[ad_1]

In the present day, we current a visitor submit written by David Papell and Ruxandra Prodan-Boul, Professor of Economics on the College of Houston and Economics Lecturer at Stanford College.

The Federal Open Market Committee (FOMC) adopted its first Assertion on Longer-Run Objectives and Financial Coverage Technique in January 2012. The targets of the assertion had been to mitigate deviations of inflation from its 2 % goal and deviations of employment from its most degree. In August 2020, the FOMC adopted a far-reaching revised assertion. The revised assertion contained two main modifications from the unique assertion. The FOMC would implement Versatile Common Inflation Concentrating on (FAIT) the place, “following durations when inflation has been operating persistently beneath 2 %, applicable financial coverage will seemingly goal to realize inflation reasonably above 2 % for a while” and coverage selections would try to mitigate shortfalls, somewhat than deviations, of employment from its most degree. In August 2025, the FOMC deserted FAIT in favor of Versatile Inflation Concentrating on (FIT) and downplayed shortfalls, primarily returning to the 2012 Assertion.

In our paper, “Different Coverage Guidelines and Publish-Covid Fed Insurance policies,” lately printed on-line in The Economists’ Voice, we analyze Fed insurance policies between 2020:Q3 and 2027:This fall utilizing a wide range of coverage guidelines and examine the coverage rule prescriptions with the federal funds price (FFR) between 2020:Q3 and 2025:Q2 utilizing the newest knowledge and with the projected FFR between 2025:Q3 and 2027:This fall utilizing inflation and unemployment projections from the June 2025 Abstract of Financial Projections (SEP). We present that FAIT was irrelevant and shortfalls had been comparatively unimportant. On this submit, we focus on the paper and lengthen the outcomes by means of 2028:This fall through the use of inflation, unemployment, and FFR projections from the September 2025 SEP.

The 2020 Assertion was adopted following a decade of low development, low inflation, and low rates of interest. The 2025 Assertion was adopted in a really completely different surroundings. Whereas there’s nice uncertainty concerning the future path of the financial system, returning to the world between 2012 and 2019 seems unlikely. Changing FAIT with FIT and including ambiguity to shortfalls look like steps in the suitable route.

Beginning with Taylor (1993), coverage guidelines have change into the usual technique for analyzing Fed coverage. The Taylor (1999) and Yellen (2012) balanced strategy rule with an unemployment hole is as follows,

the place Rt is the extent of the short-term federal funds rate of interest prescribed by the rule, πt is the inflation price, πLR is the two % goal degree of inflation, ULRt is the speed of unemployment within the longer run, Ut is the present unemployment price, and rLRt is the impartial actual rate of interest that’s in line with inflation equal to the goal degree of inflation and unemployment equal to the speed of unemployment within the longer run. The Taylor (1993) model of the rule has a coefficient of 1.0 on the unemployment hole.

The balanced strategy (shortfalls) rule mitigates employment shortfalls as an alternative of deviations by having the FFR solely reply to unemployment if it exceeds longer-run unemployment,

If unemployment exceeds longer-run unemployment, the FFR prescriptions are equivalent to these with the balanced strategy rule. If unemployment is beneath longer-run unemployment, low unemployment doesn’t contribute in direction of the FOMC elevating the FFR.

The balanced strategy (FAIT) rule is,

the place rLRt is the impartial actual rate of interest, πLR = 2, Mod represents the speed of inflation reasonably above 2 % for a while within the revised assertion and is the speed of unemployment within the longer run. The FAIT guidelines differ from the unique guidelines as a result of the prescribed FFR doesn’t improve till inflation is reasonably above 2 % for a while.

The balanced strategy (constant) rule is,

the place is the impartial actual rate of interest, = 2, and πMod represents the speed of inflation reasonably above 2 % for a while within the revised assertion. The constant guidelines mix shortfalls and FAIT.

In line with the coverage guidelines in Equations (1) – (4), the FFR absolutely adjusts at any time when the goal FFR modifications. We additionally specify inertial variations of our coverage guidelines primarily based on Clarida, Gali, and Gertler (1999) and Sack and Wieland (2000),

the place p = 0.85 is the diploma of inertia and is the goal degree of the federal funds price prescribed by every of the coverage guidelines in Equation (1) – (4). Inertial guidelines have the benefit that they decrease the variance of the FFR in response to modifications in inflation and unemployment gaps. equals the speed prescribed by the rule whether it is constructive and nil if the prescribed price is damaging.

The outcomes for the non-inertial and inertial balanced strategy guidelines are reported in Determine 1. For the reason that Taylor rule prescriptions are just like the balanced strategy rule prescriptions, we solely embrace the latter within the submit. Annual Core PCE inflation was between 1.3 and 1.5 % from September 2020 by means of March 2021 and rose to three.1 % in June 2021. Since 3.1 % is clearly greater than reasonably above 2 %, there isn’t any distinction between the prescriptions with the unique and FAIT guidelines after March 2021. As well as, the prescriptions from the unique and FAIT guidelines are damaging between September 2020 and March 2021 and set equal to zero by the ELB. Taken collectively, prescriptions from unique guidelines are equivalent to prescriptions from FAIT guidelines. Determine 1 additionally reviews the outcomes for the shortfalls and constant guidelines. For the reason that prescriptions from the FAIT guidelines are equivalent to the prescriptions from the unique guidelines, the prescriptions from the constant guidelines are equivalent to the prescriptions from the shortfalls guidelines.

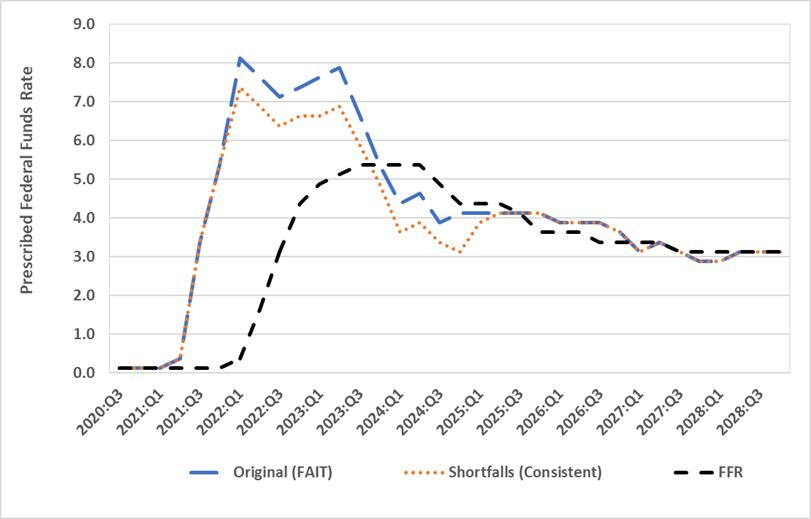

Determine 1. Unique (FAIT) and Shortfalls (Constant) Coverage Rule Prescriptions

Panel A. Non-Inertial Balanced Method Guidelines

Panel A reviews the outcomes from the non-inertial guidelines. With both unique (FAIT) or shortfalls (constant) guidelines, the prescribed FFR is bigger than the precise FFR from 2021:Q2 to 2023:Q3 and fewer than the precise or projected FFR from 2023:This fall to 2025:Q2. Beginning in 2025:Q3, the prescribed and projected FFR’s are very comparable by means of 2028:This fall. Prescriptions from the unique guidelines are equal to these from the shortfalls guidelines between 2020:Q3 and 2021:This fall and between 2025:Q2 and 2028:This fall as a result of unemployment is bigger than or equal to longer-run unemployment. Between 2022:Q1 and 2025:Q1, prescriptions from the shortfalls guidelines are decrease than these from the unique guidelines as a result of unemployment is lower than longer-run unemployment.

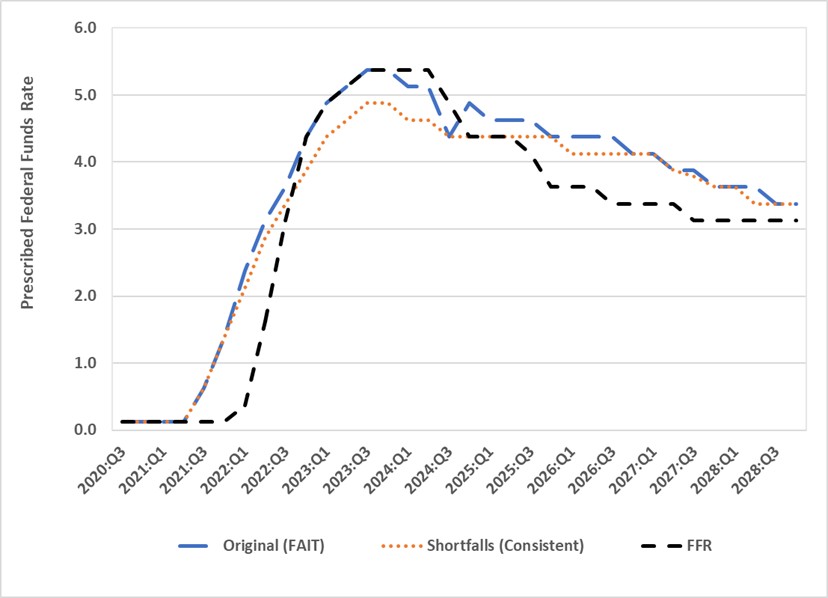

Panel B reviews the outcomes from the inertial guidelines. Whereas the prescribed FFR is greater than the precise FFR from 2021 by means of 2022, the variations are a lot smaller than with the non-inertial guidelines. Prescriptions from the unique guidelines are usually nearer to the FFR than these from the shortfalls guidelines in 2023 and 2024. Beginning in 2025:Q3, the FFR projections are persistently beneath the coverage prescriptions by means of 2028:This fall.That is very completely different than with the non-inertial guidelines, the place the prescribed and projected FFR’s are very comparable.

Determine 1. Unique (FAIT) and Shortfalls (Constant) Coverage Rule Prescriptions

Panel B. Inertial Balanced Method Guidelines

This submit written by David Papell and Ruxandra Prodan-Boul.

[ad_2]