[ad_1]

Forthcoming as a Coverage Paper on the Coverage Heart for the New South

1 Introduction

Inflation as a worldwide phenomenon has triggered the simultaneous tightening of financial and monetary insurance policies internationally. Consequently, world financial development projections for 2022 and 2023 have been revised downward. As inflation charges will come down solely regularly, given the worth stickiness of their core parts, the world faces a scenario of ‘stagflation’—a mixture of serious inflation and low or unfavourable gross home product (GDP) development.

On this briefing, we assess how this world stagflation episode would possibly evolve: in direction of a comfortable touchdown, a pointy downturn, or a deep recession (borrowing these eventualities from a September 2022 World Financial institution report; see Guénette et al, 2022). Because the evolution of the scenario will rely on how briskly inflation drops in response to financial deceleration, we body our response by way of assessing the shifts in main economies’ Phillips curves, which illustrate the connection between inflation and unemployment.

Phillips curve shifts may also mirror the cross-border spillovers of country-specific coverage selections. Moreover, the sudden abrupt deterioration of monetary situations might trigger further Phillips curve motion.

Part 2 considers {that a} world recession—world GDP rising extra slowly than the inhabitants, and thereby world per-capita GDP shrinking—is a robust chance. The mix of financial slowdown and inflation will likely be totally different in numerous international locations however will likely be a standard function.

Part 3 revisits the rationale behind Phillips Curve, i.e., the dilemma between inflation and unemployment confronted by policymakers. We examine the underpinnings of the inflation/unemployment trade-off as they had been within the 1970-Nineteen Eighties, through the ‘nice moderation’, and now after the right storm provoked by the pandemic and the battle in Ukraine. We propose that finally the prognosis for the worldwide economic system will rely on the shapes of country-specific Phillips curves after current drifts, whereas additionally being affected by the cross-country spillovers of native coverage choices.

As an instance cross-country interactions, Part 4 summarizes current challenges arising from the robust appreciation of the U.S. greenback relative to different currencies, notably these of different main economies. This may increasingly reinforce the contractionary pressures on the worldwide economic system. In emerging-market and growing international locations (EMDEs), though exchange-rate depreciation has not been as intense as in non-U.S. superior economies, vulnerabilities related to dollar-denominated liabilities might intensify issues.

Lastly, Part 5 units out three eventualities for the worldwide economic system in 2022-2024. We sketch out what a comfortable touchdown, a pointy downturn or a deep recession would possibly seem like.

2 International Financial Coverage Tightening Underway

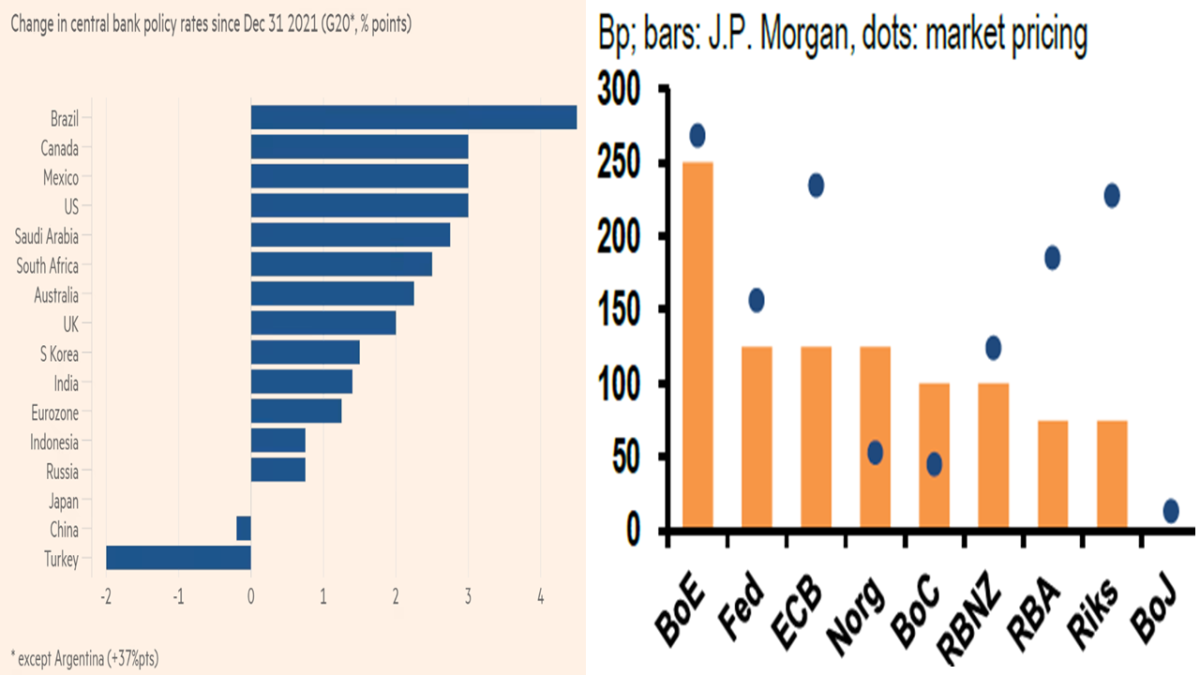

Lately, rate of interest rises have been widespread within the world economic system. The left facet of Determine 1 depicts fundamental rate of interest hikes since 2021, whereas its proper facet reveals market estimates of price hikes in superior economies as much as the second quarter of 2023.

Determine 1: International Financial Coverage Tightening

On September 21, 2022, the US Federal Reserve (Fed) raised the goal for the federal funds price by 75 foundation factors, bringing it into the three% to three.25% vary, along with signaling a noticeably larger degree on the finish of the present climbing cycle.

The Fed has maintained its ‘ahead steering’ that additional price hikes will likely be applicable. It famous that whereas nationwide spending and manufacturing have declined, the rise in employment has been strong. There’s a clear presumption that dangers of wage-price spirals is not going to disappear earlier than the labor market tightness offers solution to looseness and wage moderation.

Particular person projections by the members of the Fed’s Open Market Committee (FOMC)[1], modified considerably in comparison with these issued in June 2022. The September median federal-funds rate of interest projections pointed to a price of 4.4% on the finish of 2022, with solely two remaining FOMC conferences. It seems that committee members anticipate a 75 basis-points improve in November, and one other 50 basis-points improve in December, up from the beforehand anticipated 50 and 25 foundation factors, respectively.

Charges are anticipated to rise a bit of additional in early 2023, with a projected peak of 4.6% based on the median of committee members’ opinions, remaining there till 2024. Fed chairman Jerome Powell mentioned after the September assembly that charges should stay restrictive sufficient to maintain the U.S. economic system working beneath its potential for some time, one thing that will be mandatory to scale back inflation.

This appeared in downward revisions to forecasts for actual GDP development: 0.2% year-on-year in This autumn 2022, adopted by 1.2% and 1.7% in 2023 and 2024, respectively. Progress over the subsequent two years will likely be beneath the estimated potential degree of 1.8%. The Fed has revised its inflation forecast upward via 2024, with inflation not reaching its goal till 2025.

The Fed additionally revised its forecast for the unemployment price, predicting it should rise from 3.7% now to 4.4% by the top of 2023. Traditionally, an increase within the unemployment price of this magnitude over a yr has all the time been adopted by a recession.

In July 2022, we known as into query whether or not two consecutive quarterly unfavourable GDP numbers had been sufficient to state that the U.S. economic system was already in recession (Canuto, 2022a). Along with a discrepancy between unfavourable GDP and constructive gross home revenue (GDI) numbers within the second quarter, the efficiency of the labor market didn’t level to robust deceleration already in course, even when the job market responds to the actual economic system facet with a time lag. The slowdown within the labor market is undoubtedly a part of the aims at present pursued by the financial authorities and displays the precedence given to decreasing inflation.

There’s a common rise in rates of interest, as seen in Determine 1 (although with some exceptions: China, Japan, Turkey). Within the week of the Fed’s September assembly, the central banks of Switzerland, Sweden, Norway, Denmark, Hong Kong (China), the UK, Indonesia, the Philippines, and South Africa hiked charges, because the European Central Financial institution and the Financial institution of Canada had performed within the earlier week. In Brazil, there was no improve, not least as a result of a robust cycle of rate of interest hikes has already occurred since final yr.

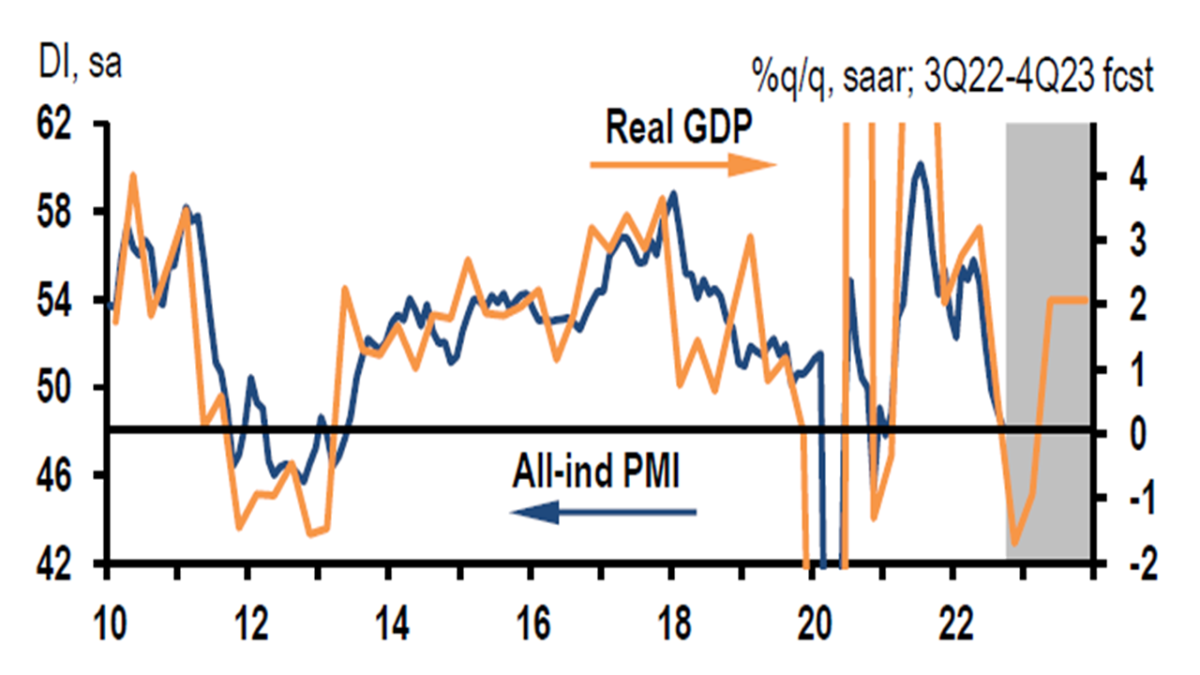

In July 2022, the European Central Financial institution (ECB) hiked rates of interest for the primary time in 11 years. On September 8, it agreed the best improve thus far, by 75 foundation factors. After being at zero or in unfavourable territory for greater than a decade, the European Union now has a price of 0.75%. Regardless of the clear indicators of a slowdown in financial exercise, the ECB’s rate of interest ought to proceed to rise. Within the euro space, industrial manufacturing dropped considerably in July 2022 (Determine 2), on account of the power worth shock, whereas headline inflation projected for September was already near 10% per yr.

Determine 2: Euro-Space All-Trade PMI and Actual GDP

The phenomenon of upper inflation is world in scope, prompting central banks world wide to push their restrictive buttons. With some exceptions, as within the case of China, Russia, Japan, and Turkey (Determine 1, left facet).

There’s an intrinsic problem to the globalized economic system. Every central financial institution appears to be like to its personal nation, deciding financial insurance policies based on what it thinks is critical relating to the native dilemma between unemployment and inflation. However in such an interdependent economic system, the repercussions of any main nation’s choices go far past its borders and again. The chance of suggestions from restrictive financial insurance policies is larger when they’re all responding to a standard inflationary downside.

For varied causes, China’s financial development has been slowing this yr (Canuto, 2022b). The Eurozone additionally seems to be sliding in direction of an financial contraction, as famous above. The mix of upper power costs, U.S. greenback appreciation relative to the euro, China’s development deceleration, and dangers of a second eurozone debt disaster as rates of interest and danger premium on Italian bonds go up, leads one to strongly anticipate recession in Europe. Taking moreover under consideration the slowdown in america, a “world recession” is prone to happen, that’s, a fall in world GDP per capita.

A September report by the World Financial institution – Guénette et al (2022) – famous how, regardless of the worldwide slowdown in development underway, inflation in lots of international locations has risen to the best ranges in many years. Consequently, the worldwide economic system is experiencing a interval of worldwide synchronicity within the tightening of financial and monetary insurance policies, just like the one which preceded the worldwide recession of 1982, whereas world financial development decelerates.

A key variable on this regard would be the evolution of the inflation price, requiring – or not – intensifying the tightening. With inflation hovering across the multi-decade highs in Europe and the US and exercise weakening, the course for financial coverage faces a problem. Financial coverage instructions robust credibility and inflation expectations stay steady in Europe and the US, however one concern is that top inflation itself raises the danger for second-round results on wages. Second spherical results on wage ranges have been noticed within the current previous however not sustained will increase in wage and worth inflation.

It stays to be seen to what extent, within the coming months, worth feedbacks and the inflationary spiral within the largest economies will yield to fiscal and financial tightening with out requiring even stronger doses. In any case, the downward revision of world development projections in 2022 and 2023 has already been exceptional.

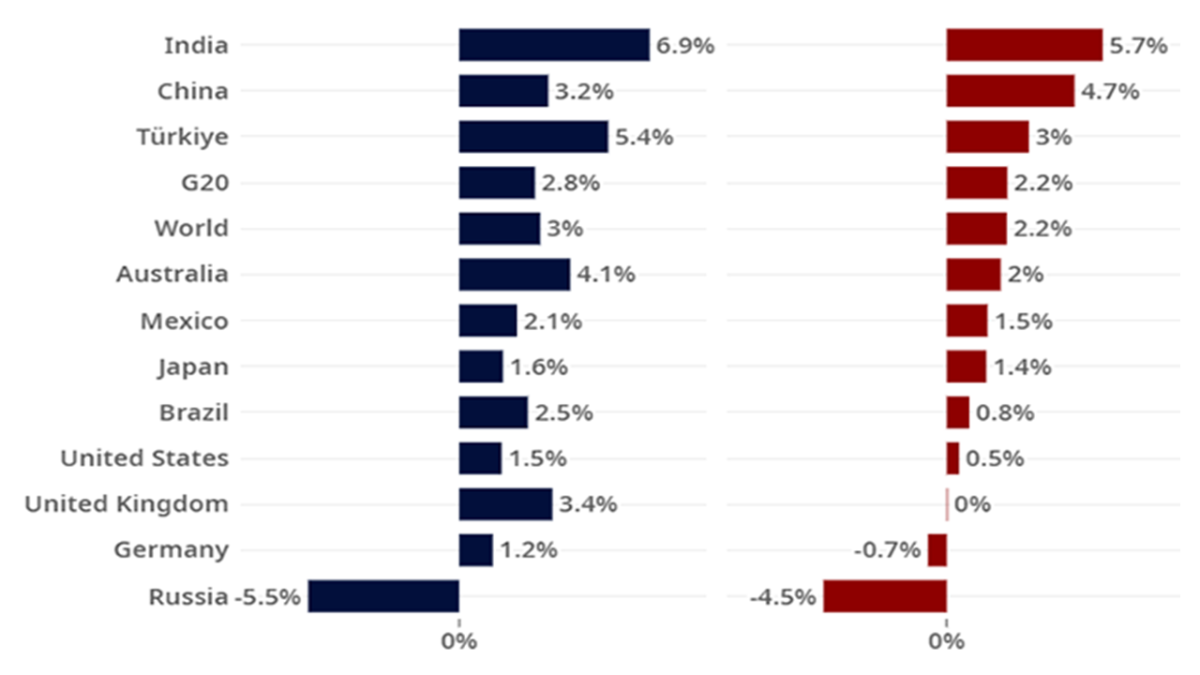

The September 2022 OECD Financial Outlook revised downward its projections of GDP development in 2022 and 2023 (Determine 3). International development is projected to stay subdued within the second half of 2022, earlier than slowing additional in 2023 to an annual price of simply 2.2%. In comparison with the OECD forecasts from December 2021, earlier than Russia’s invasion of Ukraine, world GDP is now projected to be a minimum of $2.8 trillion decrease in 2023.

Determine 3: Actual GDP Progress Projections for 2022 and 2023,

(Chosen international locations, year-over-year, %)

3 Whither the Phillips Curve?

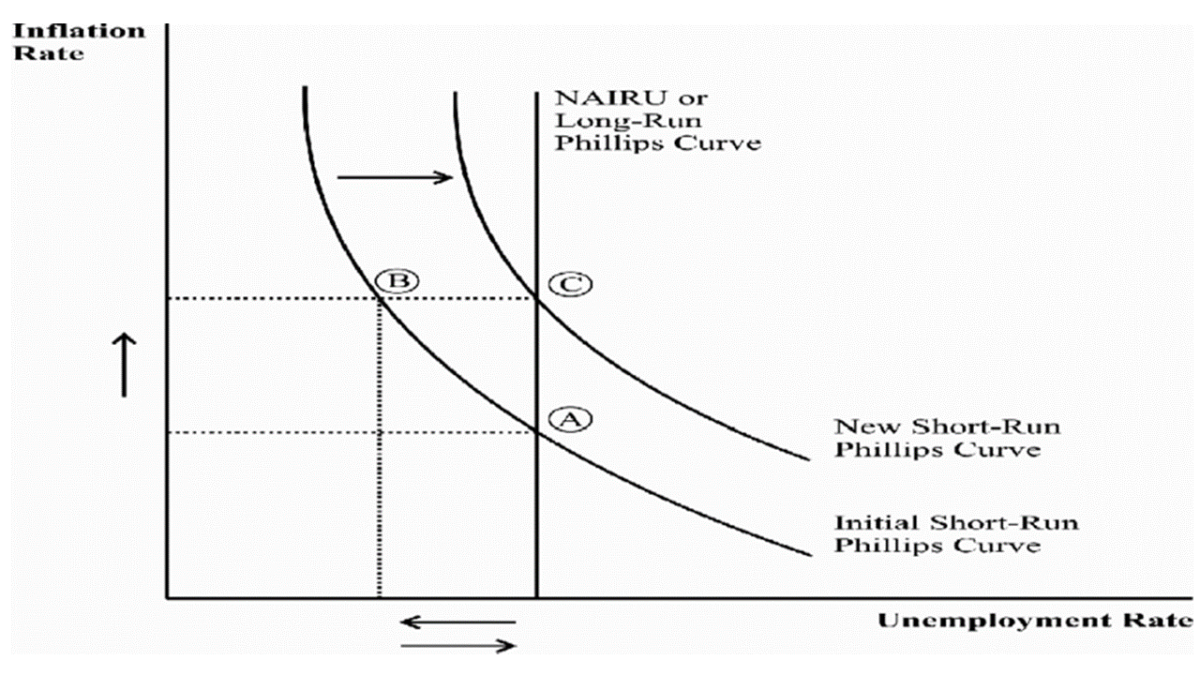

The Phillips curve represents the inverse relationship between inflation charges and the unemployment price and/or the diploma to which a rustic’s potential GDP is successfully being produced. Inflationary pressures improve as unemployment declines and/or the heating up of financial exercise begins to battle with its capability, and vice versa. The curve is called after the British economist A.W. Phillips, whose 1958 paper examined unemployment and wage development in the UK between 1861 and 1957.

The relevance of the Phillips curve for macroeconomic evaluation and financial coverage choices is rapid, as rate of interest choices by central banks rely on the extent of combination demand and, subsequently, on the extent to which potential GDP will likely be under- or over-utilized. The Phillips curve expresses the ‘inflation-unemployment dilemma’.

In precept, at every second in time, there could be a degree or vary of rates of interest at which demand pressures wouldn’t be extreme or could be inadequate in relation to potential GDP, not by probability known as the ‘impartial’ rate of interest, since inflation ranges and unemployment would have a tendency to stay steady. Constantly, there may be the thought that there’s a sure price of unemployment at which inflation stays steady – the non-inflation accelerating price of unemployment (NAIRU).

The connection between unemployment and inflation expressed within the Phillips curve doesn’t essentially stay steady. Along with doable supply-side shocks altering the connection, there are additionally endogenous adjustments when the economic system spends a while working far above – or beneath – the impartial degree.

In conditions of overheating and rising inflation, the expectations of financial brokers in relation to this could cause them to react in ways in which find yourself establishing vicious circles of inflationary suggestions. What’s extra, as soon as that occurs, expectations and behavioral suggestions will solely be reversed if the economic system spends a while beneath its potential, throughout which the inertia of inflation will preserve it going for a while.

That is illustrated by the shift of the preliminary short-run Phillips curve towards a brand new short-run Phillips curve (Determine 4), after a while spent at level B, quite than level A. Stability can then solely be reached with the unemployment price transferring again to NAIRU (level C in Determine 4). Any return to level A will seemingly demand a interval of unemployment charges above NAIRU, coupled with an unwinding of inflation expectations and of wage-price spirals.

Determine 4: The Phillips Curve

The so-called ‘stagflation’ (vital inflation, excessive unemployment, and 0 or low financial development) noticed within the Nineteen Seventies and Nineteen Eighties in america corresponded to being in a zone to the appropriate of level C in Determine 4. The Phillips curve had shifted upwards, and inflation solely declined after a interval of excessive unemployment.

Conversely, the next many years noticed the interval of ‘nice moderation’, the identify given to the interval of low macroeconomic volatility skilled in america from the mid-Nineteen Eighties till the 2007-2008 monetary disaster. The Phillips curve had shifted down.

After the ‘nice recession’ that adopted the worldwide monetary disaster, the shift appeared to have been confirmed. The U.S. economic system took some time to recuperate however ended up going via an extended and regular enlargement for greater than a decade, at charges beneath historic averages, however akin to a time file with out recessions. Unemployment remained low, with a price decrease than the bottom factors of the earlier 50 years, dropping to three.5%.

In the meantime, inflation remained beneath the Federal Reserve’s 2% goal, averaging 1.7% all through the enlargement. The looseness of financial coverage—together with quantitative easing, or the Fed shopping for authorities bonds and mortgages—didn’t have an effect on inflation (Canuto, 2022d).

Two fundamental elements clarify this ‘flattening’ of the Phillips curve. The primary was the anchoring of inflation expectations at low ranges. The second was the chances opened by the globalized economic system: as a substitute of upward pressures on the home costs of merchandise that is likely to be briefly provide, imports might act as absorbers of demand. Within the absence of generalized overheating, globalization might operate as a buffer in opposition to inflation in particular person international locations.

Then got here the rise in inflation with the provision shocks accompanying the pandemic, the invasion of Ukraine, and the “excellent storm” (Canuto, 2022c). From being thought of a short lived phenomenon, accelerated inflation got here to be acknowledged as one thing that isn’t routinely reversible.

This isn’t least as a result of it additionally displays the dimensions of fiscal and financial stimulus in superior economies, with the sharp channeling of demand for items—instead of providers—creating bottlenecks in provide chains and conflicting with provide capacities. As well as, the workforce has contracted, lowering doable employment ranges.

The Phillips curve has shifted. As Gita Gopinath, the IMF’s first deputy managing director, outlined in a presentation on the Federal Reserve’s August 2022 Jackson Gap Financial Symposium, lower than 1 / 4 of a share level of the rise in inflation could be attributed to unemployment falling beneath the ‘pure’ price estimate, or NAIRU (Gopinah, 2022). In any case, there may be now a simultaneous improvement internationally within the tightening of financial and monetary insurance policies, making a worldwide recession seemingly, as we now have mentioned.

And now? The place will the Phillips curve go? Will the connection return to the way it was earlier than the pandemic?

Based on the Institute of Worldwide Finance (Brooks et al, 2022), the impact of the pandemic as a supply of shocks on provide chains appears to have ended, given the stage of normalization of supply instances and the discount of its upward stress on inflation. On the provision facet, nevertheless, there are nonetheless the impacts of the battle in Ukraine on world inflation, particularly in Europe.

Moreover, the post-pandemic job provide will stay troublesome to foretell for a while. There’s additionally the danger that “relative deglobalization” of worth chains undermines the balancing of provide and demand through overseas commerce, quite than home costs (Canuto, 2022e; Canuto et al, 2022).

And on the mixture demand facet? Will the long-term low rates of interest that prevailed within the current previous return, or will the ‘excellent storm’ deliver structural adjustments?

Gopinath instructed that whereas demographics, revenue inequality, and a desire for secure belongings will proceed to maintain charges low, larger debt post-pandemic and inflationary shocks accompanying the power transition (Canuto, 2021c) will work in the wrong way. In flip, it’s troublesome to foretell the place labor provide and productiveness will go.

The Philips curve will preserve transferring. In the meantime, it is usually essential to confirm whether or not the financial adjustment applications underway will likely be efficient in conserving inflationary targets as anchors for expectations. This may increasingly make the distinction by way of which development deceleration situation prevails.

4 U.S. Greenback Appreciation Might Be Contractionary

The current robust appreciation of the U.S. greenback relative to different currencies, notably of different main economies, might reinforce the contractionary stress on the worldwide economic system. In rising market and growing international locations (EMDEs), though exchange-rate depreciation has not been as intense as for non-U.S. superior economies, vulnerabilities related to dollar-denominated liabilities might result in intensified issues.

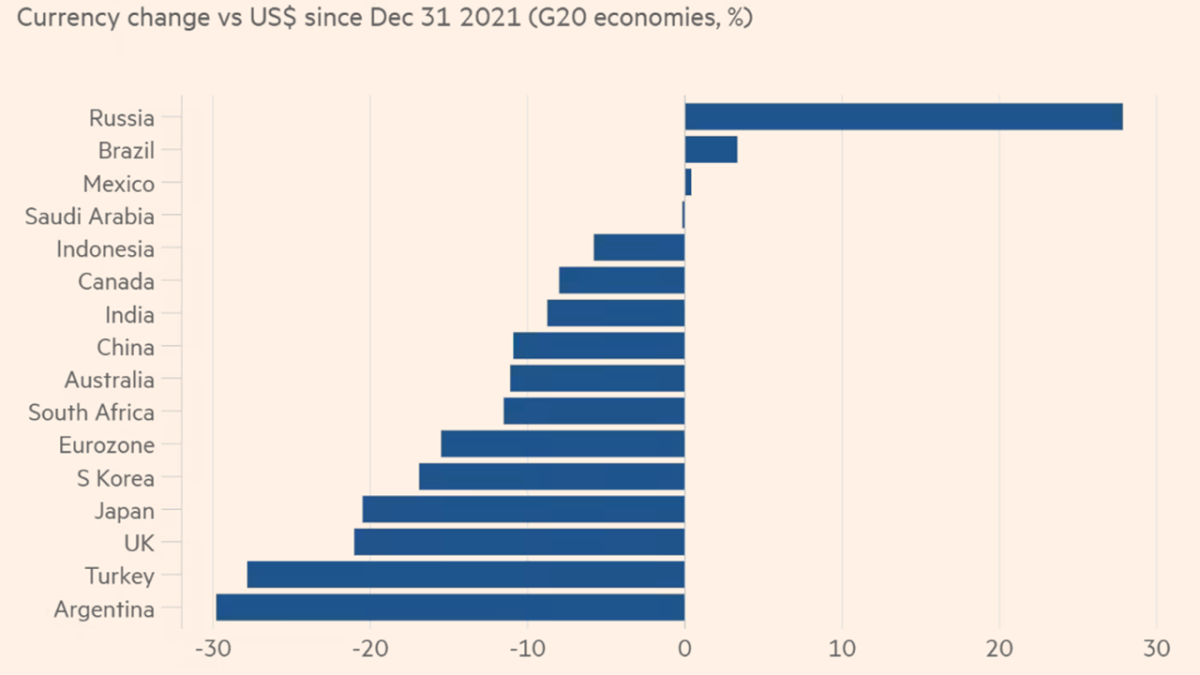

Take the U.S. Greenback Index (DXY), a measure of the worth of the greenback in opposition to six different world currencies[2]. On September 28, the DXY was at its highest degree since Might 2002. In comparison with the start of 2022, the greenback was up 18% in opposition to the euro, and 26% in opposition to each the Japanese yen and British pound. Determine 5 reveals how 20 G20 currencies have to this point in 2022 advanced relative to the U.S. greenback.

Determine 5: G20 Currencies Relative to the U.S. Greenback in 2022

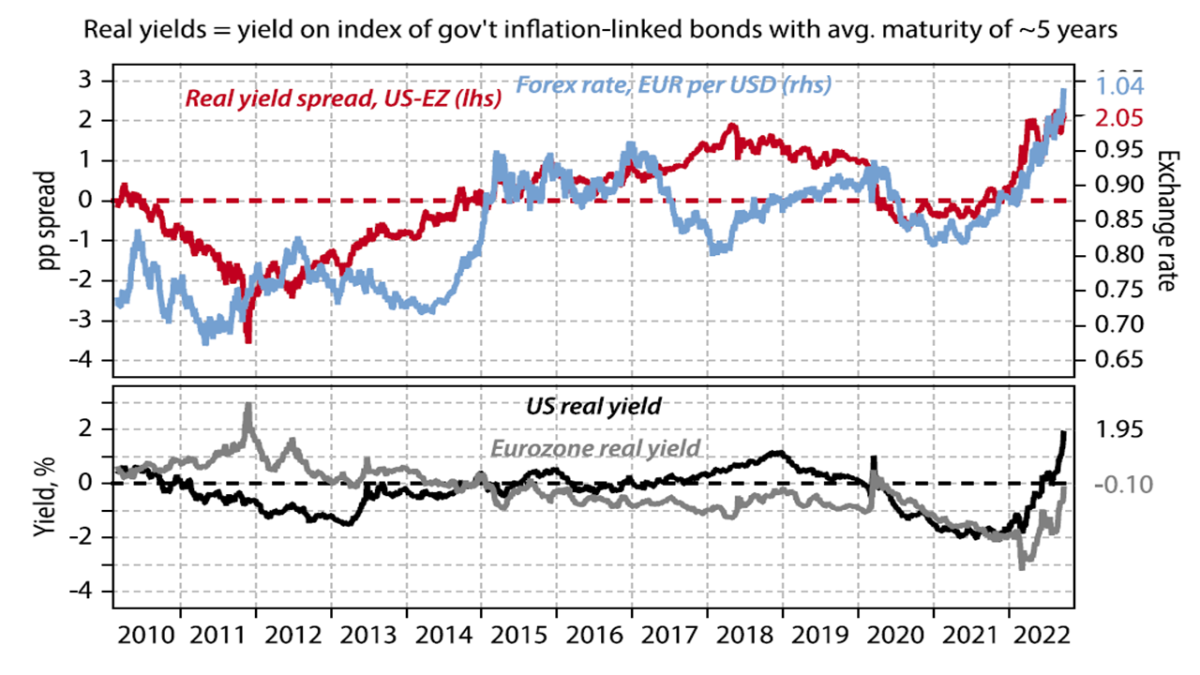

A key further driver of the U.S. greenback appreciation has been the upper yield in actual phrases of U.S. belongings relative to others. Determine 6 reveals the differential in actual yields between the U.S. and the euro space, as measured by yields on five-year inflation-indexed authorities bonds, pairing it with the euro-dollar depreciation. It displays the extra fast rate of interest strikes within the U.S., adopted by market expectations in regards to the Fed’s anti-inflation drive, in comparison with others.

Determine 6: U.S. and Euro Space: Actual Yields and Change Charges

Based on W. Denyer, an identical image could also be constructed extra broadly for the comparability of risk-adjusted charges of return for different fixed-income belongings. Given the heights already attained by the greenback, additional bouts of greenback appreciation would possibly occur provided that the opposite central banks proceed to lag in setting rates of interest and/or the tempo of adjustment by the Fed accelerates even additional. There are additionally all the time, after all, one-off occasions, corresponding to an intense depreciation of the British pound attributable to a proposal for unfunded tax cuts, that in early October was partly reversed.

Some international locations have tried direct interventions in change charges as a substitute of—or as a complement to—lifting home rates of interest. Japan has opted to promote U.S. Treasury bond reserves to attempt to counteract the yen’s change price devaluation in opposition to the greenback. Switzerland additionally mentioned to be contemplating promoting overseas forex to assist the Swiss franc, in addition to elevating rates of interest between conferences of its central financial institution.

The interval after the 2008-2009 world monetary disaster noticed ‘forex wars’, when international locations accused one another of exporting their unemployment issues via vital reductions in home rates of interest and forex devaluation. A ‘reverse forex battle’ might now be rising, because the appreciation of the U.S. greenback exports inflation to others. Clearly, within the absence of some form of new Plaza Accord[3], particular person nation efforts to evade rate of interest changes through direct interventions in change markets can have restricted impact, if the underlying elements resulting in capital flows are usually not altered.

In any case, moreover hurting U.S. multinational corporations’ income from overseas, in addition to rising markets’ dollar-denominated overseas liabilities (Canuto, 2020), a method or one other the U.S. greenback appreciation might result in inflationary shocks in different international locations and, thereby, even tighter financial insurance policies. Suggestions loops of restrictive insurance policies could also be sparked by drastic and sudden U.S. greenback appreciation.

The situation the worldwide economic system will comply with will rely on native combos of inflation stickiness, mandatory financial tightening, and monetary vulnerability. The place Phillips curves have moved to will matter.

5 Three Completely different Close to-Time period Eventualities

For the reason that starting of 2022, a fast deterioration of development prospects, coupled with rising inflation and tightening financing situations, has ignited a debate about the potential for a worldwide recession—a contraction in world per-capita GDP (Canuto, 2022c).

Consensus forecasts for world development in 2022 and 2023 have fallen considerably because the starting of the yr. Though these forecasts don’t level but to a worldwide recession in 2022–2023, Guénette et al (2022) name consideration to the expertise of earlier recessions, highlighting a minimum of two current options that point out a excessive chance of a worldwide recession within the close to future.

First, each world recession since 1970 was preceded by a major weakening of world development within the earlier yr, as has occurred not too long ago. Second, all earlier world recessions coincided with sharp slowdowns or outright recessions in a number of main economies.

Regardless of the present slowdown in world development, inflation has risen to multi-decade highs in lots of international locations. To curb the dangers from persistently excessive inflation, given the context of constrained fiscal area, many international locations are withdrawing financial and monetary assist. The worldwide economic system is in the midst of one of the internationally synchronous episodes of financial and monetary coverage tightening of the previous 5 many years.

These coverage actions are understood as essential to comprise inflationary pressures. However, as we now have mentioned, their mutually compounding results might result in higher impacts than supposed, each by way of tightening monetary situations and in accelerating the expansion slowdown. Whereas such tightening coverage situations weren’t seen on the time of the 1975 world recession, they had been earlier than the 1982 recession.

Guénette et al (2022) suggest three eventualities for the worldwide economic system in 2022-2024 as doable near-term development outcomes. The primary baseline situation follows carefully current consensus forecasts of development and inflation, in addition to market expectations for coverage rates of interest. One might name it a ‘soft-landing’ situation.

In such a baseline situation, world development is forecast to gradual from 2.9% in 2022 to 2.4% in 2023, rising to three% in 2024. The slowdown in 2023 would result in development in per-capita phrases approaching that of the downturn episodes of 1998 and 2012. International commerce development would mirror a broad-based weakening of demand in 2023, earlier than accelerating in 2024.

Progress in superior economies would gradual from 2022 to 2023, earlier than recovering considerably in 2024. In flip, development in rising market and growing economies (EMDEs) would speed up from 2022 to 2024, as world headwinds fade, and the post-pandemic restoration continues.

How about inflation? After peaking at 7.7% in 2022, world headline CPI inflation within the baseline situation would stay excessive relative to the inflation goal into 2023, at 4.6%. Nonetheless, the projection for 2024, at 3.2%, is according to a gradual method to the goal, which is about 2.5% on the world degree in GDP-weighted phrases (common 2% within the U.S.).

Inflation in EMDEs is projected to say no quickly from 9.4% in 2022 to 4.5% in 2024, staying above its combination goal of round 3.5%. The decline in core CPI inflation, which excludes the risky power part, could be extra sluggish. Given this inflation outlook and the anticipated path of coverage charges, short-term rates of interest would stay unfavourable, or close to zero, in actual phrases all through a lot of the projection horizon.

Nonetheless, there’s a chance that the diploma of financial coverage tightening at present anticipated will not be sufficient to revive low inflation rapidly sufficient to quell inflation fears. The second situation—sharp downturn—supposes an upward transfer in inflation expectations, which might result in further synchronous financial coverage tightening by main central banks.

Main central banks in superior economies and EMDEs are then assumed to boost their benchmark coverage charges by a cumulative 100 foundation factors above baseline assumptions over the remainder of 2022 and the top of 2023, deciding to maintain this differential via 2024. On this situation, the worldwide economic system would nonetheless escape a recession in 2023 however would undergo a pointy downturn with out restoring low inflation by the top of the subsequent yr. Whereas headline inflation would proceed its downward trajectory in 2024, it will do it at a slower tempo. The decline in core inflation, then again, could be broadly unchanged relative to the baseline situation, because the upward stress from larger inflation expectations would counterbalance the muted impression of widening output gaps.

Based on model-based projections in Guénette et al (2022), the worldwide economic system would nonetheless escape a recession on this sharp-downturn situation, regardless of present process a worldwide downturn (in per-capita phrases) on par with that in 2001, and worse than these in 1998 and 2012. Superior economies general wouldn’t see a contraction of output in 2023, with development of 0.5%. Nonetheless, the extra tightening of financial coverage would result in so-called ‘technical recessions’, i.e., two consecutive quarters of unfavourable quarter-over-quarter development, in each america and the euro space in 2023. Restoration of exercise on this situation would happen in 2024. Nonetheless, the projected GDP development price of two.7% could be 0.3% beneath the baseline-scenario price.

Within the third situation—world recession—the extra will increase in coverage charges would set off a pointy re-pricing of danger in world monetary markets, leading to a worldwide recession in 2023. As in some earlier experiences, abrupt coverage shifts in main economies would possibly trigger deep world monetary stress, aggravating already heightened macroeconomic vulnerabilities.

Otherwise from the interval of the good moderation, the concentrate on inflation discount would constrain the power of central banks to offer aid to burdened monetary markets, past some eventual focused credit score easing to alleviate acute liquidity shortages in key funding markets, as lenders of final resort. Fiscal coverage can be anticipated to face comparable constraints, stopping governments from implementing large-scale assist measures—notably after the upper public debt left as a legacy of the pandemic (Canuto, 2021a).

The headwinds from the globally synchronous coverage tightening could be compounded by a pointy deterioration of world monetary situations. International GDP development would decline by 1.9% in 2023 and 1% in 2024, in comparison with the figures of the baseline situation. These numbers are corresponding to the 1982 recession, with development slowing to 0.5%. International GDP per capita would contract by 0.4%, according to the 1991 recession, though milder than the 1982 episode when the inhabitants grew quicker.

In any case, the evolution of world output underneath this situation could be inside historic expertise of world recessions over the previous 5 many years. Everlasting output losses relative to pre-pandemic tendencies (Canuto, 2021b) could be higher if the continued world slowdown depicted within the soft-landing situation turns into this third situation.

Subsequently, policymakers should take a slim path. Financial coverage have to be applied on the depth mandatory to revive worth stability, whereas fiscal coverage should take into account medium-term debt sustainability objectives. Globally, policymakers want to face able to handle the potential spillovers from globally synchronous withdrawal of growth-supporting insurance policies.

Finally, policymakers should deal with the dilemmas put earlier than them as depicted in Phillips curves, regardless of the configuration of parameters at present defining their shapes is likely to be. Downward stickiness of inflation charges (demanding or not additional financial coverage tightening) and the evolution of monetary situations (embedding varied doable stress ranges) will outline which situation the worldwide economic system will gravitate in direction of.

An vital ‘recognized unknown’ is whether or not worsening monetary situations will set off a monetary shock by themselves, no matter shapes of Phillips curves. Based on experiences from score businesses and others, combination company and family measures of vulnerabilities at present don’t present the degrees of fragility seen in earlier disaster moments. Many corporates have used the response of authorities to the pandemic through liquidity abundance and low long-term rates of interest, as a window of alternative to increase the length at low value of their liabilities.

Nonetheless, there are those that level to areas of monetary intermediation which have developed a excessive vulnerability to shocks – corresponding to sudden disappearance of liquidity – within the current previous. Chapter 3 of the IMF’s October International Monetary Stability Report approaches how open-end funds, which provide every day redemptions whereas holding illiquid belongings, have acquired a major position in monetary markets. They’re weak to investor runs and asset hearth gross sales that may be triggered by sudden liquidity shocks, as an illustration (IMF, 2022).

As giant banks ceased to behave as market makers because the world monetary disaster and the next voluntary and regulatory restrictions, being changed by non-banking monetary establishments which can be obliged to liquefy belongings upon calls for from the funding facet, sudden disappearance of liquidity has turn out to be extra frequent and doubtlessly extra troublesome (Canuto, 2021d). Together with in authorities bonds markets, as we noticed in U.S. Treasuries in March 2020. Central banks are at present doing “quantitative tightening” and any U-turn on provision of liquidity to markets might sign a weakening of their drive in opposition to inflation.

Housing markets are additionally reeling from the elevation of mortgage charges. The lengthy period of very low rates of interest has additionally generated substantial overvaluation of belongings relative to earnings (Canuto, 2021e). Personal fairness and enterprise capital funds have intensively bloomed.

As rates of interest have entered the on-going upward section, unfavourable surprises might come from varied spots. They could worsen the macroeconomic downturn. The Phillips curve would then are inclined to exhibit larger unemployment charges (under-utilization of capability), whilst inflation charges transfer down.

Forthcoming as a Coverage Paper on the Coverage Heart for the New South

Otaviano Canuto, primarily based in Washington, D.C, is a senior fellow on the Coverage Heart for the New South, a professorial lecturer of worldwide affairs on the Elliott College of Worldwide Affairs – George Washington College, a nonresident senior fellow at Brookings Establishment, a professor affiliate at UM6P, and principal at Heart for Macroeconomics and Improvement. He’s a former vice-president and a former govt director on the World Financial institution, a former govt director on the Worldwide Financial Fund and a former vice-president on the Inter-American Improvement Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics at College of São Paulo and College of Campinas, Brazil.

[1] Consisting of the seven members of the Board of Governors of the Federal Reserve System, the president of the Federal Reserve Financial institution of New York, and 4 of the remaining eleven U.S. Reserve Financial institution presidents; see https://www.federalreserve.gov/monetarypolicy/fomc.htm.

[2] The index’s parts are the euro (58% weight), the Japanese yen (14%), the British pound (12%), the Canadian greenback (9%), the Swedish krona (4%), and the Swiss franc (4%) (Bezek, 2022).

[3] Signed on September 22, 1985, on the Plaza Lodge in New York Metropolis, between France, West Germany, Japan, the UK, and america, to depreciate the U.S. greenback by intervening in forex markets.

[ad_2]