[ad_1]

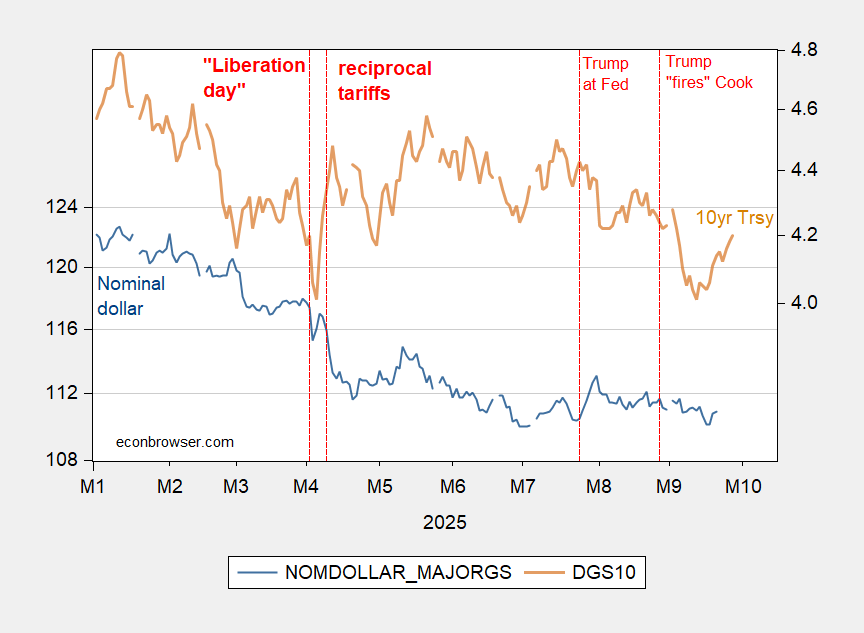

Some folks argue the concurrent greenback decline and Treasury yield incrase was attributable to liquidity points as repicing occurred in opposition to a backdrop of a rising share of worth delicate Treasury holders. Others that it was a flight away from the US greenback property spurred by tariff uncertainty (see a dialogue right here). Right here’s the image folks know, the greenback vs. US Treasurys:

Determine 1: Nominal greenback in opposition to superior economies currencies (blue, left scale), and 10 yr US Treasury yield, % (tan, proper scale). Supply: Federal Reserve, Treasury, through FRED.

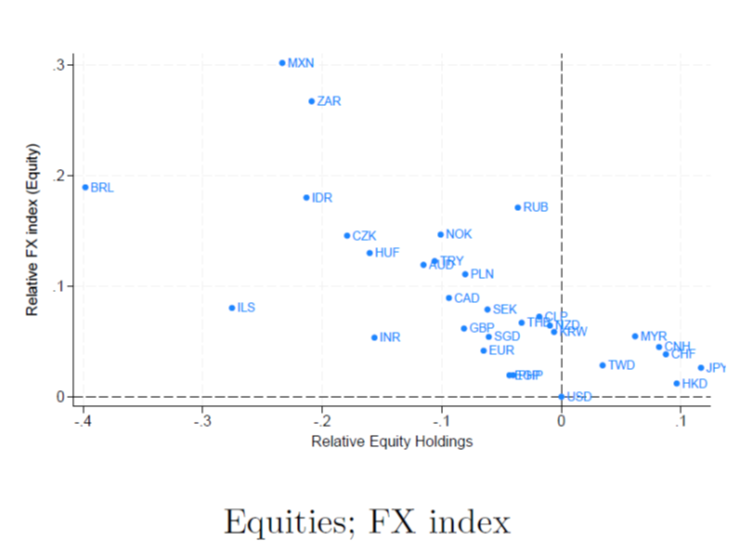

And listed here are two graphs from Helene Rey and Vania Stavrakeva, “Deciphering Turbulent Episodes in Worldwide Finance”, keynote offered on the Asian Financial Coverage Discussion board (Singapore, 2025). (My dialogue right here).

The primary is the response of the trade charge to fairness flows in the course of the pandemic. The foreign currency weakened as imputed fairness flows moved to the US.

Supply: Rey, Stravakeva (2025).

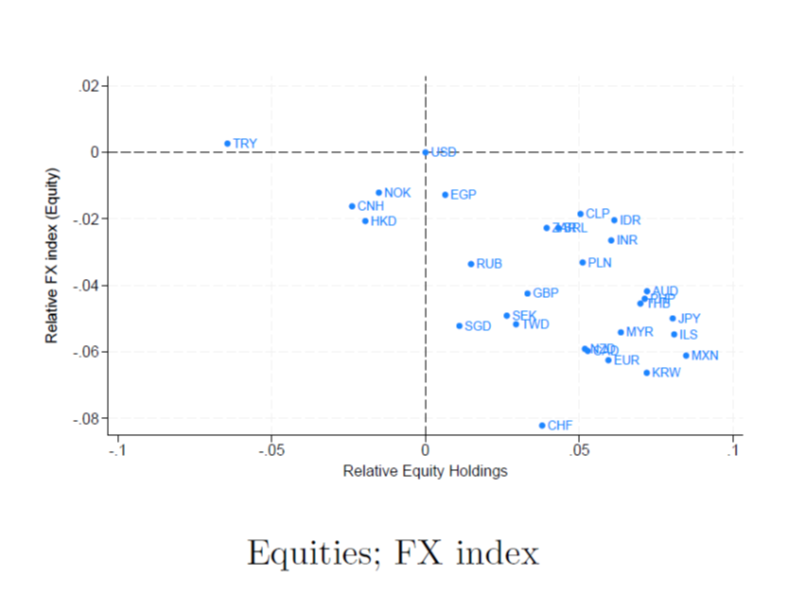

In distinction, in 2025 round “Liberation Day”, different currencies strengthened as imputed fairness flows moved out of the US.

Supply: Rey, Stravakeva (2025).

So, whereas I don’t low cost fully the thought of illiquidity within the Treasury market as a driver of the rise in Treasury yields round “Liberation Day”, it appears to me that at the least a part of the shift post-“Liberation Day” is because of the decline within the confidence within the greenback. Whereas the correlation in modifications within the greenback’s vale and within the Treasury yield have re-asserted itself, it’s fascinating that in Determine 1, the hole that widened within the ranges has persevered.

[ad_2]