[ad_1]

That is Bare Capitalism fundraising week. 101 donors have already invested in our efforts to fight corruption and predatory conduct, significantly within the monetary realm. Please be a part of us and take part through our donation web page, which reveals methods to give through test, bank card, debit card, PayPal. Clover, or Sensible. Examine why we’re doing this fundraiser, what we’ve completed within the final 12 months,, and our present objective, strengthening our IT infrastructure.

Yves right here. We haven’t executed a “How’s your financial system?” reader question in fairly some time. The newest GDP revision suggests it is likely to be helpful to get some sightings. Even when the plural of anecdata just isn’t knowledge, it might probably make sense of issues that don’t appear so as to add up.

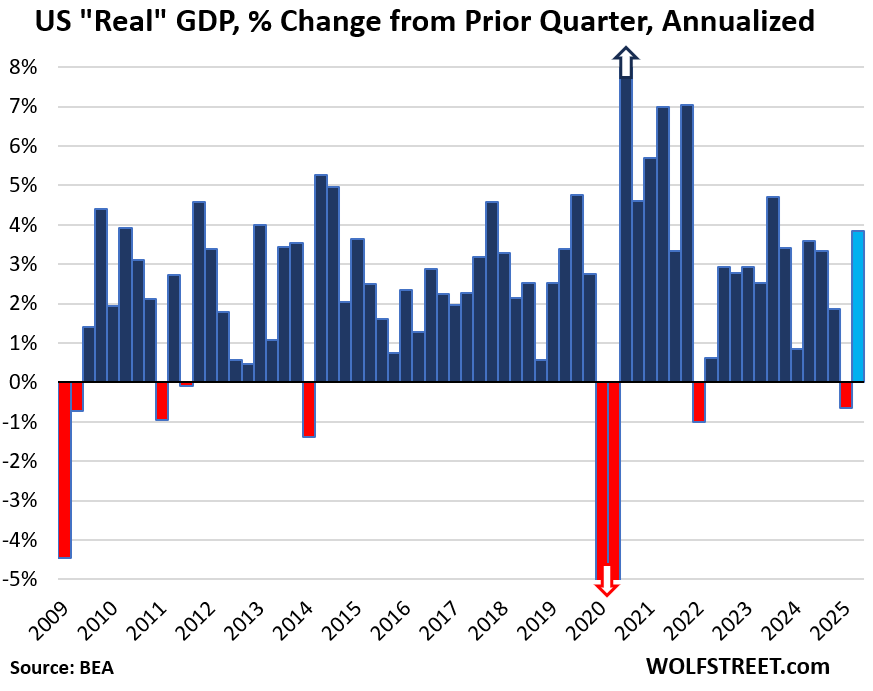

The large anomaly right here is the now-very-peppy 3.8% second quarter GDP, now revised two occasions upward from its unique 3% stage. That stands in stark distinction with anemic jobs progress. It additionally appears inconsistent with many studies, each within the press and from readers, of many small companies struggling bigly from tariffs, making them unable to promote their wares at something like their former worth factors, having nice issue discovering US sources, and seeing their revenues shrink to the purpose of vanishing.

Equally, progress within the US has more and more been assist up by spending on the very high of the earnings chain. But there are indicators of lower than strong well being there, from luxurious distributors faring badly to a collapse in artwork gross sales.

Maybe what’s going on within the financial system parallels the inventory market, with averages propped by ginormous AI valuations at a only a few corporations, together with ginormous AI “capital funding” which as Ed Zitron has chronicled intimately, has produced virtually bupkis in the best way of revenues. AI is one sector with superheated exercise. Are there different very robust pockets that would greater than compensate for what looks like approach an excessive amount of lackluster exercise?

By Wolf Richter, editor at Wolf Avenue. Initially revealed at Wolf Avenue

Authorities consumption and inventories had been an even bigger drag although. All adjusted for inflation.

Again on July 30, the “advance estimate” of GDP for the second quarter confirmed 3.0% progress, held down by anemic client spending progress and plunging inventories. The “second estimate,” launched on August 28, revised GDP progress for Q2 larger to three.3%.

Immediately, the “third estimate” of Q2 GDP revised Q2 GDP progress to three.8%, the quickest progress since Q3 2023, pushed largely by an enormous up-revision of client spending. This 3.8% price of progress is within the scorching zone for the US, whose common GDP progress over the previous 10 years is simply over 2%. All progress figures are adjusted for inflation.

The “first estimate” of GDP progress is the one which will get all the eye within the media. The revisions are usually not the main target of any consideration. For that purpose, I’ll examine immediately’s “third estimate” to the “first estimate,” partially as a result of the up-revisions had been so huge and cumulative.

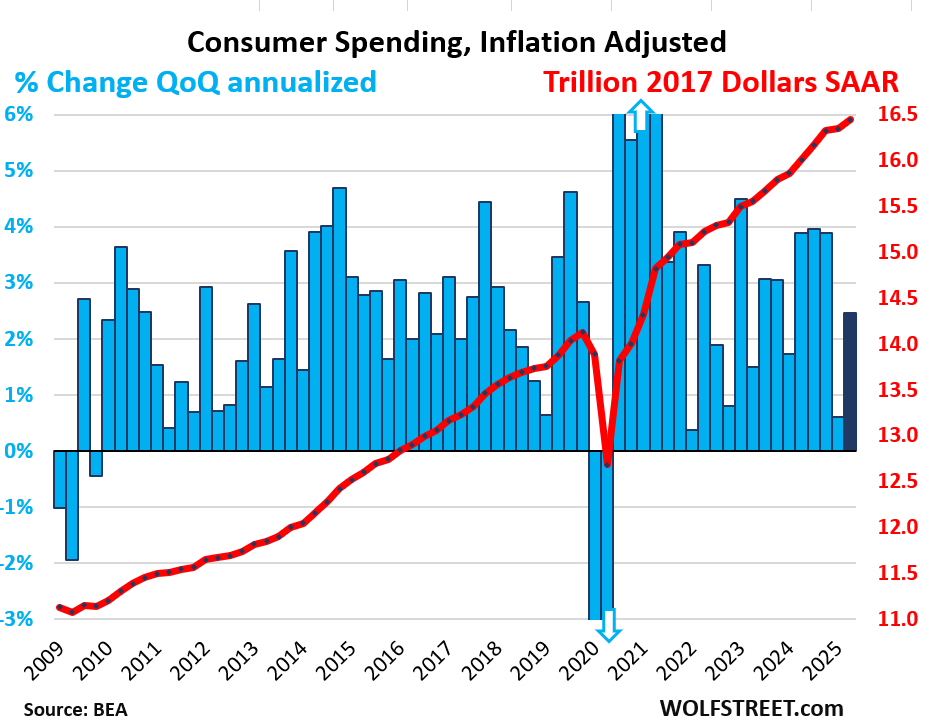

Client spending progress was revised as much as +2.5% in Q2. The primary estimate had pegged client spending progress at a worrisomely anemic 1.4%, the second estimate at 1.6%. Immediately’s huge up-revision to +2.5%, practically doubling the expansion price of the primary estimate, was the most important contributor to the up-revision of general GDP progress (all adjusted for inflation).

This 2.5% is wholesome progress in client spending. The purple line reveals the annualized client spending in 2017 {dollars} (proper scale). The blue columns present the expansion price in p.c (left scale).

Non-public fastened funding was revised to a progress price of 4.4%, from the dreadfully anemic 0.4% within the first estimate. Immediately’s up-revision considerably contributed to the up-revision of general GDP progress:

- Funding in tools was revised as much as +8.5%

- Funding in mental property was revised as much as +15.0%.

- Funding in constructions had plunged by 10.3% within the first estimate. This plunge was lowered to -7.5% immediately.

However residential fastened funding (resembling development of single-family and multifamily properties) was pegged within the first estimate at a drop of -4.6%; this drop elevated to -5.1% in immediately’s third estimate, and lowered the up-revision of personal fastened funding.

Revisions That Pushed the Different Manner v. First Estimate:

Internet exports (exports minus imports) had been revised decrease, they worsened:

- Imports plunged rather less (-29.3%) than the primary estimate (-30.3%); imports subtract from GDP.

- Exports fell by 1.8%, similar price as the primary estimate. Exports add to GDP.

Authorities consumption shrank by 0.1% (federal, state, and native governments mixed), in comparison with progress of 0.4% within the first estimate.

The plunge in personal inventories worsened, and deducted 3.44 proportion factors from GDP progress, versus 3.17 proportion factors within the first estimate. Inventories had soared in Q1 on tariff-frontrunning, and in Q2 they undid a few of that improve.

What Slowdown?

The robust Q2 progress got here after the explosion of imports on tariff-frontrunning had knocked Q1 GDP progress into the destructive (-0.6%). Client spending progress in Q1 was additionally weak. So there have been a variety of considerations about progress. And the primary estimate of Q2 client spending progress (+1.4%) did nothing to alleviate these considerations.

However the revised Q2 progress figures, particularly the up-revisions of client spending again into the wholesome vary, ought to relieve these anxieties.

And Q3 client spending to this point seems fairly good, as indicated by robust retail gross sales in July and August. So perhaps the look forward to the downward spiral of the financial system – regardless of lowered authorities spending – could must be prolonged slightly additional?

[ad_2]