%, respectively. Turnover of FX choices greater than doubled. Turnover of FX swaps grew modestly, leading to a drop of their share to 42% (from 51% in 2022).

- The US greenback continued to dominate world FX markets, being on one facet of 89.2% of all trades, up from 88.4% in 2022. The share of the euro fell to twenty-eight.9% (from 30.6%) and that of the Japanese yen was nearly unchanged at 16.8%. The share of sterling declined to 10.2% (from 12.9%). The shares of the Chinese language renminbi and the Swiss franc rose to eight.5% and 6.4%, respectively.

- Inter-dealer buying and selling accounted for 46% of worldwide turnover (nearly unchanged from 47% in 2022). The share of buying and selling with “different monetary establishments” was 50% (up from 47%). At $4.8 trillion, turnover with different monetary establishments was 35% greater than in 2022, largely pushed by 72% greater buying and selling of outright forwards and a 50% improve in spot transactions with this counterparty group.

- Gross sales desks within the high 4 jurisdictions – the UK, the US, Singapore and Hong Kong SAR – accounted for 75% of complete FX buying and selling (“net-gross” foundation2). Singapore gained market share, reaching 11.8% of the overall (up from 9.5% in 2022).

Superior economies nonetheless have a lot greater GDP per capita. That interprets amongst different issues into extra funds out there for funding.

What’s subsequently prone to show detrimental to the greenback, maybe sooner relatively than later, is greenback investments falling out of trend. The Liberation Day flight from Treasuries produced a corresponding marked fall within the greenback. That has not solely been considerably reversed however a VoxEU examine even discovered that Treasuries have returned, at the least for now, to their standing as a haven in occasions of perceived excessive danger.

Trump is declaring battle on the perceived security of US monetary markets together with his continued deregulation push and promotion of crypto-scamming. An AI implosion and/or a personal debt market freakout may additionally result in flight from greenback investments and therefore the greenback.

By Wolf Richter, editor at Wolf Avenue. Initially printed at Wolf Avenue

A scorching theme broadly banded about to pump up cryptos, gold, silver, and even shares is the so-called “forex debasement commerce.” The thought is that sufficient merchants rally behind a typical theme to maneuver costs of their course for lengthy sufficient to make a critical buck and generate charges from the buying and selling.

This debasement-trade theme is a wager that authorities borrowing and cash printing will erode the worth of the US greenback dramatically and rapidly, and that subsequently sufficient traders will pile into cryptos, gold, silver, and even shares, to trigger costs of these devices to blow up. And so they did.

However the large bond market has taken the other wager, led by the $29-trillion Treasury market, the $11-trillion company bond market, the $9-trillion residential MBS market, the $4-trillion municipal bond market, plus the opposite segments of the bond market, the place yields have fallen this 12 months and have been in the identical comparatively slender vary for the previous three years.

These bond traders wager that inflation will cool additional over the longer horizon, and that the comparatively low yields they get on their securities will subsequently adequately remunerate them for inflation and for the dangers they’re taking, and that the cooling of inflation will trigger yields to say no additional sooner or later, thereby pushing up costs of bonds that had been issued earlier at greater yields.

If the bond market have been fearing a speedy and substantial debasement of the US greenback – the theme being hyped by the debasement commerce promoters – it could demand a lot greater yields. However that hasn’t been the case.

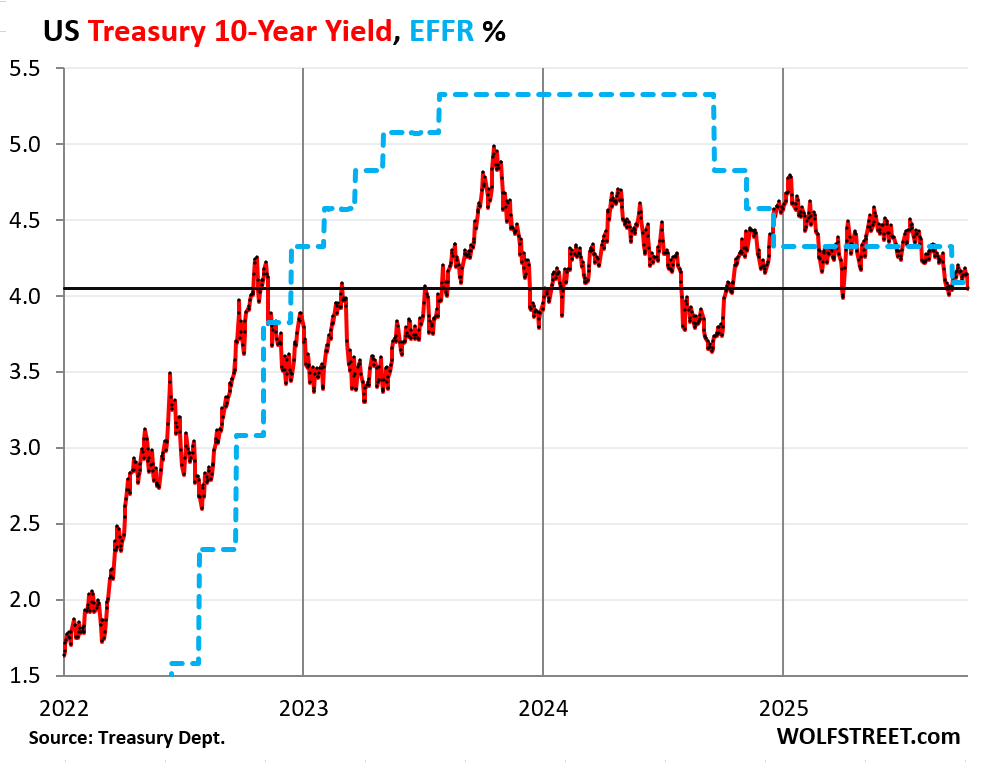

The ten-year Treasury yield, for instance — now barely above 4% as of Friday night (bond markets are closed right this moment) — has been on a downtrend this 12 months and has been roughly in the identical vary for 3 years:

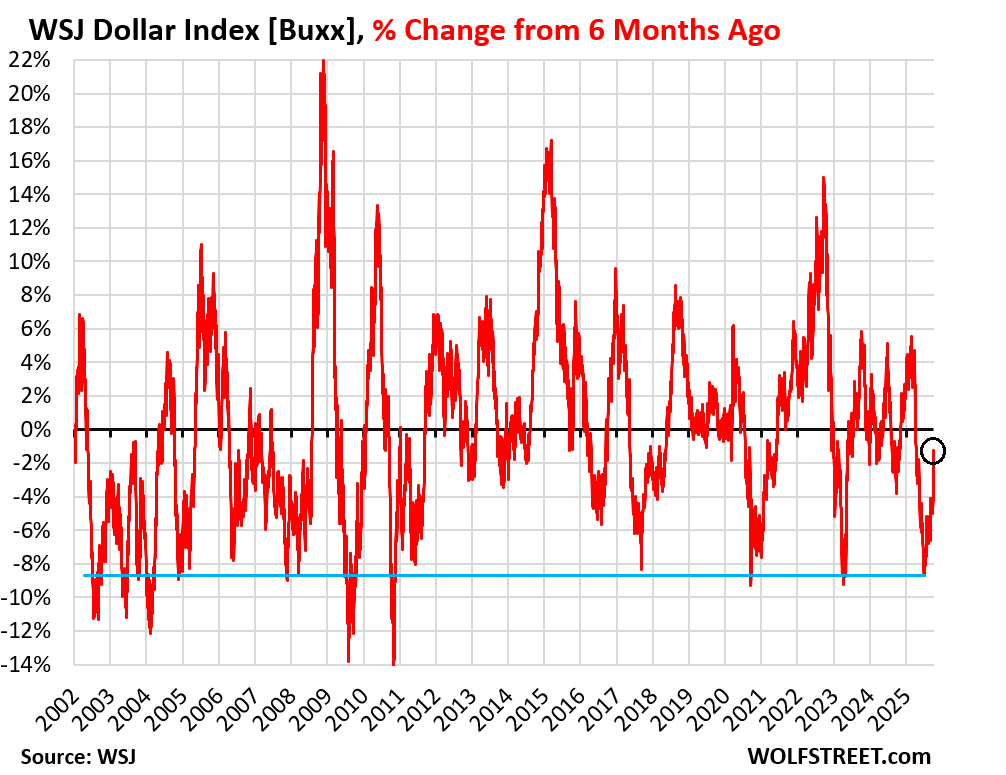

However, however, however, the US greenback…. The greenback’s drop throughout the first half of 2025 has been falsely promoted in clickbait headlines and by braindead manipulative speaking heads on TV, as “the steepest decline in additional than a half a century,” or no matter.

What did happen is that the greenback indices had spiked within the final 4 months of 2024 and topped out on the very finish of December. And that four-month spike was then unwound-plus-some over the six months precisely from the start of January via the start of July, with the euro and yen dominated DXY Greenback Index dropping 11% and the broader WSJ Greenback Index [BUXX] dropping 9% over the primary six months of the 12 months.

However even larger six-month drops have been frequent and bottomed out in:

- April 2023

- September 2020

- November 2010

- August 2009

- April 2008

- June 2007

- And so on., all the way in which again to Adam and Eve.

The one factor that was distinctive concerning the 6-month drop in 2025 was that it began firstly of January. Solely the beginning date was distinctive.

This chart reveals the 6-month share change of the WSJ Greenback Index [BUXX], which tracks a basket of 16 main currencies.

The blue line signifies the 6-month 9% drop from the start of January via the start of July. Notice all of the even larger 6-month drops which have dropped via the blue line over the previous 23 years.

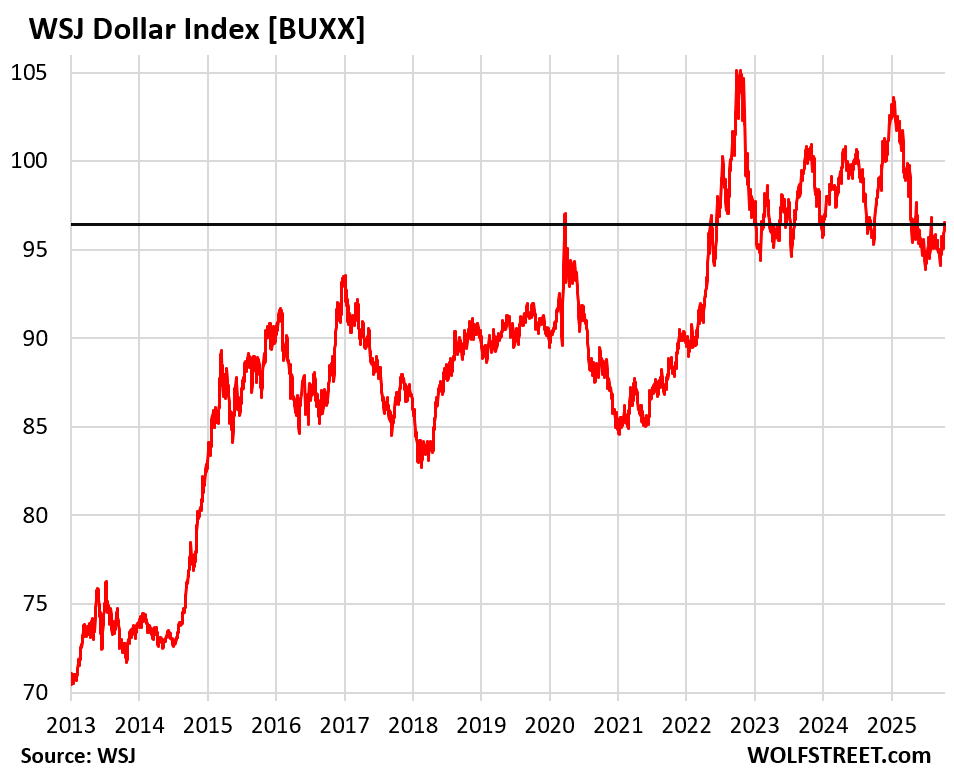

And naturally, the greenback has bounced again some for the reason that starting of July with the WSJ Greenback Index rising right this moment to 96.4, up by 2.6% from the low firstly of July.

The 16 currencies within the trade-weighted index are: Euro, Japanese Yen, Chinese language Yuan, Canadian Greenback, Mexican Peso, South Korean Gained, New Taiwan Greenback, Indian Rupee, Hong Kong Greenback, Singapore Greenback, British Pound, Australian Greenback, New Zealand Greenback, Norwegian Krone, Swiss Franc, and the Swedish Krona.

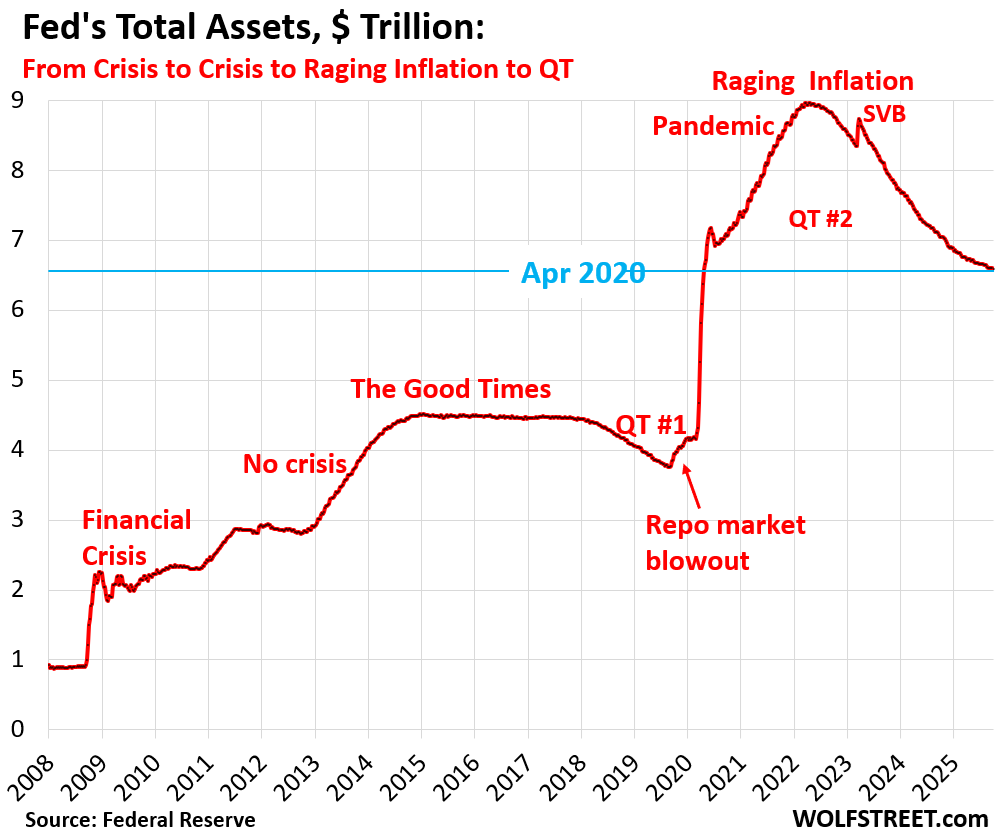

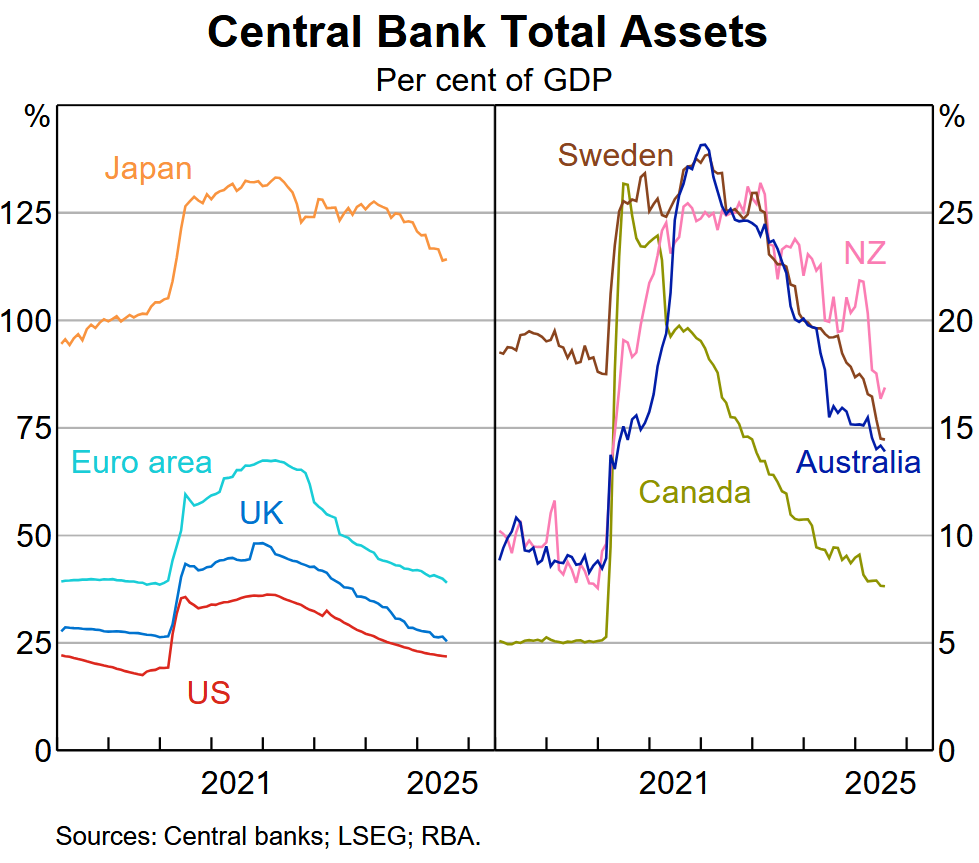

The Fed has been doing the other of “cash printing” for over three years, having shed $2.4 trillion in belongings by now – “cash unprinting?” – and it continues to shed belongings beneath its Quantitative Tightening program, and folk selling the debasement commerce want to try this:

Different central banks too have been shedding belongings beneath their QT packages, most notably the ECB and the Financial institution of Japan. Listed here are the stability sheets of among the main central banks in relationship to the dimensions of their economies, one other eye-opener of what the debasement commerce faces: Superb How the Cash-Printing World Has Reversed.

[ad_2]