[ad_1]

Counting on GDP may present a deceptive impression of regained momentum.

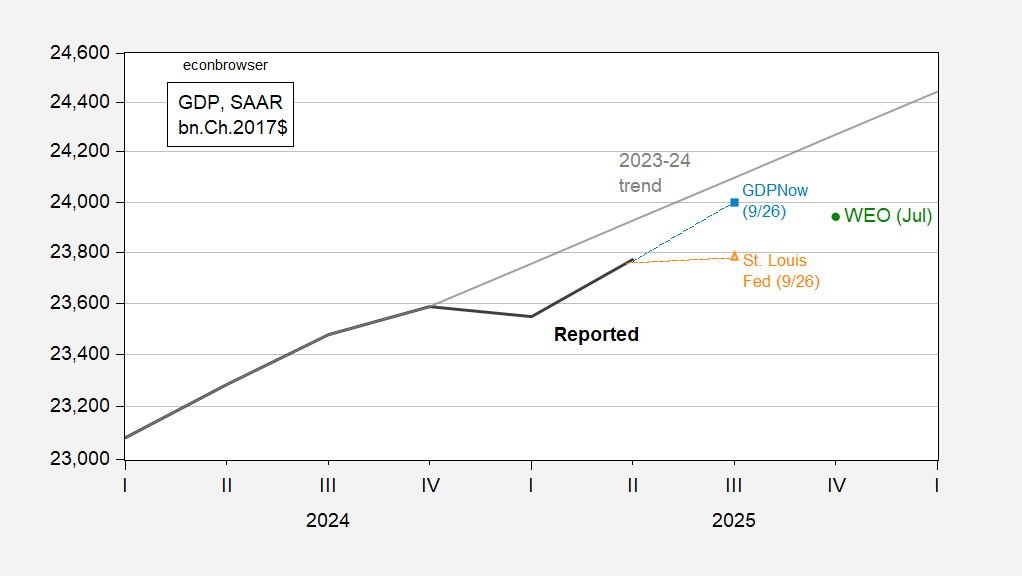

Determine 1: GDP (daring black), 2023-24 stochastic pattern (grey), GDPNow (9/26) (gentle blue sq.), St. Louis nowcast (9/26) (orange triangle), IMF WEO (July) (inexperienced circle). Supply: Atlanta Fed, St. Louis Fed, IMF World Financial Outlook, July replace, creator’s calculations.

One could be tempted to see a return to the pre-Trump GDP trajectory (particularly if one depends on the Atlanta Fed’s nowcast), nevertheless it’s not clear to me this path is sustainable, particularly once we think about mixture demand’s evolution, as measured by last gross sales to non-public home purchasers, what Jason Furman refers to as “Core GDP”. I feel that notably in these instances, specializing in this measure is advisable, given the measurement points attendant with imports and inventories within the front-running of tariffs.

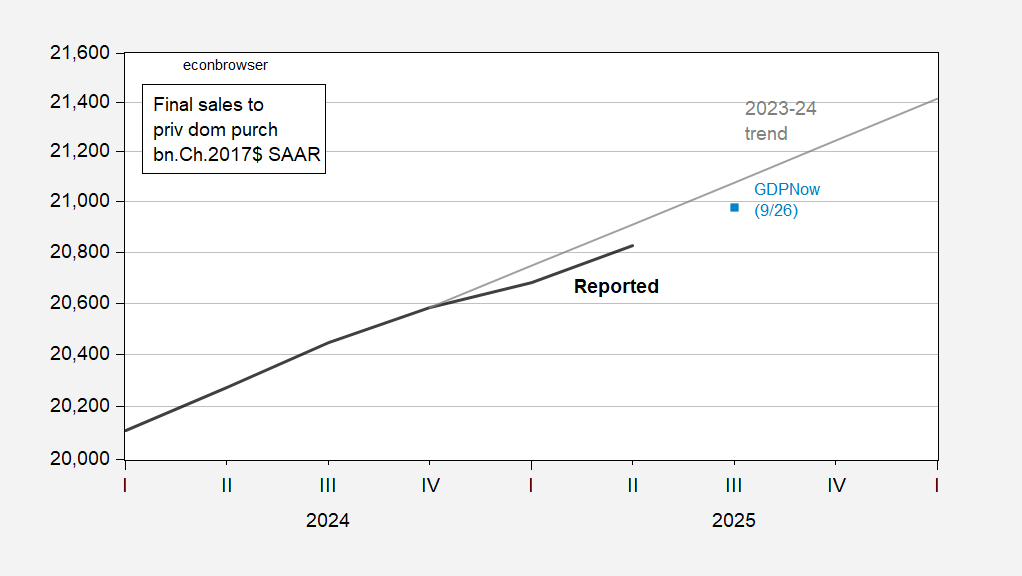

Determine 2: Remaining gross sales to non-public home purchasers (daring black), GDPNow nowcast of 9/26 (gentle blue sq.), 2023-24 stochastic pattern (grey), all in bn.Ch.2017$ SAAR. Supply: BEA, Atlanta Fed, creator’s calculations.

As this graph demonstrates, even with the pretty upbeat Atlanta Fed nowcast, personal home mixture demand has not returned to its pre-shock trajectory.

[ad_2]