[ad_1]

Unique – Coverage Heart for the New South

Whereas we level out a relative decline of the U.S. greenback weight in these features extra lately, we additionally spotlight gravitational components that are likely to uphold its place. Due to this fact, the “exorbitant privilege” that the U.S. greenback has offered to its issuer is prone to stay.

Information about “de-dollarization.”

The heavy monetary sanctions on Russia after the invasion of Ukraine sparked speculations that the weaponization of entry to reserves in {dollars}, euros, kilos, and yen would stimulate a division within the worldwide financial order. China would are likely to strengthen its personal worldwide funds system and speed up the institution of its forex – the renminbi – as a rival reserve forex to cut back its vulnerability to strikes of an analogous nature in opposition to it. Nations dealing with geopolitical dangers of their relationship with the US and Europe would seize the chance to change out of the greenback system. Nonetheless, there’s a strategy to go between prepared and doing on this case…

In March, Brazil and China agreed to make use of native currencies of their bilateral commerce. China is the nation’s largest buying and selling accomplice, being the vacation spot of greater than 30% of exports and the origin of greater than 20% of imports. Given the pattern in direction of surplus flows on the Brazilian aspect, it’s assumed that Brazil will accumulate reserves in renminbi (RMB).

On the Russia-China summit in March, President Putin mentioned that enterprise transactions between Russia and international locations in Asia, Africa, and Latin America can be completed in RMB. Final December, China, and Saudi Arabia carried out their first yuan transaction, following Saudi statements that they have been trying to diversify away from the US greenback. Including Iran, one other nation grappling with US sanctions, quickly “petrodollars” is likely to be changed within the dialogue by “petroyuans”.

Additionally value noting is French firm Whole Energies’ buy of liquefied pure fuel (LNG), settled in yuan, from Chinese language state-owned CNOOC.

Strictly talking, because the world monetary disaster, China has sought to increase the usage of the renminbi in worldwide commerce and as a reserve asset at different central banks. It pursued a proliferation of forex swap strains with central banks in different international locations – together with Brazil.

It’s not shocking, due to this fact, how the “de-dollarization” of the worldwide financial system, “multipolarity”, or “bipolarity” of the worldwide financial system have turn into buzzwords in latest months. Nonetheless, it’s essential to gauge the actual scope of what’s occurring.

Currencies as technique of cost

First, it’s crucial to contemplate the distinction between utilizing forex to settle transactions —that’s, as a way of cost– and its function as a retailer of worth. In fact, from the perspective of a central financial institution that must be prepared for these funds, utilizing forex in transactions tends to result in the structure of reserves within the corresponding forex.

Nonetheless, it’s value distinguishing between currencies’ makes use of for funds (flows) and shops of worth (shares, reserves), amongst different causes, as a result of transactions could also be settled with out utilizing a retailer of worth. The latest Brazil-China settlement, as an illustration, implies that importers will make funds in native currencies, as a substitute of every other forex, with settlements occurring periodically. An analogous scheme was used up to now by Brazil and different Latin American international locations to economize on the necessity to use U.S. {dollars} on all particular person cross-border transactions amongst them (Reciprocal Funds and Credit score Conventions, CCR in Portuguese and Spanish).

It must be famous on this context that the majority of overseas alternate transactions corresponds primarily to monetary operations, not commerce in items and companies. The scale acquired by Chinese language overseas commerce constituted a large foundation for the potential use of its forex, however not on the monetary transaction aspect.

In 2015, when the RMB was accepted to be a part of the particular basket of currencies that serves as the bottom for Particular Drawing Rights (SDRs, the accounting forex issued by the IMF), together with the greenback, euro, yen, and pound, it was due to its weight through China’s overseas commerce, not for standards relative to its use in monetary transactions.

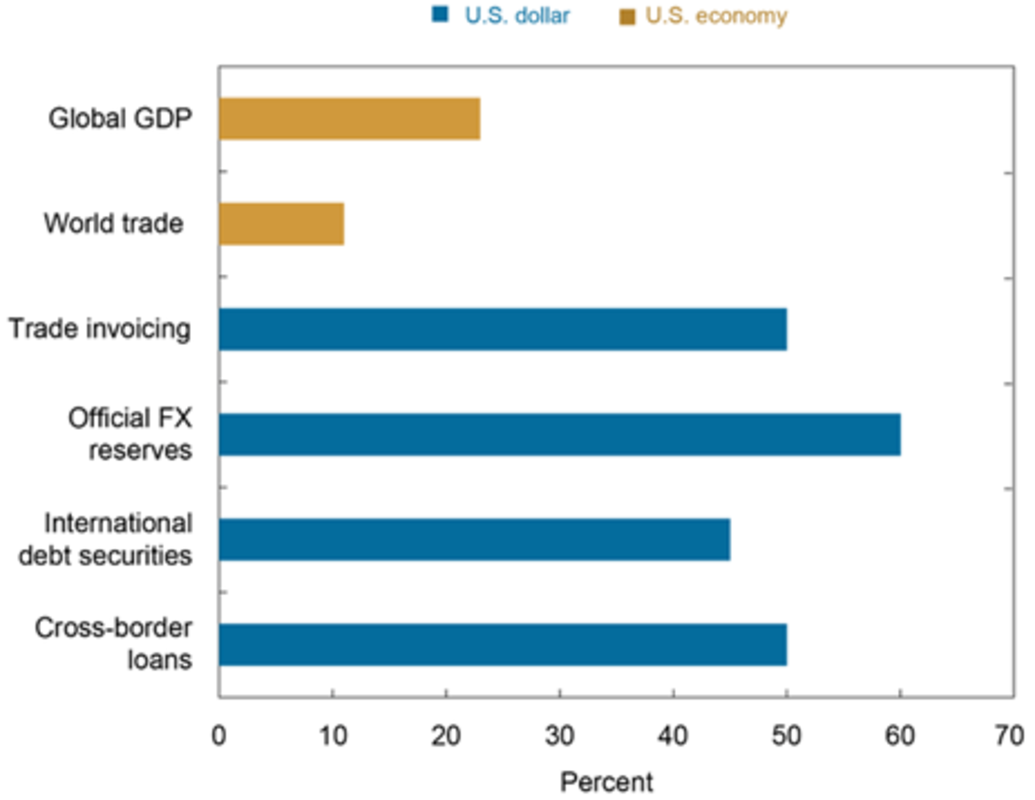

The worldwide use of the U.S. greenback within the worldwide financial system is way greater than the relative measurement of the U.S. financial system (Determine 1). The U.S. greenback’s shares of overseas commerce invoicing, worldwide debt issuance, and cross-border lending are properly above what the nation’s shares of worldwide commerce, worldwide bond issuance, and cross-border borrowing would counsel.

Determine 1 – The U.S. Greenback’s Function in Worldwide Financial System Eclipses the US’ Presence within the World Economic system

Commerce can, in fact, stimulate commerce finance in a rustic’s forex. Lenders lengthen credit score to facilitate the cross-border motion of products and companies.

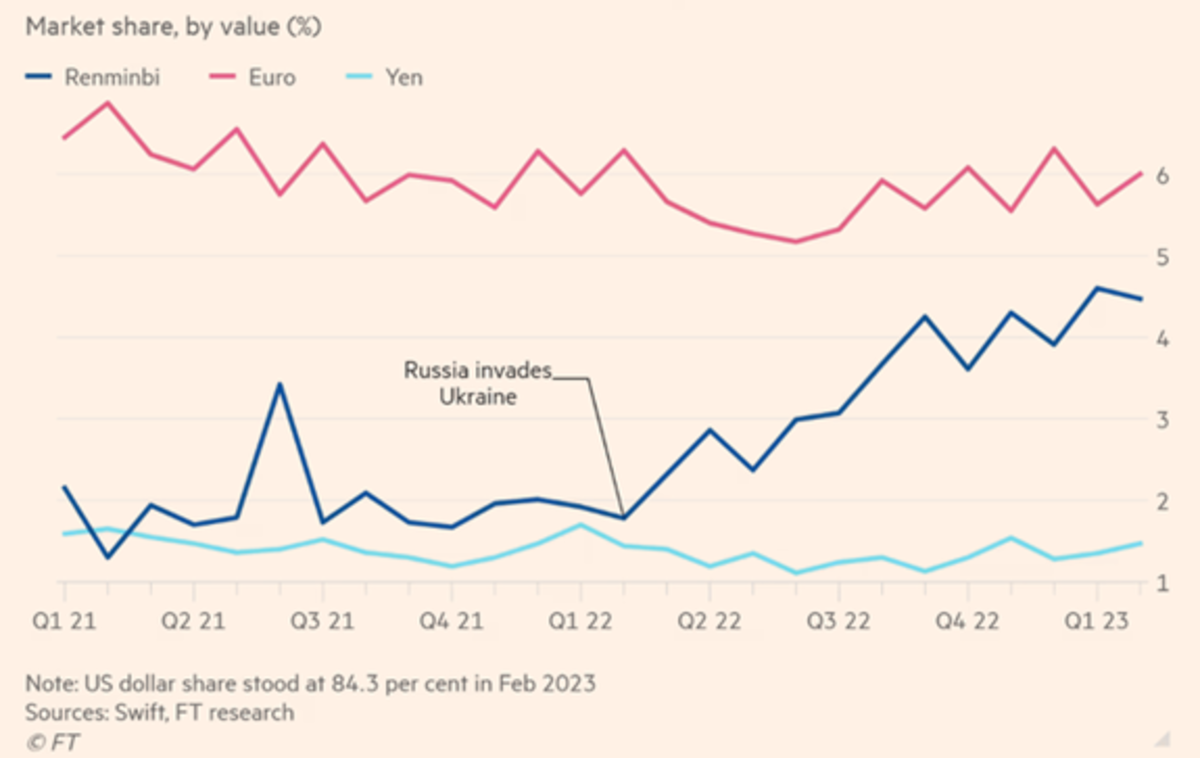

The renminbi’s share of commerce finance has greater than doubled because the invasion of Ukraine, as its share by worth of the market rose from lower than 2% in February 2022 to 4.5% a yr later (Determine 2). That mirrored the usage of China’s forex to facilitate commerce with Russia and the rising value of greenback financing because the begin of the on-going Fed’s interest-rate hikes (Locket and Leng, 2023).

Determine 2 – China has greater than doubled its share of world commerce finance

Whereas the euro and yen account for six% and fewer than 2% of the overall, the U.S. greenback’s share was 84.3% in February 2023, down from 86.8% a yr earlier.

The renminbi’s rising share of commerce finance displays China’s drive to speed up its internationalization. It constitutes a problem to the west’s use of sanctions to bar main Russian monetary establishments from utilizing the Swift platform of funds. The renminbi’s newest rise amongst commerce finance currencies has not been matched by higher use in worldwide funds made on Swift, which have plateaued at about 2 % of the worldwide complete.

China had already made an effort to internationalize the renminbi within the years main as much as August 2015, when a devaluation led to extreme capital flight. This led China’s central financial institution to reverse course and impose draconian capital controls that stalled China’s progress in selling the forex’s world use. Nonetheless, it appears to have shifted again to looking renminbi internationalization because the starting of 2022 by looking for higher use of the forex in settlement of cross-border commodities trades and bettering world entry to derivatives tied to renminbi property.

Currencies as shops of worth (reserves)

In addition to approaching the load of currencies of their use as the first conduit to conduct worldwide transactions (flows), both for commerce or for finance, one must measure their roles as reserve currencies of selection (shares) by central banks and different cross-border wealth holders.

Commerce transactions and reserves from central banks and different world public buyers may bolster the renminbi’s place instead forex to the greenback, euro, yen, and sterling. Nonetheless, to transcend settlement of transactions and commerce finance, the qualitative leap in direction of the internationalization of the Chinese language forex as a reserve forex will solely happen when confidence in its convertibility is ample to persuade unofficial (personal) buyers to maintain reserves denominated in it.

Central banks will need to have reserves in currencies with which they’ll function within the numerous alternate transaction areas. It’s not by likelihood that overseas alternate swap strains with China have been little used, whereas these of nations with the US Federal Reserve have been activated in occasions of must stabilize flows. As we argue within the following, tight capital controls maintained by China will curb the renminbi from transferring up dramatically the ranks of world funds currencies and a inventory functioning as a retailer of worth.

Over the past a long time, roughly two-thirds of the world’s overseas reserves have been maintained in US Treasuries and different quasi-sovereign USD property. A gradual decline within the greenback’s share in complete reserves occurred within the 2000s, and it was interpreted as a pure diversification by central banks reflecting commerce and monetary globalization. Even the introduction of the euro, regardless of bets on the time, didn’t considerably change the greenback’s dominance in overseas reserves.

The “greenback dominance” remained regardless of the falling share of US GDP within the world financial system. From the Nineteen Seventies onwards, it survived the tip of gold convertibility and of the mounted alternate price regime inherited from Bretton Woods. Its presence in banking and non-banking transactions grew after the 2007-08 world monetary disaster.

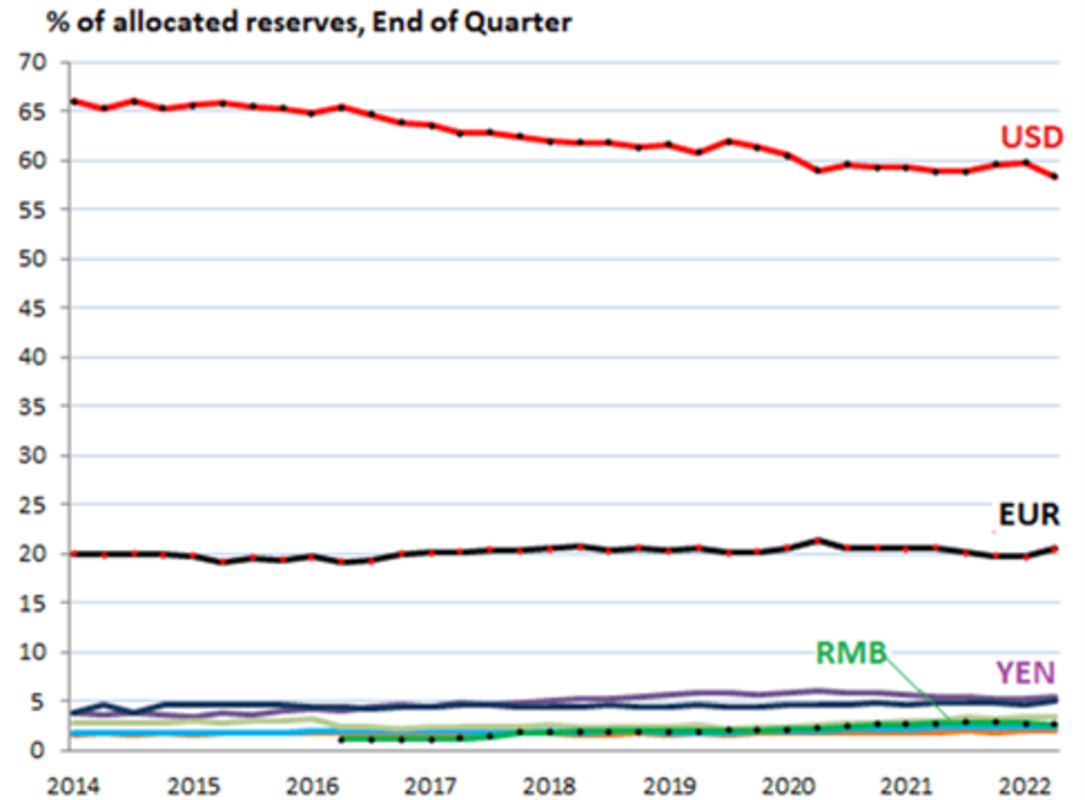

The Worldwide Financial Fund (IMF) releases quarterly information on official overseas alternate reserves (COFER). The most recent report exhibits a discount within the diploma of “greenback dominance”, with the greenback’s share of central financial institution reserves falling because the starting of the century, down 12 share factors from 71% in 1999 to 59% final yr (Determine 3).

Determine 3 – U.S. greenback share of world reserves

Not in favor of the pound sterling, the Japanese yen, or the euro – regardless of the rise that the latter skilled throughout its first decade of existence. As an alternative, in favor of what Arslanalp et al. (2022) referred to as “non-traditional reserve currencies” (Australian greenback, Canadian greenback, Swiss, and others), together with the Renminbi (RMB), which reached 2.6% of the overall (Determine 4).

Determine 4. Forex Composition of World Overseas Change Reserves 2014-2022 (%)

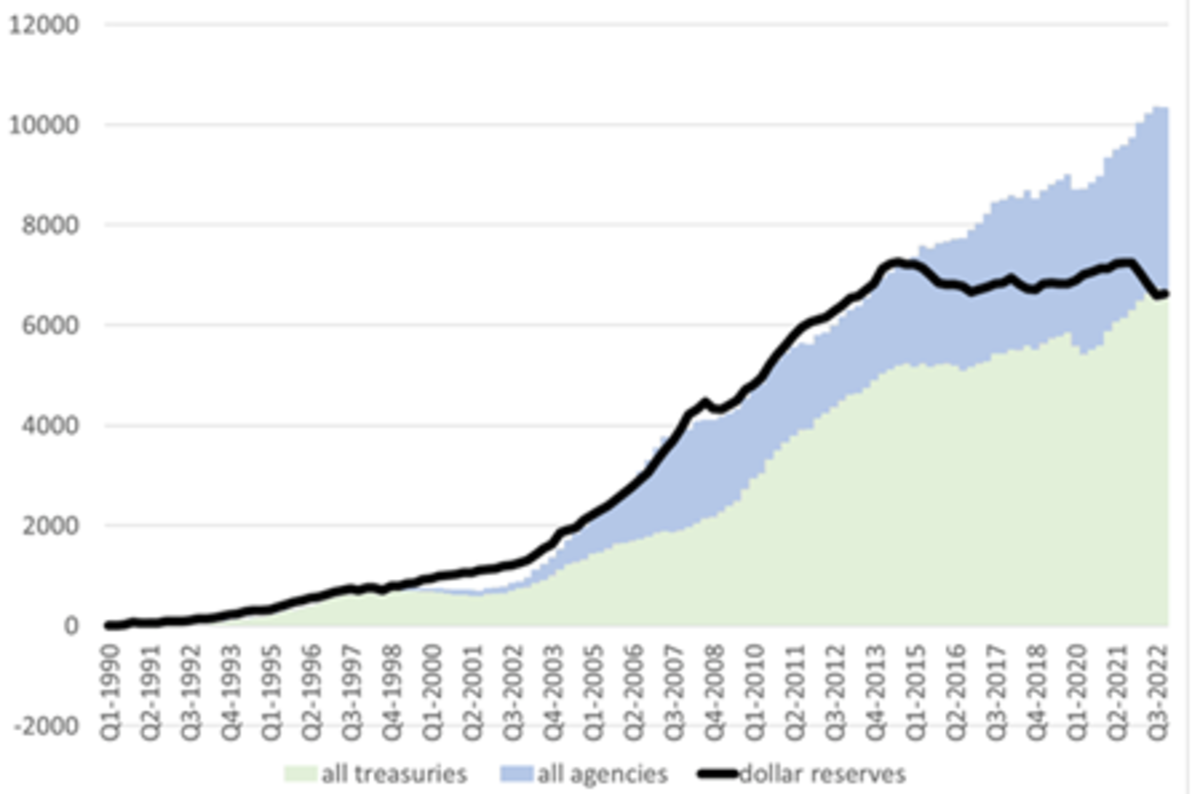

On the finish of This autumn of final yr, non-US central banks held $6.47 trillion in USD-denominated property, comparable to US Treasury securities, US company bonds, and US mortgage-backed securities. Even because the greenback’s share has dropped since 2014, holdings of dollar-assets rose from $4.4 trillion in 2014 to $7.1 trillion in Q3 2021 earlier than falling because the Fed initiated its QT and interest-rate hikes (Richter, 2023) (Canuto, 2022a).

The figures offered above should be adjusted to compensate for fluctuations in relative forex costs and keep away from distorting the notion of climbs or downfalls of their reserve standing.

De-dollarization will stay sluggish and bounded.

4 gravitational components favor the continuation of the greenback’s central place in worldwide monetary markets, in commerce invoices and funds, and private and non-private overseas alternate reserves. Name them “community – complementarity and synergy – results” (Arslanalp et al., 2022). The relative enlargement of the opposite currencies is dependent upon how efficiently they handle to offset these components.

First, the extra in depth put in base for dollar-denominated transactions favors the forex. The rise in liquidity and the discount in transaction prices within the “non-traditional” overseas alternate markets – together with technological enhancements in platforms – helped cut back this drawback.

As well as, no different financial system gives an equal quantity of “investment-grade” authorities bonds as the US does. That quantity permits central banks to build up reserves and personal buyers to make use of them as a “haven”, one thing bolstered by the “quantitative easing” because the world monetary disaster. On this regard, the announcement by then President of the European Central Financial institution, Mário Draghi, within the euro disaster in 2012, that he would do “no matter it takes” as a last-resort supplier of liquidity for euro-denominated property issued within the eurozone was important. Moreover, the European Restoration Fund was created final yr. The worldwide provide of liquid and safe-haven property usable as central financial institution reserves tended to widen in favor of the euro.

Third, additionally it is value noting that “non-traditional currencies” have been favored by a partial seek for returns in reserve administration. Central financial institution steadiness sheets – of superior and rising economies – have taken on monumental proportions lately. Now, a few of them separate what can be the suitable tranche for “liquidity administration” (the rationale why there are reserves in liquid and low-risk property, with the aim of stabilization), from one other “funding tranche” (attainable to be allotted in much less liquid however extra worthwhile property).

Many international locations have additionally created SWFs (Sovereign Wealth Funds) to handle the funding tranche of the general public sector’s overseas forex holdings. The seek for diversification helped “non-traditional” reserves.

That is illustrated by Determine 5 – which we took from an April 2 tweet by Brad Setser (from the U.S. CFR – Council on Overseas Relations) – displaying how overseas acquisition of U.S. Treasuries and Businesses has decoupled from official greenback reserves. Brad Seter has lately compiled information suggesting how accumulation of U.S. greenback property by official establishments aside from central banks has grown in weight within the final decade. He remarks that “the massive [current account] surplus international locations (China, the GCC, Russia, Singapore) have giant state sectors that dominate the steadiness of funds”, and that “state asset accumulation outdoors of reserves is, properly, fairly sturdy”.

Determine 5 – drivers of overseas purchases of U.S. Treasuries and Businesses

The fourth gravitational in favor of the greenback can be the absence of rules limiting liquidity and asset availability, together with capital controls. Regardless of the sanctions already utilized in instances comparable to Iran, Venezuela, and Russia, there’s a issue right here for Chinese language bonds in comparison with these in {dollars} and the opposite three main currencies.

Because the world monetary disaster, China has sought to increase the usage of the Renminbi in worldwide commerce and as a reserve asset at different central banks. This was adopted by a proliferation of overseas alternate swap strains with different international locations.

Nonetheless, as we have now beforehand approached (Canuto, 2022b), whereas commerce transactions and reserves by central banks and different world public buyers might reinforce the renminbi’s place instead forex to the greenback, euro, yen, and pound sterling, the qualitative leap towards the internationalization of the Chinese language forex as a reserve forex will solely happen when confidence in its convertibility is ample to persuade unofficial (personal) buyers to maintain reserves denominated in it. It’s not by likelihood that the forex swap strains with China have been little used, whereas these of the international locations with the Federal Reserve have been activated in occasions of must stabilize flows.

By all indications, Chinese language monetary authorities don’t look like contemplating relinquishing controls as a precedence on the instant horizon. They’ll probably search to develop the usage of the renminbi to the extent that this may be completed with out relinquishing controls and, due to this fact, with out the ambition to construct some parallel regime or substitute for the prevailing one. The reserve issuer should settle for that giant quantities of its forex flow into the world and, due to this fact, that overseas buyers have some weight in figuring out home long-term rates of interest and the alternate price.

Final yr, proper after Russia’s invasion of Ukraine, portfolio overseas capital actions into and out of China have been illustrative of what’s at stake and the potential prices for China of dashing out of its present regime. Knowledge launched by the Institute of Worldwide Finance (IIF) revealed an unprecedented giant outflow of portfolio (debt and equities) capital from China within the wake of the Russian invasion of Ukraine and sanctions. On the identical time, such flows remained steady in different rising economies (Canuto, 2022b).

Though later partially reversed, the timing of the phenomenon means that it had some correlation not with home difficulties with the nation’s property sector or different causes however primarily with the struggle in Ukraine and sanctions. Paradoxically, the identical sanctions that stimulated the rise of renminbi on transactions additionally sparked capital actions out of China. Given the magnitudes of repressed home monetary wealth in China, one might guess dramatic outflows would comply with that capital-account liberalization in the hunt for diversification because it occurred in 2015.

Total, one might conclude that the relative dominance of the U.S. greenback seems to be declining however at a really gradual tempo. Occasions since final yr and the coverage strikes talked about right here within the first merchandise have boosted the renminbi as a payment-and-reserve forex however any declaration of “de-dollarization” appears to be untimely.

Could the U.S. greenback “exorbitant privilege” be a “handicap”?

Again within the Sixties, Valéry Giscard d’Estaing, then the French Minister of Finance, coined the time period “exorbitant privilege” to the U.S. greenback place as a main world forex. Such a place permits a rustic to provide money or secure property wanted by the remainder of the world in alternate for items and companies or long-term property.

Extra broadly:

“Nations that problem reserve currencies, particularly the US, have a tendency to learn from what known as an ‘exorbitant privilege’. This broadly refers back to the impact of the worldwide demand for secure property on the reserve forex issuers funding prices, which tends to tilt consumption in direction of the current and results in greater funding. World demand for reserve property additionally tends to understand the forex of reserve issuers. These results unambiguously weaken reserve forex issuers’ present accounts. (…) The estimated coefficient means that for every 10 share factors of world reserves held in its forex, a rustic’s present account steadiness is weakened by about 0.3 % of GDP.” (Cubeddu et al., 2019, p.9).

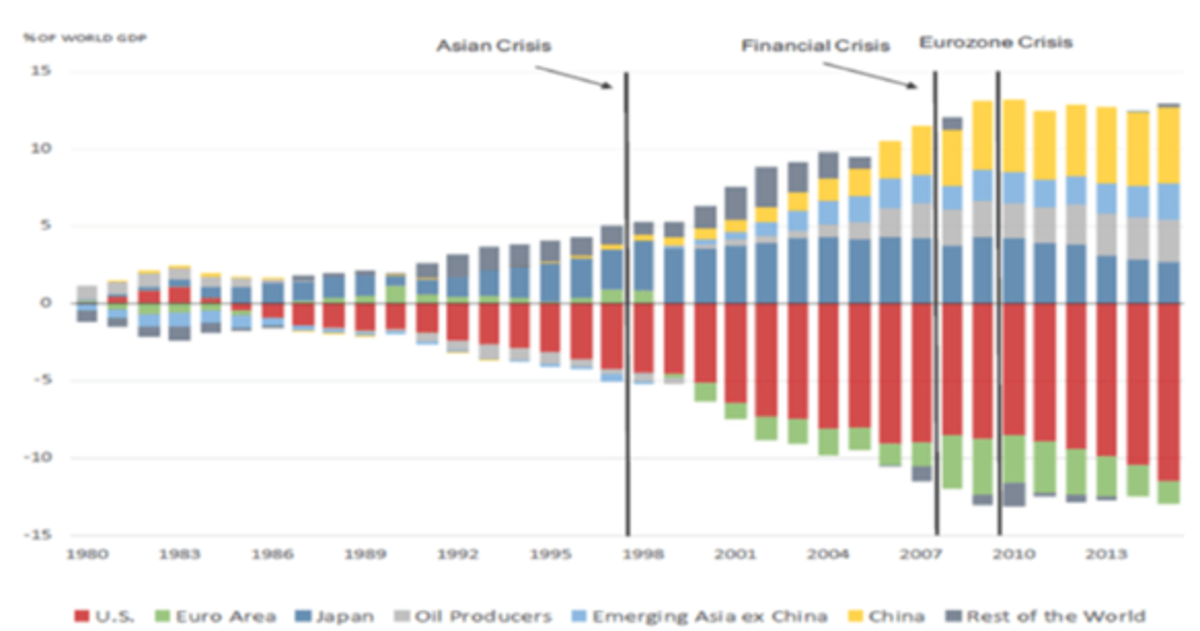

Nation-level mismatches between provide and demand for secure property seem within the evolution of corresponding internet shares of secure overseas property. Determine 6 portrays the U.S. and euro space under the road, as safe-asset suppliers, whereas China, Japan, oil producers, and rising Asia ex-China are internet purchasers above the road. To the extent that the world inventory of secure property strikes upward, cross-border internet purchases of secure property give carriers of the “exorbitant privilege” the next quantity of goods-and-services and funding property from the rest-of-the-world in alternate for these secure property (Canuto, 2020).

Determine 6 – Internet secure positions as a fraction of world GDP

There are these, nevertheless, who see that “bonus” as an “onus”. All of it hinges on whether or not the goods-and-services and funding property “imported totally free”, similar to a sure degree of current- and/or capital-account deficit that the issuer of secure property can incur in alternate for the availability of these property, come along with or changing native manufacturing, no matter whether or not the “safe-asset supplier” runs a surplus or deficit within the different balance-of-payment accounts.

The “onerous” view of the “exorbitant privilege” is offered, as an illustration, by Pettis (2022), for whom it “permits lots of the world’s largest economies to make use of a portion of American demand to resolve poor home demand and gasoline home progress, for which the US financial system should then make up by rising its family or fiscal debt. These economies, in different phrases, can improve their worldwide competitiveness by decreasing the relative share households retain of what they produce. They’ll then run the massive surpluses wanted to steadiness their home demand deficiencies whereas maintaining progress excessive. That is the type of beggar-thy-neighbor commerce coverage that Keynes most urgently warned in opposition to.”

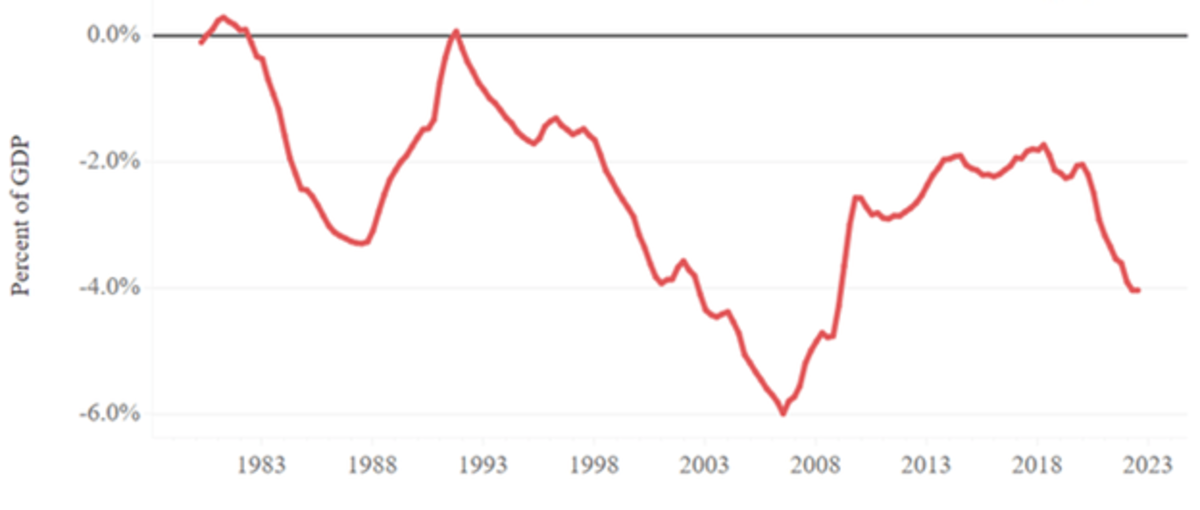

Pettis’ argument, nevertheless, just isn’t framed solely regarding the steadiness related to the availability of secure property, which he blurs into the broader problem of U.S. current-account deficits (Determine 7): “With out the widespread use of the US greenback because the mechanism that permits world imbalances to be absorbed by the US financial system, these imbalances can not exist.”

Determine 7 – U.S. present account

Extreme or inadequate current-account balances are higher approached by means of the IMF’s methodology of analysis of “current-account imbalances” relative to international locations’ “fundamentals” in its annual “exterior sector report” (IMF, 2022) (Canuto, 2020). The “exorbitant privilege” shouldn’t be confounded with occasional international locations’ shortcomings in acquiring full employment or environment friendly allocation of assets.

Conclusion

However the on-going drive by international locations – China specifically – for the next plurality of fundamental currencies within the worldwide financial system, elevating the usage of renminbi, “de-dollarization” appears certain to be partial and restricted. Greater velocity and depth of such a change would require a metamorphosis of China’s regulatory and coverage regime, for which the nation almost definitely is not going to have the will to implement on the present historic juncture. Whereas the euro has remained principally a regional reserve forex, the U.S. might retain its “exorbitant privilege” by means of provision of U.S. greenback secure property for longer.

References

Akinci, O.; Benigno, G.; Pelin, S.; and Turek, J. (2023). The Greenback’s Imperial Circle, Federal Reserve Financial institution of New York Liberty Avenue Economics, March 1.

Arslanalp, S.; Eichengreen, B.J.; and Simpson-Bell, C. (2022). The Stealth Erosion of Greenback Dominance: Energetic Diversifiers and the Rise of Nontraditional Reserve Currencies, Worldwide Financial Fund, IMF Working Paper No. 2022/058, March 24.

Caballero, R.J., Farhi, E., and Gourinchas, P.-O. (2020). World imbalances and coverage wars on the zero-lower certain, January 16.

Canuto, O. (2020). World imbalances, coronavirus, and secure property, Coverage Heart for the New South, August 10.

Canuto, O. (2021). China’s Renminbi Wants Convertibility to Internationalize, , July 28.

Canuto, O. (2022a). Quantitative Tightening and Capital Flows to Rising Markets, Coverage Heart for the New South, PB – 42/22, June.

Canuto, O. (2022b). Greenback dominance will stay, Coverage Heart for the New South, March 20.

Cubeddu, L.M.; Krogstrup, S.; Adler, G.; Rabanal. P.; Dao, M.; Hannan, S.A.; Juvenal, L.; Buitron, C.O.; Rebillard, C.; Garcia-Macia, D.; Jones, C.; Rodriguez, J.; Chang, Okay.S.; Gautam, D.; Wang, Z.; and Li, N. (2019). The Exterior Stability Evaluation Methodology: 2018 Replace, Worldwide Financial Fund, IMF Working Paper No. 2019/065, March 19.

Locket, H. and Leng, C. (2023). Renminbi’s share of commerce finance doubles since begin of Ukraine struggle, Monetary Occasions, April 11.

Pettis, M. (2022). Will the Chinese language renminbi substitute the US greenback?, Assessment of Keynesian Economics, Vol. 10 No. 4, Winter, pp. 499-512.

Standing of US Greenback as World Reserve Forex and Change Charges: Sluggish Lengthy-Time period Decline on Monitor, Wolf Avenue, April 2 .

Stell, B. and Della Rocca, B. (2023). CFR World Imbalances Tracker, CFR, January 19.

Otaviano Canuto, based mostly in Washington, D.C, is a senior fellow on the Coverage Heart for the New South, a professorial lecturer of worldwide affairs on the Elliott Faculty of Worldwide Affairs – George Washington College, a nonresident senior fellow at Brookings Establishment, a professor affiliate at UM6P, and principal at Heart for Macroeconomics and Growth. He’s a former vice-president and a former government director on the World Financial institution, a former government director on the Worldwide Financial Fund and a former vice-president on the Inter-American Growth Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics at College of São Paulo and College of Campinas, Brazil.

[ad_2]