[ad_1]

Coverage Heart for the New South

The beginning of 2022 has been marked by simultaneous indicators of a slowdown in international financial progress, and a reorientation towards tightening of financial insurance policies in superior economies. In its World Financial Prospects report, printed on January 11, the World Financial institution forecast that, after a price of world progress at 5.5% final 12 months, it ought to average to someplace round 4.1% in 2022 and three.2% in 2023..

Along with the consequences of the Omicron COVID-19 variant initially of 2022, much less fiscal help and lingering provide chain disruptions and bottlenecks level to a slowdown. In the USA, enterprise and client confidence surveys in December already advised a touchdown in progress.

For China, the World Financial institution, expects GDP progress of 5.1% this 12 months, under the 8% estimated for 2021. Along with attainable restrictions on mobility due to China’s ‘zero COVID’ method, the adjustment within the property sector will include client spending and residential funding.

Whereas superior economies and China scale back their paces of growth, central banks are on a tightening path—aside from in China. The Federal Open Market Committee (FOMC) of the Federal Reserve Financial institution (Fed) of the USA meets on 25-26 January. However the reorientation of its financial coverage since October has been clear within the minutes of its conferences since then, and in statements by its president Jerome Powell. Along with a U.S. unemployment price under 4%, client value inflation ended the 12 months at 7%, a stage not seen because the early Eighties. Treating it as a ‘transitory’ phenomenon has been deserted by the Fed.

Whereas the September 2021 FOMC assembly advised an rate of interest hike this 12 months, the stakes are actually three or 4 will increase. As well as, the tip of the Fed’s bond-buying program was introduced ahead to March, whereas Jerome Powell telegraphed that the Fed’s stability sheet discount would start before anticipated, maybe as early as mid-year.

After rate of interest hikes in the UK, Norway, and New Zealand, the identical is anticipated in Canada later this month. Strikes in the identical route by the European Central Financial institution and Sweden are actually anticipated for early 2023.

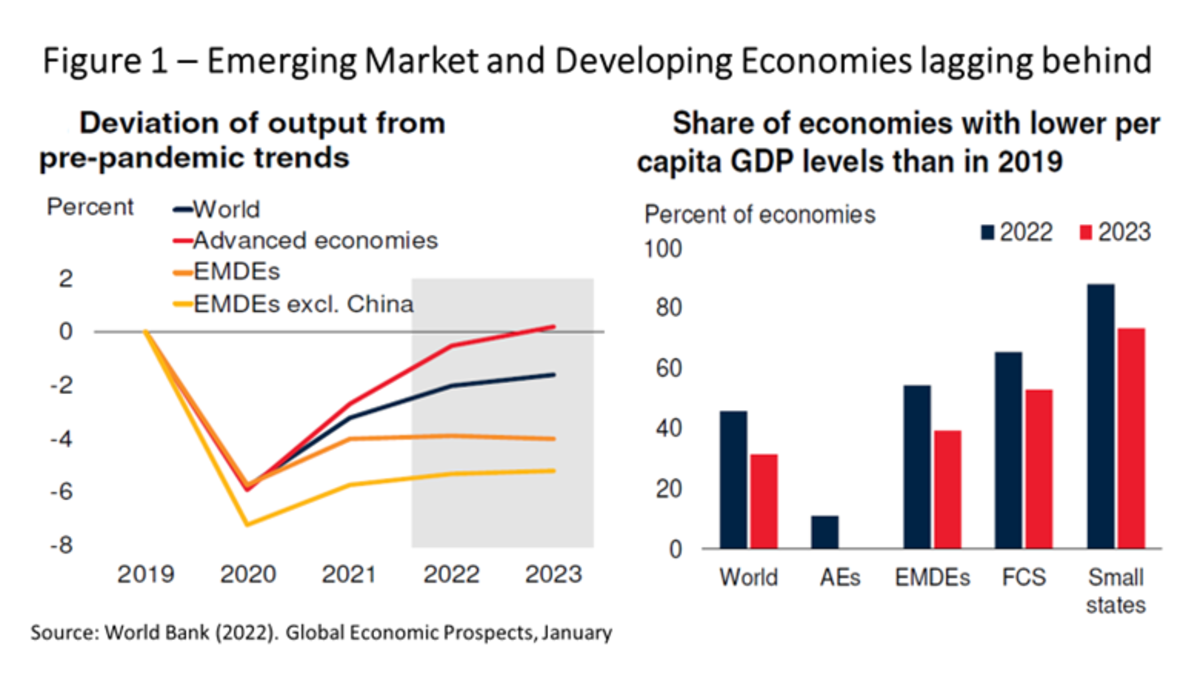

That is the exterior situation confronted by rising and creating economies, whose sluggish restoration from the pandemic is anticipated to proceed. The World Financial institution doesn’t count on their return to pre-pandemic GDP and funding tendencies in 2022-23 (Determine 1).

Excessive inflation charges and public indebtedness throughout the pandemic are constraining the adoption of expansive fiscal and financial insurance policies in rising and creating international locations. Not coincidentally, greater rates of interest and the downward revision of fiscal help are seen generally. The query is whether or not the expansion slowdown with tightening monetary circumstances in superior economies is more likely to be disastrous for rising markets, with touchdown turning into a tough one of their case.

Tightening exterior monetary circumstances will doubtlessly intensify the challenges dealing with rising market policymakers. For rising market economies which can be at present present process vital home inflationary pressures, the danger of extra pass-through pressures from forex depreciations after markets embed greater U.S. rates of interest will likely be key in setting financial coverage. On this case, whereas financial coverage tightening cycles started in 2021 in Brazil, Mexico, and Russia, following inflation charges shifting above their targets, central banks in India and Indonesia maintained an accommodative stance, given low home core-inflation charges.

Professional-cyclicality of capital flows would even be an element impacting these international locations. Rising market economies with a excessive share of international participation in home capital markets and extra open monetary sectors are weak to the volatility of such flows. Central banks in these international locations could also be compelled to tighten financial coverage past what could be ample from a progress perspective. South Africa and Mexico are such potential instances. In instances of economic markets largely domestically funded—as it’s at present in India, Brazil, and Malaysia—the vulnerability to capital outflows driving substantial forex depreciation is decrease.

Nonetheless, the reply to the query in regards to the nature of the touchdown dealing with rising market economies will in the end depend upon how aggressively the financial coverage reorientation in superior economies takes place. . A number of components favor such a situation.

First, there has not been a big influx of international capital into rising market economies within the latest previous. Jonathan Fortun, within the Institute of Worldwide Finance’s (IIF) January 10 Capital Flows Tracker, advised that there has already been a “sudden cease” in such flows, albeit with nice differentiation amongst rising markets. One could count on that there could be no exterior sources to flee massively within the occasion of a gradual rise in exterior rates of interest.

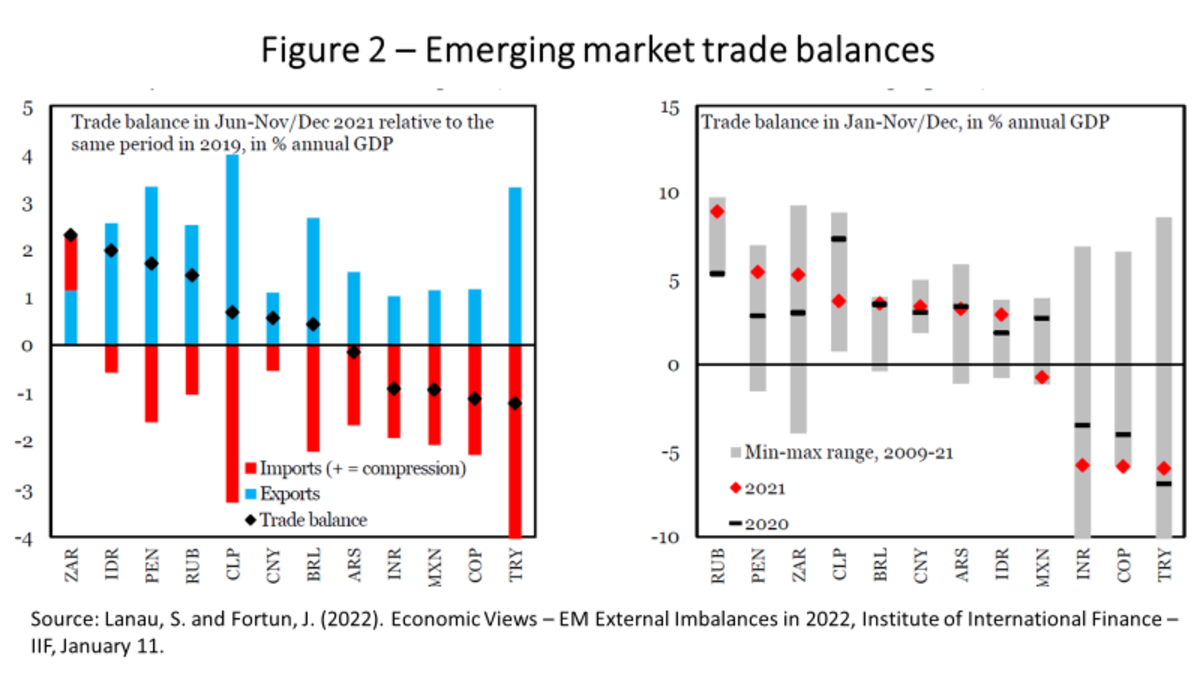

Sergi Lanau and Jonathan Fortun, from the IIF, additionally highlighted that emerging-market present account deficits have been remarkably low or nil within the final two years. Determine 2 illustrates that by displaying commerce imbalances. Within the case of Latin America, international reserves elevated in 2021, following the reinforcement of liquidity buffers began within the second half of 2020, along with the improve in Particular Drawing Rights (SDRs) permitted by the IMF in the course of final 12 months.

What about alternate charges? Are they at ranges of overvaluation that make them weak to sudden and catastrophic devaluations? Right here Robin Brooks, Jonathan Fortun, and Jack Pingle, from the IIF, recommend a extra heterogeneous image: though most rising currencies have skilled actual devaluation within the final ten years, there’s enormous differentiation, with some now exhibiting sharp devaluation and others overvaluation.

Within the case of Brazil, for instance, they estimate a level of round 20% of extra devaluation of its native forex under what could be anticipated from its fundamentals, comparable to present account balances and shares of international belongings and liabilities. The non-return of the alternate price to pre-pandemic ranges contributed to Brazilian inflation ending 2021 in double digits—on high of meals and vitality shocks. In any case, in Brazil and different rising international locations with out alternate overvaluation, a excessive likelihood of dramatic alternate price changes is just not foreseen … supplied that, in flip, the reorientation of financial coverage in superior international locations additionally doesn’t tackle dramatic contours.

Thus, we keep the situation advised final July. Besides within the case of drastic financial changes in superior economies, one should concentrate on home components to know the weaker efficiency of rising markets within the instant future, as depicted in Determine 1.

Otaviano Canuto, based mostly in Washington, D.C, is a senior fellow on the Coverage Heart for the New South, a professorial lecturer of worldwide affairs on the Elliott College of Worldwide Affairs – George Washington College, a nonresident senior fellow at Brookings Establishment, a professor affiliate at UM6P, and principal at Heart for Macroeconomics and Growth. He’s a former vice-president and a former government director on the World Financial institution, a former government director on the Worldwide Financial Fund and a former vice-president on the Inter-American Growth Financial institution. He’s additionally a former deputy minister for worldwide affairs at Brazil’s Ministry of Finance and a former professor of economics at College of São Paulo and College of Campinas, Brazil.

[ad_2]