[ad_1]

Forthcoming at Coverage Middle for the New South

The pandemic has hit Latin America onerous and its financial restoration has been slower than in different areas of the world. Along with the legacy of higher public indebtedness, the pandemic left scars on the labor market and the human capital formation of future staff.

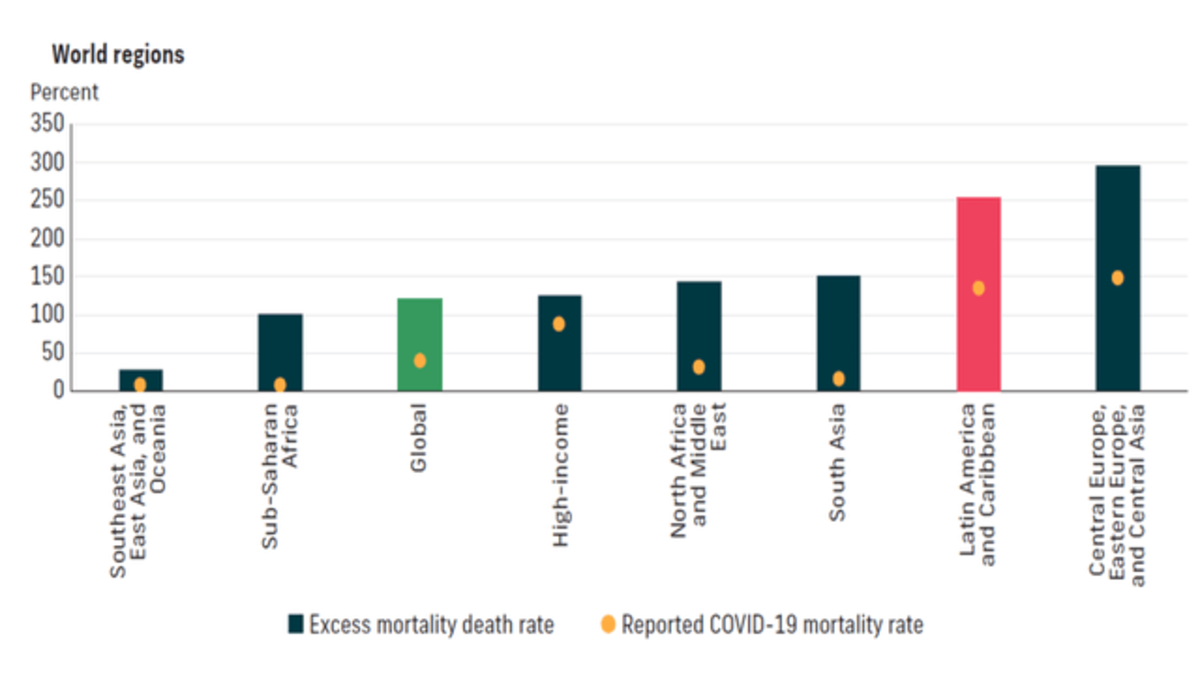

The COVID-19 disaster has receded in Latin America however has left a big toll. Reported deaths from the pandemic are at the moment low and converging to world ranges. The common extra mortality in the course of the pandemic was among the many highest on the earth: double the worldwide common and second solely to Central Europe, Jap Europe, and Central Asia, in keeping with the most recent World Financial institution’s Latin America and the Caribbean Financial Evaluate (Determine 1).

Determine 1 – Extra mortality because of the COVID-19 pandemic in 2020–21 (%)

In most nations within the area, employment and GDP have already returned to pre-pandemic ranges. However, because the World Financial institution report states, progress forecasts for the following few years counsel them to be “resiliently mediocre”. Financial progress isn’t anticipated to exceed the tempo of the 2010s.

The post-pandemic restoration partially reversed the 2020-21 poverty improve. However neither the everlasting losses of gross home product (GDP) in the course of the pandemic shall be recovered, nor have the long-term scars by way of well being, training, and future inequality been erased.

The Russian invasion and the battle in Ukraine additionally had an financial influence on the area, primarily by the shock of commodity costs and consequent will increase in home charges of inflation. Whereas commodity exporters (importers) had optimistic (detrimental) results on their GDPs, by phrases of commerce, all of them needed to face greater meals and vitality inflation, affecting notably the underside of the earnings pyramid, given the load of these things of their consumption basket.

Development charge forecasts for the area this yr have steadily elevated since January – in distinction to downgrades for the remainder of the world due to the battle in Ukraine. The GDP of internet meals and gasoline importers such because the Caribbean and Central American nations was negatively affected. Rising costs for these items have additionally affected households throughout the area. However, the overall improve in commodity costs has been a boon by way of GDP for regional exporters reminiscent of Argentina, Brazil, Chile, Colombia, Ecuador, and Peru.

For commodities as a bunch, 2022 has been a really risky yr. After rising dramatically within the first half, costs retreated within the third quarter, reflecting China’s progress slowdown and the appreciation of the US greenback. The provision shock arising from the battle in Ukraine was adopted by declining demand.

In accordance with the IMF’s World Financial Outlook launched two weeks in the past, tailwinds from commodity costs ought to change route. Within the case of oil costs, futures markets level to a fall within the coming years, after rising 41% in 2022. Russia’s invasion of Ukraine has raised base steel costs, however they’re anticipated to finish 2022 at ranges 5.5 % decrease on common and to say no by an additional 12.0% in 2023. The IMF report forecasts costs of valuable metals to fall extra reasonably: 0.9% in 2022 and an additional 0.6% in 2023.

Meals commodity costs, which additionally surged after Russia invaded Ukraine, fell to pre-war ranges this summer time, ending a two-year rally. Not earlier than including 5 share factors to common meals value inflation charges in 2021, plus an estimate of 6 share factors in 2022 and a pair of share factors in 2023.

The uneven results of upper commodity costs on the area’s inhabitants, primarily undermining the buying energy of the underside of the pyramid, have been – to various levels – accompanied by social switch insurance policies and different varieties of help. The absence of available fiscal house for such use has been a constraint.

The elevated frequency and protection of antagonistic climate occasions, possible already reflecting local weather change, has additionally been one other supply of meals and vitality value shocks. In recent times, extra frequent floods and droughts have affected meals and vitality provides in China, India, Europe, the US, Africa, and Latin America itself. Local weather change, a plague (pandemic), battle, and the upper starvation dangers constituted a “excellent storm”.

Along with the consequences of those three shocks, a fourth supply has include the tightening of worldwide monetary circumstances. Excessive world inflation has been met with tighter financial insurance policies by central banks in superior economies.

Development dynamics shocked a lot of the area positively, favored by the return of companies and employment to pre-pandemic ranges, in addition to exterior circumstances that remained favorable till not too long ago – together with nonetheless excessive commodity costs, nonetheless sturdy exterior demand, and remittances, along with the return of tourism. These had been the explanatory elements behind the upward revisions to progress forecasts for this yr since January.

However tightening world monetary circumstances are pushing in the other way now. The provision and prices of home finance have develop into much less pleasant because the area’s main central banks have raised their rates of interest to manage home inflation. Capital inflows decreased and exterior borrowing prices elevated, resulting from decrease threat urge for food on the a part of traders.

The area is mostly extra resilient to an ongoing monetary-financial shock like this than in earlier instances. Banking programs are more healthy and public stability sheets are typically not as fragile as at different instances previously. The cushion by way of international alternate reserves additionally makes a distinction in lots of instances.

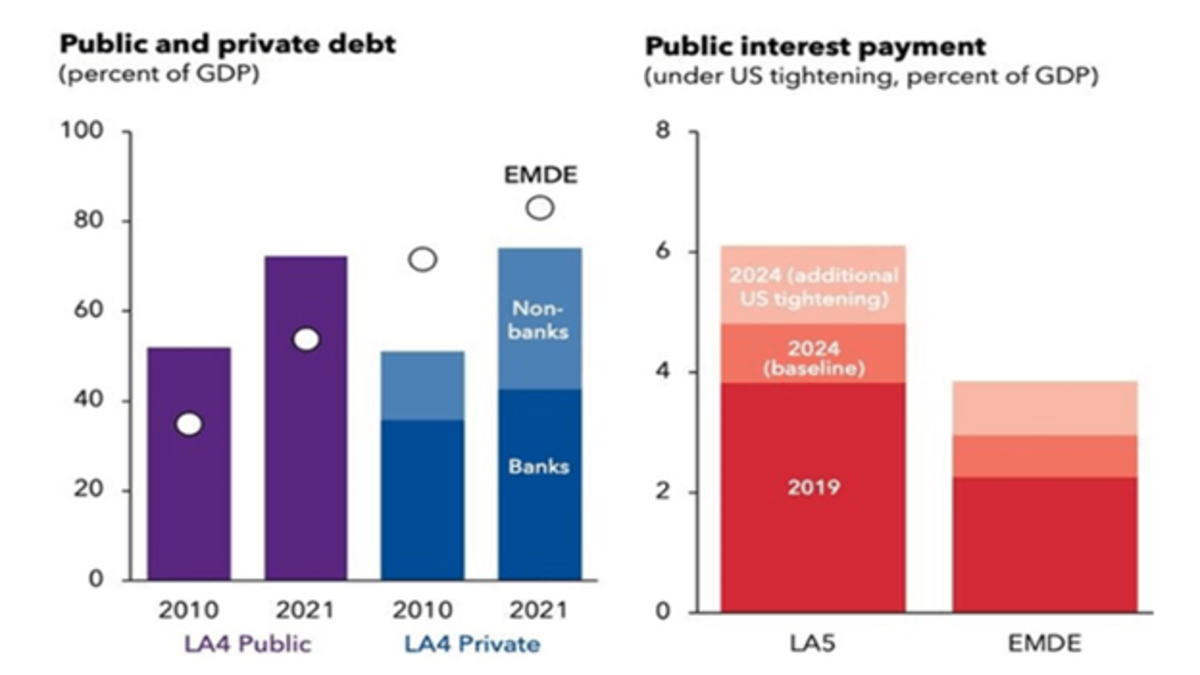

Company debt exterior the banking system is, nonetheless, some extent that deserves consideration. Larger home rates of interest may even tighten circumstances for rolling over public debt (Determine 2).

Determine 2 – Excessive Debt

After the upward surprises in GDP progress in 2022, the anticipated efficiency for subsequent yr is weaker. Whereas the IMF and World Financial institution, respectively, count on the typical GDP progress charge to succeed in 3.5% and three% in 2022, their forecasts go right down to 1.7% and 1.6% in 2023.

Latin America’s restoration after the proper storm shouldn’t be restricted to a easy return to pre-pandemic “mediocre” ranges of output progress. Investments in inexperienced infrastructure, exploring areas of digital connectivity opened by the pandemic, in addition to enhancing the enterprise setting and training can result in an inflection in direction of extra resilient, inclusive, and dynamic progress patterns.

Otaviano Canuto, based mostly in Washington, D.C, is a senior fellow on the Coverage Middle for the New South, a professorial lecturer of worldwide affairs on the Elliott Faculty of Worldwide Affairs – George Washington College, a nonresident senior fellow at Brookings Establishment, a professor affiliate at UM6P, and principal at Middle for Macroeconomics and Growth. He’s a former vice chairman and a former government director on the World Financial institution, a former government director on the Worldwide Financial Fund, and a former vice chairman on the Inter-American Growth Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics on the College of São Paulo and the College of Campinas, Brazil.

[ad_2]