[ad_1]

Boo.

Now that the leap scares are out of the best way, let’s discuss one thing actually scary: being a shareholder of Fiserv (NYSE: FI).

I’m overlaying it for one purpose solely: It’s the worst-performing inventory within the S&P 500 this yr. Almost two-thirds of its market worth has vanished in just some months.

For many who’ve held by means of the drop, it’s been a horror present. However the true query now could be whether or not the frightful fundamentals are lastly priced in.

The inventory had already slid almost 40% yr to this point coming into this week, however the collapse got here on Wednesday when the fintech agency slashed its annual earnings forecast and unveiled a broad government shake-up.

Third quarter outcomes confirmed the pressure. Income missed expectations by greater than 8%, working revenue fell 10% yr over yr to $1.44 billion, and free money circulate fell 28% to $1.33 billion. Adjusted earnings per share dropped 11% to $2.04.

The corporate reduce its full-year earnings per share forecast from a variety of $10.15 to $10.30 to $8.50 to $8.60 – a 16% drop. That despatched shares down 44% in a single day, the steepest fall in firm historical past.

New CEO Mike Lyons referred to as it a “crucial and essential reset.” Translation: Administration uncovered accounting surprises, unrealistic progress assumptions, and weak spot in Argentina.

The corporate is reorganizing underneath a brand new One Fiserv plan, with recent management now steering its two core divisions – Service provider Options and Monetary Options.

Fiserv nonetheless runs the digital “plumbing” of recent finance. It strikes cash and manages funds for banks like Citigroup and Wells Fargo, retailers equivalent to Walmart, and even U.S. authorities businesses.

However buyers don’t purchase pipes; they purchase revenue circulate. And proper now, that circulate seems unsure.

Analysts haven’t been form. Steering cuts, board turnover, and imprecise long-term targets have shaken confidence. BTIG downgraded the inventory, warning of a “laundry record of causes” to not personal it.

Nonetheless, whole capitulation can create alternative. When an organization this central to the funds ecosystem resets expectations, it’s price asking whether or not the pendulum has swung too far.

In spite of everything, The Worth Meter doesn’t care about headlines – solely fundamentals.

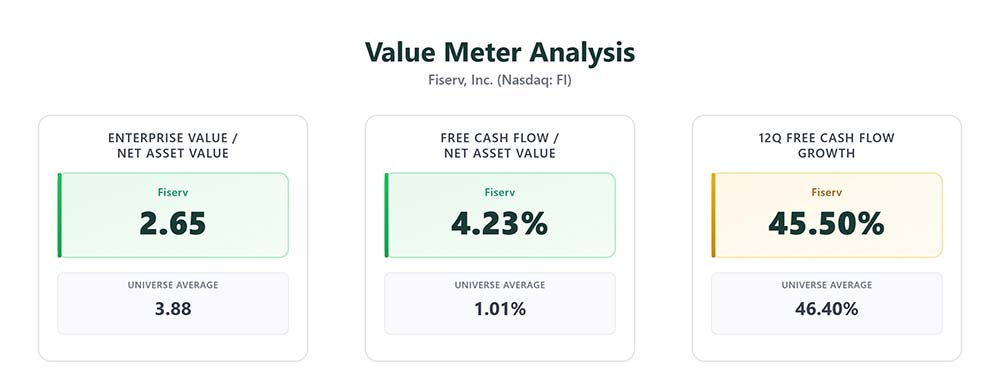

Fiserv’s enterprise value-to-net asset worth (EV/NAV) ratio stands at 2.65, properly beneath the universe common of three.88 – a transparent low cost.

Its free money flow-to-net asset worth (FCF/NAV) is available in at 4.23%, greater than 4 occasions the market’s 1.01% common.

And its 12-quarter free money circulate progress fee of 45.5% almost matches the broad market’s 46.4%, displaying that the engine’s nonetheless operating even after the wreck.

Now, that doesn’t erase the corporate’s issues. Administration nonetheless has to rebuild belief, stabilize margins, and show that the reset wasn’t simply spin. However when a worthwhile infrastructure agency trades at a reduction whereas nonetheless producing wholesome money circulate, the setup will be quietly compelling.

For now, concern dominates the narrative. However that’s normally when worth begins to stir.

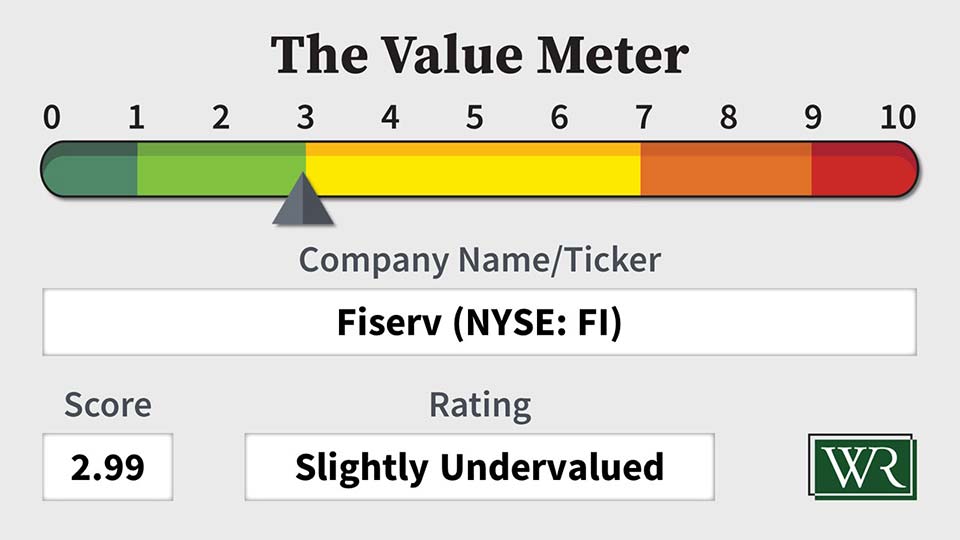

The Worth Meter charges Fiserv as “Barely Undervalued.”

What inventory would you want me to run by means of The Worth Meter subsequent? Put up the ticker image(s) within the feedback part beneath.

[ad_2]