[ad_1]

First appeared at Coverage Heart for the New South

Chinese language financial figures launched because the starting of August have confirmed a slowdown in its progress. New Omicron coronavirus outbreaks within the context of Covid-zero coverage, the housing droop and warmth waves have been holding up the tempo of the economic system.

China’s present progress slowdown is an extra step within the trajectory of regularly declining charges that has accompanied the “nice rebalancing” because the starting of the 2010s. One main distinction now’s the notion of exhaustion of waves of overinvestment in actual property and infrastructure as a lever, as in comparison with three earlier moments because the starting of the final decade.

China’s 2022 Financial Development Deceleration

Chinese language financial figures launched because the starting of August confirmed a slowdown in its progress. New Omicron coronavirus outbreaks within the context of Covid-zero coverage, the housing droop and warmth waves have been holding up the tempo of the financial restoration.

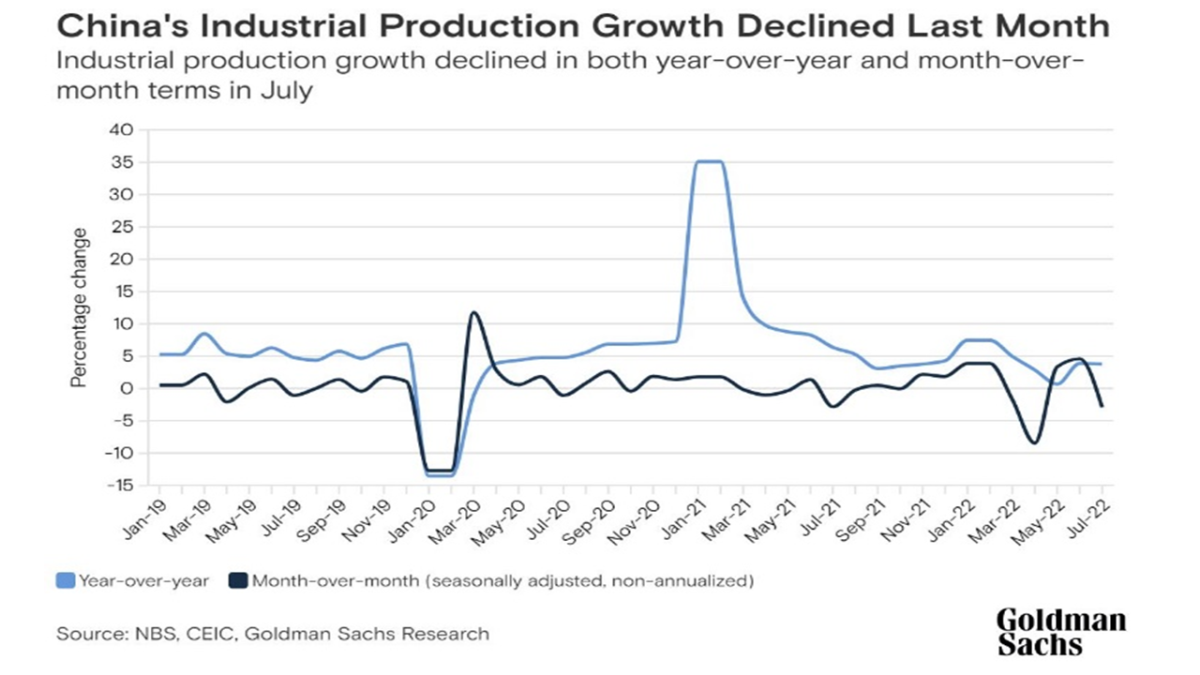

The economic system began the 12 months with a robust momentum in January-February, however destructive shocks led Gross Home Product (GDP) to have contracted by an estimated (seasonally adjusted annual) fee of 5.4% q/q within the second quarter. GDP progress estimates by a number of worldwide banks for the world’s second-largest economic system this 12 months have been just lately revised all the way down to ranges between 2.5 and three.3%. Industrial manufacturing grew simply 3.8% in July from a 12 months earlier, nicely under anticipated 4.5% (Figure 1).

Determine 1

A very sizzling and dry summer season is stressing power provides and resulting in manufacturing cuts in sure provinces and in some energy-intensive sectors.

The disaster in China’s actual property sector continues to undermine financial efficiency. Housing is a crucial part of mounted funding. It grew by simply 5.7% within the first seven months of the 12 months, in comparison with the identical interval in 2021. Final 12 months, that quantity was 10.3% larger year-on-year from July on.

Property gross sales are anticipated to say no about 7% and development begins to fall about 30%, in annual phrases, within the second half of the 12 months (Yao, 2022). The true property slowdown since final 12 months was initially pushed by the coverage selection to cut back builders’ leverage and obtain a long-term goal of housing “for housing, not for hypothesis”. Banks, regulators, and native governments should follow this coverage goal and a common bailout just isn’t on the playing cards. There may be an expectation that changes of steadiness sheets of firms and prospects/suppliers within the sector will happen with out leading to some systemic disaster, regardless of occasional defaults and bankruptcies.

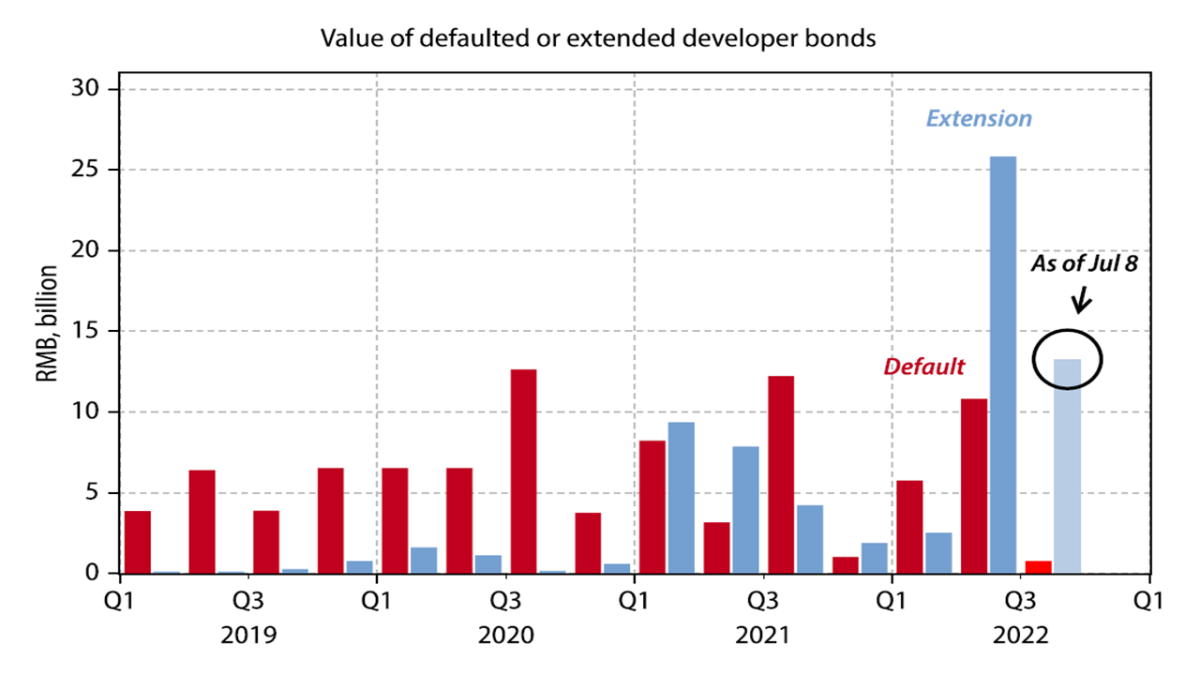

Monetary stress on extremely indebted property builders has elevated over the previous couple of years. Many builders have been unable to refinance in bond markets for many of 2021, and several other main builders have both negotiated reimbursement extensions with collectors or defaulted outright. As proven by Zhang (2022), many collectors have accepted to barter reimbursement extensions forward of potential defaults to present builders extra time to attempt to keep away from them (Determine 2).

Determine 2 – China: developer bond reimbursement bond points are usually not getting higher

In flip, retail gross sales in July have been up simply 2.7% year-on-year, far under expectations of 5%. New outbreaks of Omicron and the dangers of confinement on account of being within the incorrect place and time, along with affecting retail commerce, additionally did so within the case of home tourism. The influence of the Omicron wave to China’s financial progress was vital, particularly in areas topic to COVID associated lockdowns.

Since 2020, family consumption has remained weak, persistently staying under the 2017-19 development (Gatley, 2022). The labor market has been very tender and that doesn’t assist.

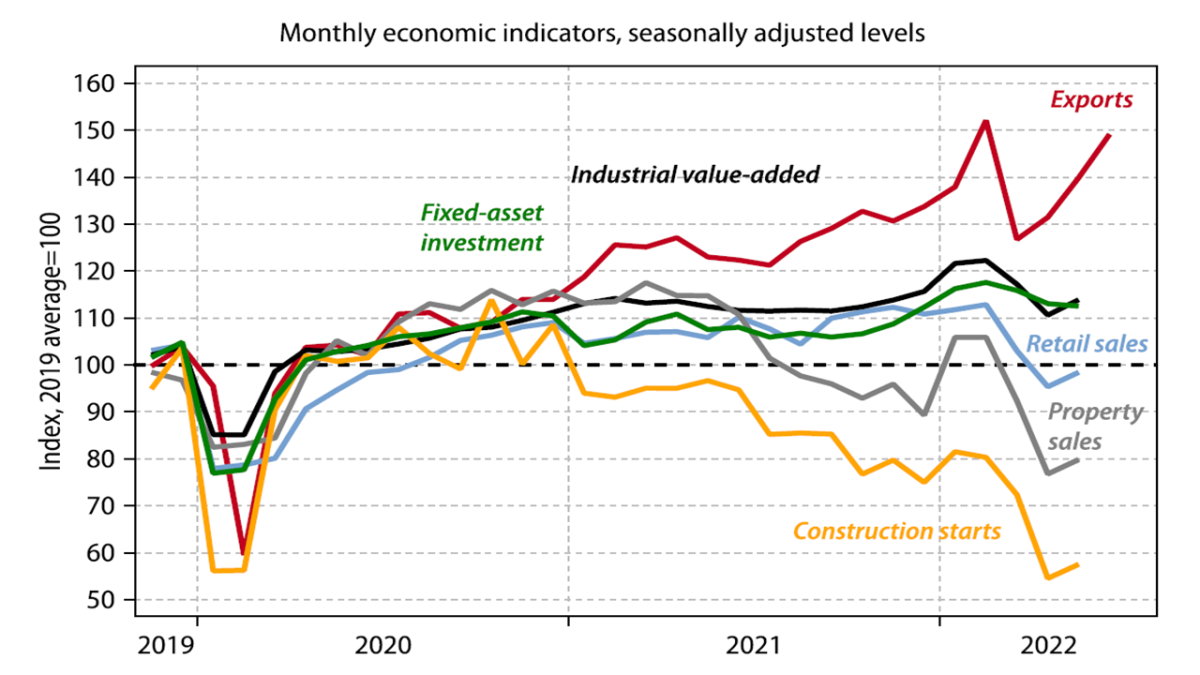

Strictly talking, solely exports maintained a great tempo (Determine 3). Commerce has recovered quicker than home exercise, on condition that the reopening first began with streamlining logistics and transportation, particularly for trade-related actions. Moreover, manufacturing and investments are outpacing consumption and companies, as manufacturing facility reopening has been the next precedence than rest of particular person mobility restrictions.

Manufacturing unit exercise has come again extra shortly than many anticipated, with exports posting their highest progress fee in a 12 months in June, whereas indicators of the buying choices of households have lagged. As approached under, such a sample runs towards the “rebalancing” pursued by Chinese language authorities because the starting of the final decade.

Determine 3 – Exports apart, the rebound of lockdowns has been very lackluster

Regardless of the slowdown, the measures taken by the federal government to counter it may be thought of modest, in contrast to different moments in latest historical past. The Folks’s Financial institution of China minimize two main rates of interest mid-August – the repo rates of interest on one-year and seven-day open market operations – by… 10 foundation factors!

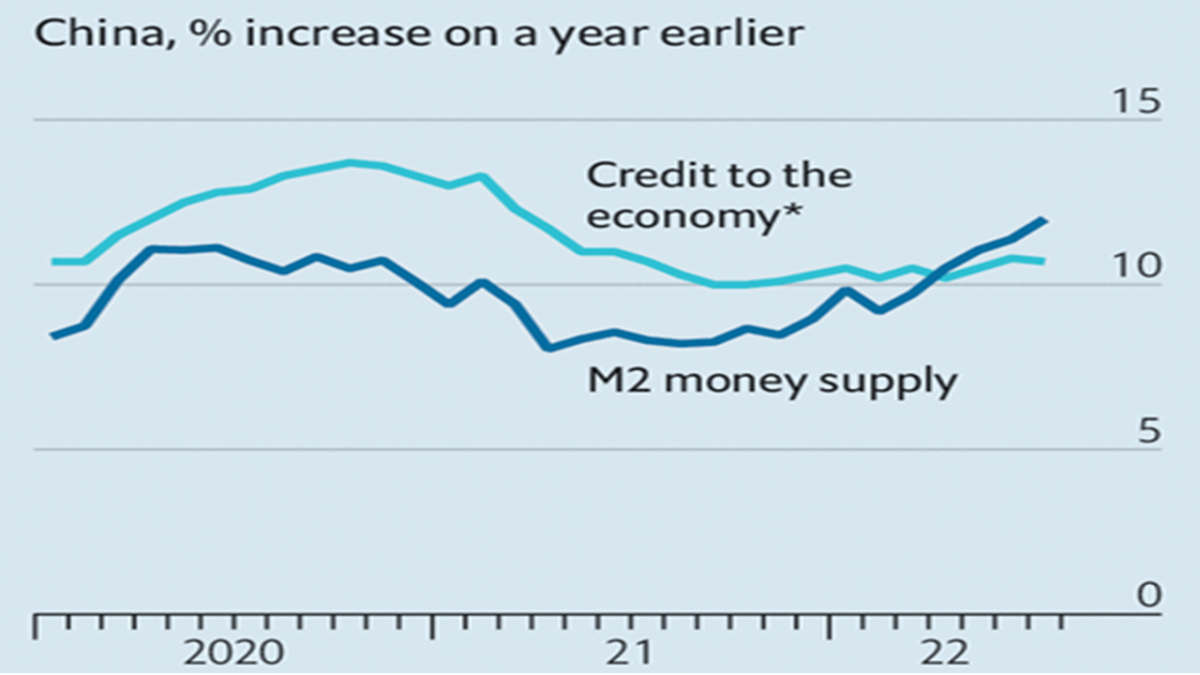

Analysts don’t consider such fee reductions – and different newly introduced incremental fiscal measures – might considerably increase financial progress. The will increase within the financial base (M2) since final 12 months haven’t been accompanied by an equal enlargement of home credit score (Determine 4), denoting the presence of dampening elements underlying the slowdown in investments – actually in the true property space, given the delicate state of affairs of corporations within the sector and of the demand for its merchandise.

Determine 4 – China: credit score and M2 cash provide

China’s Nice Rebalancing

To know the place Chinese language financial progress is, it’s crucial to return to the start of the final decade. In December 2011, once I was one of many vice presidents of the World Financial institution, I attended a ceremony in Beijing by which then-President Hu Jintao made one of many first statements on the necessity for an inevitable “rebalancing” of the Chinese language economic system (Qingfen and Ran, 2011).

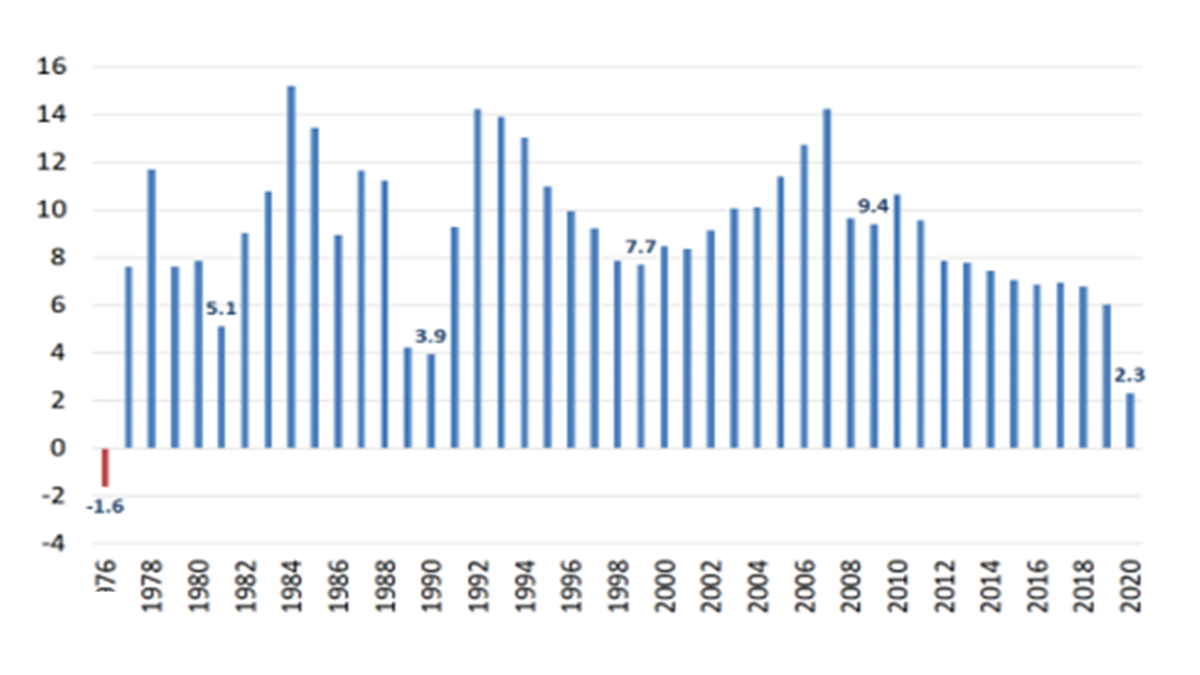

There must be a gradual redirection in direction of a brand new sample of progress, by which home consumption ought to enhance in relation to investments and exports, whereas an effort would even be made to consolidate native insertion up the ladder of worth added in world worth chains. Companies also needs to enhance their weight in GDP relative to manufacturing. China would now not have the double-digit GDP progress charges of earlier a long time (Determine 5), however progress would now not be, as Premier Wen Jiabao had mentioned in 2007, “unstable, unbalanced, uncoordinated and unsustainable”.

Determine 5 – China: annual GDP progress charges

Excessive and sustained GDP growth-rates had been based mostly on elevated investment-to-GDP ratios – which have been solely attainable with low shares of wage revenue and home consumption, in addition to with low-cost and repressed finance (Canuto, 2019a).

One other issue was dynamic markets overseas prepared and able to absorbing an enlargement of Chinese language exports – one thing that would not occur indefinitely, given the dimensions acquired by China’s economic system. The mixture of excessive funding and low home consumption (a flipside of excessive income relative to wages) was solely attainable due to present account surpluses in buying and selling with the remainder of the world.

Rising revenue disparities have been a home flipside of that mannequin, a possible supply of social pressure together with modifications within the exterior setting.

Three mutually reinforcing paths of transformation have been seen forward in 2011, with a structural slowdown of progress on the playing cards.

First, China had accrued massive productiveness will increase by means of transferring sources from low-productivity agriculture actions to trade — a typical function of economies shifting from low- to middle-income ranges (Canuto, 2019b). These good points had, to a big extent, already occurred. On the demographic entrance, the old-age-dependency ratio had began to rise. Beneficial properties in financial effectivity and technological progress – based mostly on absorption of present, imported applied sciences – must be more and more changed with native innovation. The set of second-generation coverage reforms crucial for that will require time, whereas low-hanging fruits, when it comes to productiveness will increase, could be much less obtainable.

As a second path of change, a rebalance within the sector-structure and in aggregate-demand-composition was anticipated. Increased shares of companies and consumption, following rising wages, with a lower in exports, financial savings, and funding ratios-to-GDP, ought to accompany the elevated reliance on home sources of mixture demand.

The revenue hole between coastal areas – the place particular zones have been created and extended- and center and western areas ought to fall because the labor pool shrank. Regardless of decrease GDP progress charges on account of decrease investment-to-GDP ratios and complete issue productiveness will increase tougher to acquire, the favored notion of rising prosperity would in all probability be larger than earlier than, with rising buying energy by the inhabitants.

The third path of structural transformation could be a shift up the worth chain in tradable and non-tradable actions. That ought to underpin the paths of change within the sector construction and in elements of mixture demand. A transition to extra refined manufacturing processes was already being pursued.

Whereas shifting to a much less spectacular progress trajectory, China could be morphing right into a mass-consumer market economic system, mixed with provide capability more and more reliant on progress of “complete issue productiveness”.

Having a transparent roadmap didn’t imply a straightforward journey. Given the low degree of home consumption in GDP (a reality that’s nonetheless current) and, subsequently, the dependence on investments and commerce balances, the transition would run the chance of experiencing an abrupt drop within the tempo of progress, significantly given the context after the disaster 2008-09 world monetary disaster. To allay fears of an abrupt slowdown, waves of credit-driven overinvestment in infrastructure and housing adopted. A second spherical of such overinvestments got here into play in 2015–2017, in response to an actual property downturn and a inventory market decline. As well as, in fact, to the enlargement insurance policies adopted throughout the pandemic disaster in 2020.

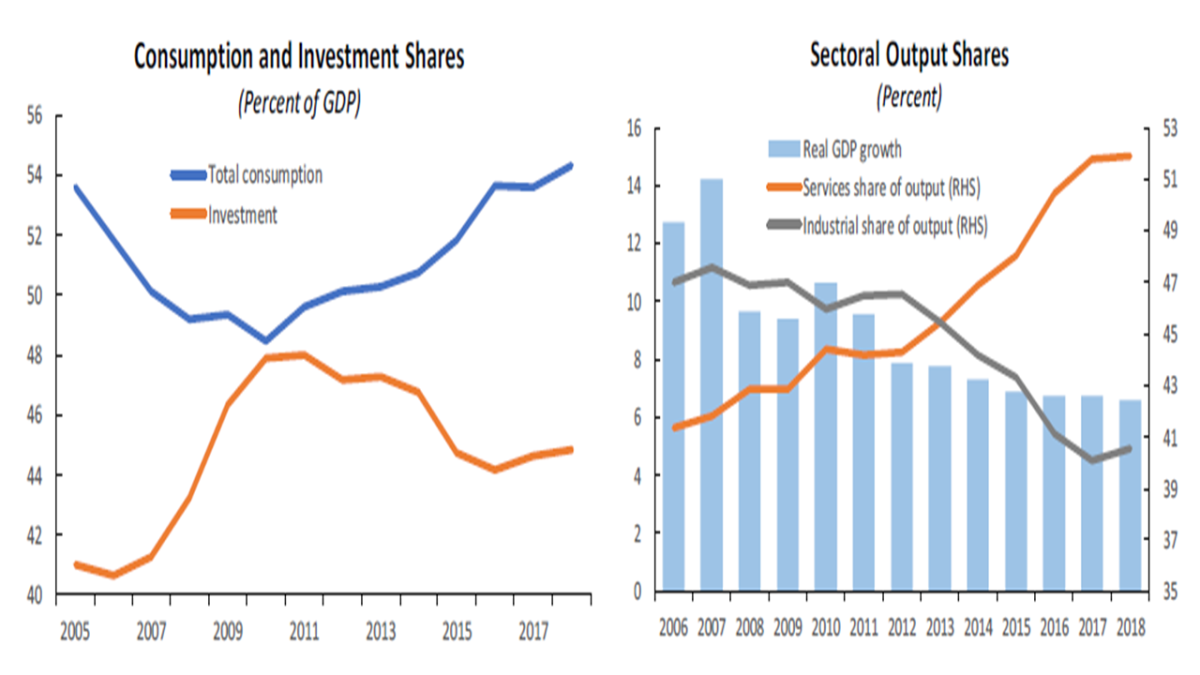

Certainly, a decline in Chinese language GDP progress charges passed off regularly to six% in 2019, in direction of ranges such because the 4% anticipated after the pandemic (Determine 5). And the gradual rebalancing towards lowering dependence on funding and commerce surpluses could be seen in Figures 6 and seven.

The left-hand panel of Determine 6 depicts how home demand began shifting away from funding and in direction of consumption, whereas the right-hand panel, on the manufacturing facet, reveals companies outgrowing manufacturing, because the construction of manufacturing turned extra advanced, built-in, and with larger worth added.

Nevertheless, and that may be a problem, the transition towards a much less investment- and export-dependent progress mannequin has been going down from a place to begin of exceptionally low consumption-to-GDP ratios as in comparison with the remainder of the world. No surprise rebalancing towards a consumption-based progress mannequin was anticipated to be solely regularly pursued, as GDP progress charges would possibly collapse, fairly than slide down. The change of progress sample would require time-intensive structural reforms.

Determine 6 – China’s rebalancing towards consumption and companies

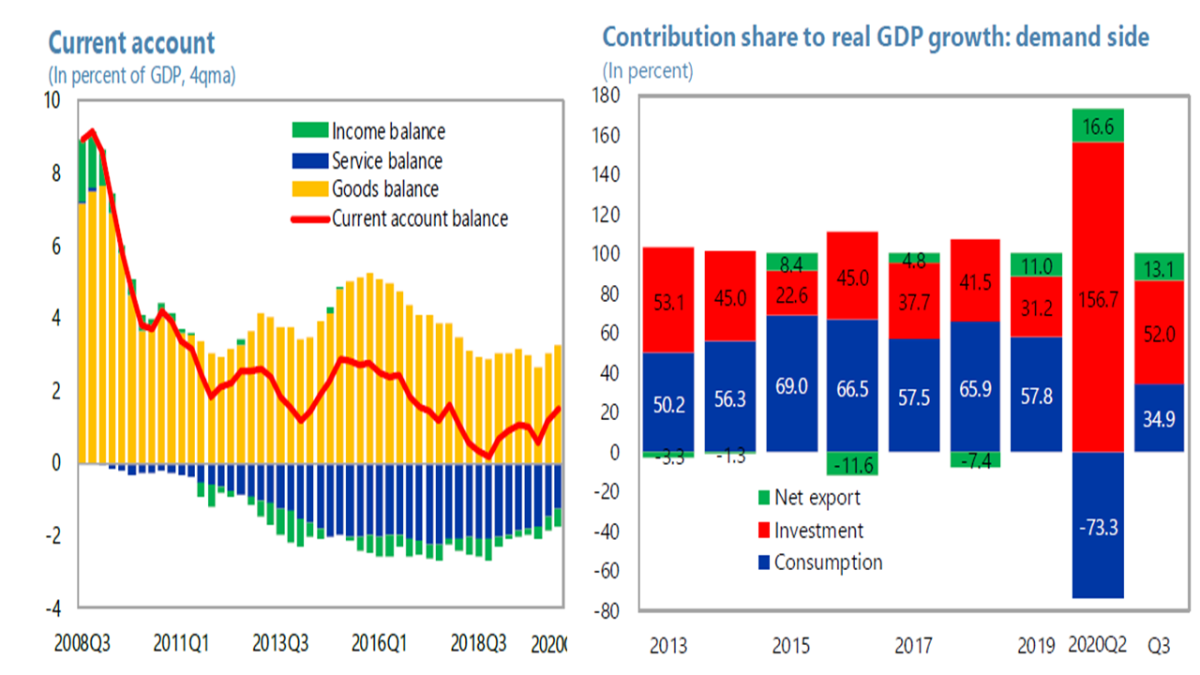

The left-hand panel of Determine 7 shows the lower of the function performed by current-account surpluses with the remainder of the world, as a part of China’s progress rebalancing. 2020 was a degree off the curve. China’s current-account surplus narrowed in Q1 however widened once more to 1.5% of GDP over 4 quarters ending in Q3, reflecting a stronger commerce steadiness and a collapse in outbound tourism. The best-hand panel reveals how rebalancing in direction of consumption regressed as public funding drove the 2020 first part of after-pandemic restoration… and the re-opening after the Q1 lockdown favored industrial exercise.

Determine 7 – China’s rebalancing towards much less export-dependence

A query laborious to reply issues how the gradual evolution of GDP progress and modifications of composition since 2010 would have been within the absence of the waves of infrastructure and actual property overinvestment, counting solely on the “rebalancing”, that’s, a rise in wages and mass home consumption and the transition to higher weights of companies and better know-how.

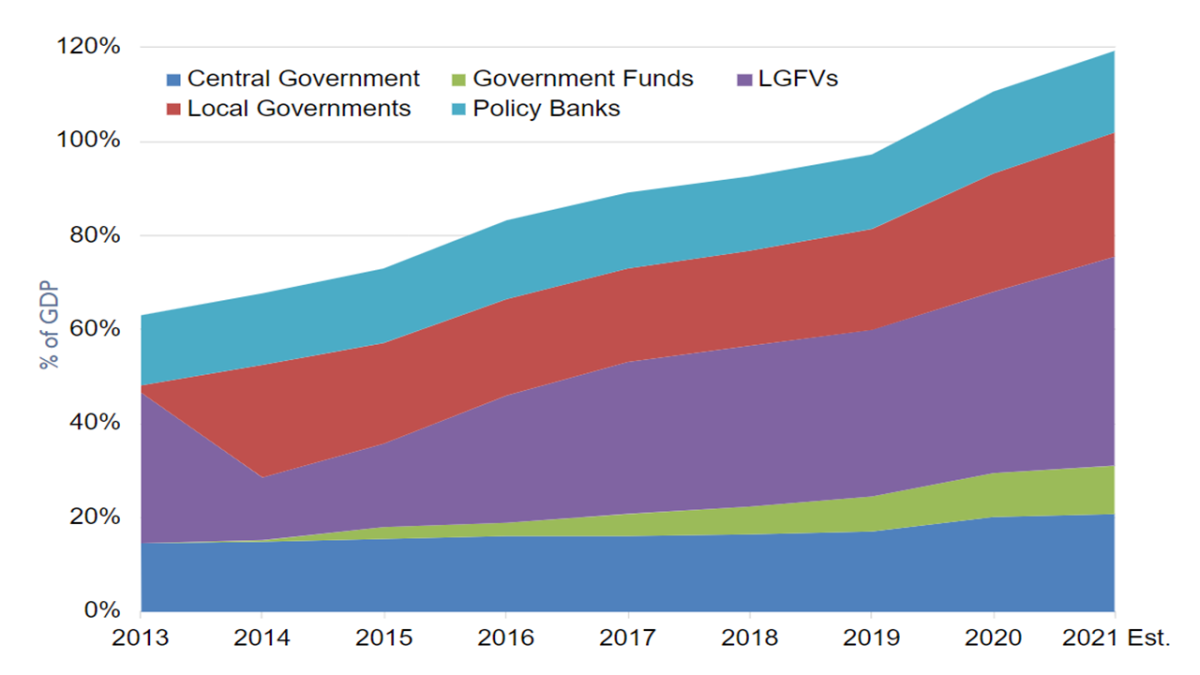

This issues insofar as there may be an ongoing notion that the true property and infrastructure over-investments as a progress lever have depleted. Not solely due to the degrees of indebtedness – significantly through native authorities financing automobile debt (LGFVs in Determine 8) that adopted its intensive use, but additionally as a result of, on the margin, its returns when it comes to GDP progress confirmed a declining contribution. Clearly, Chinese language authorities are actually selecting to safeguard their economic system from monetary vulnerabilities, even on the value of GDP progress under official targets.

Determine 8 – China’s complete authorities debt, by supply 2013–2021 (Est.)

Development Challenges Forward

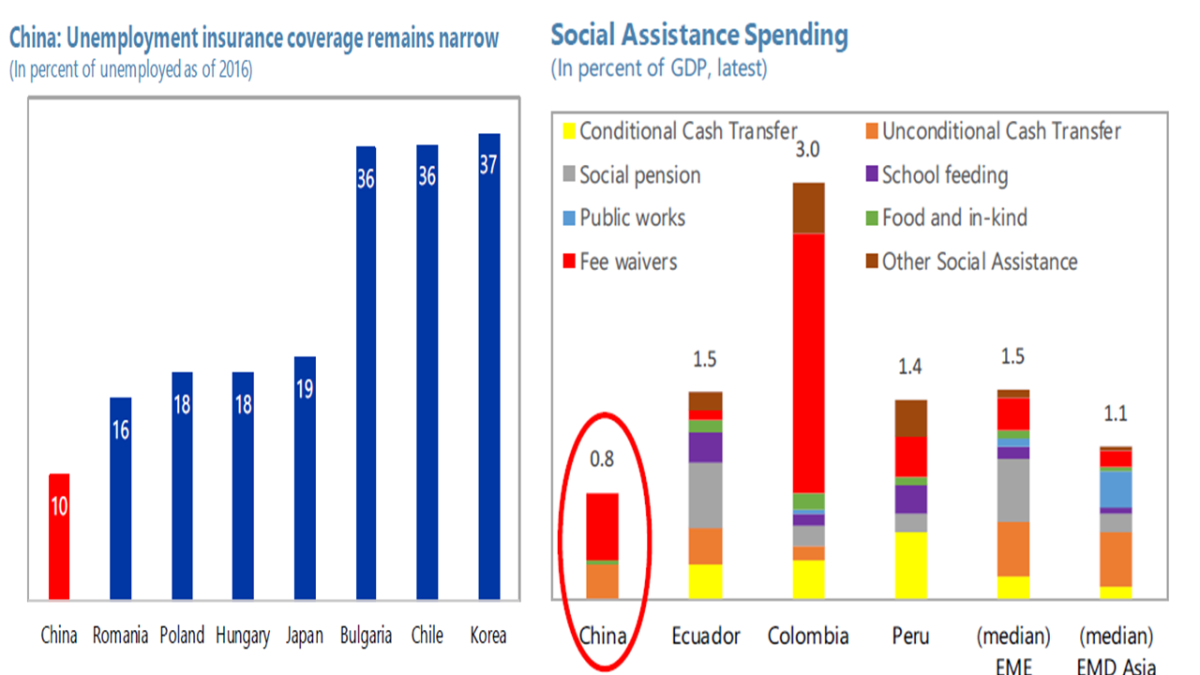

The share of home consumption to GDP stays exceptionally low and that is still a problem for China’s financial rebalancing. Along with the excessive proportion of income in relation to wages, low ranges of public spending on the social security web have led to excessive family financial savings. As depicted on the left-hand panel of Determine 9, the protection of the unemployment insurance coverage system continues to be extraordinarily restricted, offering protection for just one in three individuals within the city labor power and for fewer than one in 5 migrant employees. Protection is even thinner in rural areas. Solely 10 p.c of 23 million unemployed employees obtained advantages in 2016 (IMF, 2020).

Spending on social help and public well being care is low. China’s mixture welfare and well being expenditures are solely about 3.5 p.c of GDP, a lot lower than the common of greater than 6 p.c of GDP of its rising market friends (Determine 9, right-hand panel).

Determine 9 – Unemployment insurance coverage protection and social help spending

One other problem can be in climbing the technological and value-added ladder. Beforehand, to some extent, China resorted to insurance policies of compelled transfers by those that wished to speculate there or the usage of applied sciences with out recognition of mental property. Alternatively, it has on the similar time additionally finished its homework when it comes to investments in training, infrastructure, and many others. to soak up this know-how creatively (Canuto, 2018).

China has now reached the highest of the ladder in lots of sectors, the place “tacit and idiosyncratic” know-how content material should be developed domestically, as it isn’t obtainable just by utilizing or adapting present applied sciences (Canuto, 1995). Moreover, the “new regular” of the worldwide economic system after the pandemic and rising geopolitical dangers because the conflict in Ukraine tends to exhibit an setting much less pleasant for China’s delving into know-how overseas (Canuto, 2022). In precedence sectors, corporations have continued to extend their capital expenditure.

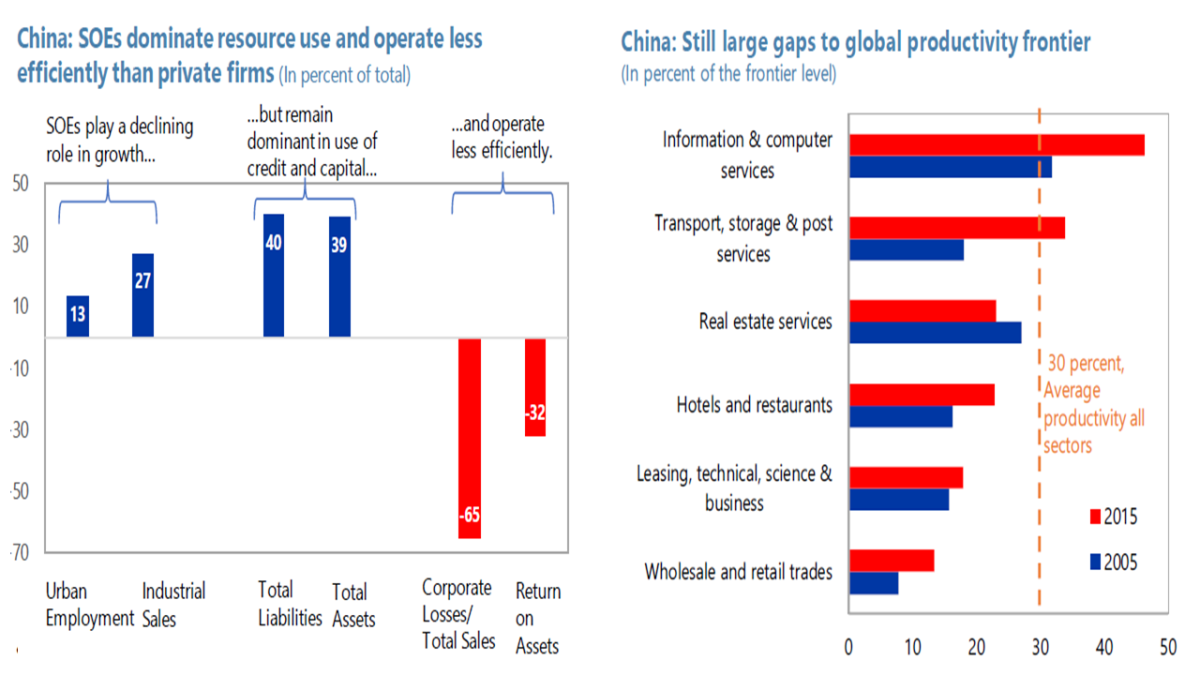

China also needs to resume the rebalancing between private and non-private firms (SOEs and POEs) in service sectors, by which – not by likelihood – Chinese language productiveness stays nicely behind the border in superior nations (Determine 10, right-hand panel).

Determine 10 – China’s rebalancing: SOEs and POEs

Again in 2011 Chinese language authorities referred to a “rebalance between private and non-private sectors” as a part of “rebalancing”. However such rebalance has stalled and progress in reforming SOEs has seen restricted progress. Credit score continues to be preferentially channeled to state companies, which take pleasure in implicit ensures, and competitors between non-public corporations and State-owned enterprises stays uneven in sectors the place these SOEs have been thought to open area. Whereas massive state-owned banks preserve lending to SOEs, infrastructure and actual property investments have been supported by shadow finance.

SOE deleveraging has paused, reflecting, partly, the pandemic disaster and the resort to them to assist progress. That will have been a unprecedented coverage choice. What issues right here is to name consideration to the truth that the efficiency indicators on the left-hand panel of Determine 10 recommend that the absence of serious reform of SOE companies has come at a value when it comes to productiveness and actual returns foregone. In keeping with IMF (2020), even amongst listed corporations, the common productiveness hole between SOEs and personal enterprises throughout sectors in China is about 20 p.c.

China has seen exceptional progress during the last a long time, however common sectoral productiveness but stays at about one third of the worldwide frontier. Productiveness gaps are particularly massive within the companies sector. For instance, enterprise companies productiveness stands at solely 17 p.c of the frontier degree, to a big extent due to excessive entry limitations. Reforms addressing these gaps would come with additional opening non-strategic sectors similar to companies to the entry of recent non-public corporations—each home and international. Eradicating regional regulatory limitations would additionally assist enhance competitors and enhance issue allocation by facilitating agency entry and mobility throughout areas in all sectors.

These productiveness gaps have vital implications for the extent of GDP contemplating the SOE sector’s dominance in the usage of sources. IMF (2020) refers to a employees evaluation suggesting that reforms closing productiveness gaps between SOEs and POEs throughout sectors might elevate output by round 4 p.c over the medium to long run.

Lastly, it’s value recalling the debt legacy of the three earlier waves of overinvestment in housing and infrastructure. Safeguarding towards monetary crashes will imply much less use of them to spice up progress forward.

Backside Line

The trajectory of China’s financial progress will stay sliding towards decrease ranges. Within the coming years, the remainder of the world can now not depend on China as an engine of progress as exuberant because it has been in latest a long time. Given the dimensions acquired by its economic system and its progress charges on the margin it’ll stay, although, as a elementary part of the worldwide financial dynamics.

References

Aasaavari, N. et al (2020). China’s Rebalancing: Alternatives and Challenges for LAC Exporters, IMF Working Paper WP/20/239, November.

Borst, N. (2022). The Stability Sheet Constraints on China’s Financial Stimulus, SEAFARER, August.

Canuto, O. (1995). Competitors and endogenous technological change: an evolutionary mannequin, Revista Brasileira de Economia – RBE, EPGE Brazilian College of Economics and Finance – FGV EPGE (Brazil), vol. 49(1), January.

Canuto, O. (2018). Climbing a tall data ladder, Coverage Heart for the New South, Might 10.

Canuto, O. (2019a). China’s Development Rebalance with Downslide, Coverage Heart for the New South, Coverage Transient PB-19/07, March.

Canuto, O. (2019b). Traps on the Street to Excessive Revenue, Coverage Heart for the New South, Coverage Transient PB-19/14, April.

Canuto, O. (2022). Slowbalization, Newbalization, Not Deglobalization, Coverage Heart for the New South, June 1.

Gatley, T. (2022). July 14th webinar: China, Gavekal Analysis.

IMF (2020), Folks’s Republic of China, Employees Report for the 2020 Article IV Session, November.

Qingfen, D. and Ran, Y. (2011). ‘Opening-up to proceed’, Chinadaily, December 12.

Yao, R. (2022). The Development Recession Deepens, Gavekal Dragonomics, August 11.

Zhang, X. (2022). The Monetary Stress From Property Spreads, Gavekal Dragonomics, July 13.

Otaviano Canuto, based mostly in Washington, D.C, is a senior fellow on the Coverage Heart for the New South, a professorial lecturer of worldwide affairs on the Elliott College of Worldwide Affairs – George Washington College, a nonresident senior fellow at Brookings Establishment, a professor affiliate at UM6P, and principal at Heart for Macroeconomics and Improvement. He’s a former vice-president and a former govt director on the World Financial institution, a former govt director on the Worldwide Financial Fund, and a former vice-president on the Inter-American Improvement Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics on the College of São Paulo and the College of Campinas, Brazil.

[ad_2]