[ad_1]

Inventory Market Outlook coming into the Week of December 14th = Uptrend

ANALYSIS

The inventory market outlook exhibits an uptrend, however shares have struggled to make a lot progress over the previous two weeks.

The S&P500 ( $SPX ) misplaced 0.6% final week. The index sits 1% above the 50-day transferring common and ~10% above the 200-day transferring common.

No change within the indicators once more this week; nonetheless ready for institutional exercise to substantiate the most recent rally try. It’s value noting that we’re exterior the perfect window for a follow-through day (4-7 days after the preliminary reversal). Wednesday regarded prefer it had an opportunity, however didn’t handle to maneuver greater than 1%. In the course of the wait, the market picked up 4 distribution days, which isn’t very promising.

SPX Worth & Quantity Chart for Dec 14 2025

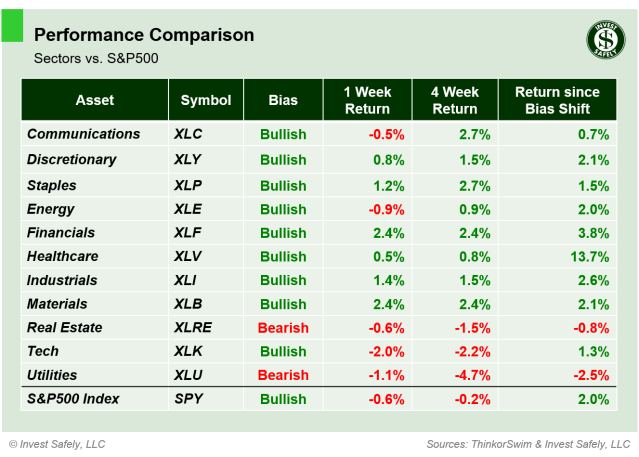

PERFORMANCE COMPARISONS

Financials and Supplies ( $XLF & $XLB ) broke out final week. Expertise ( $XLK ) led the to draw back on AI-related worries. Staples and Supplies ( $XLP & $XLB ) returned to bullish bias from Impartial.

S&P Sector Efficiency from Week 50 of 2025

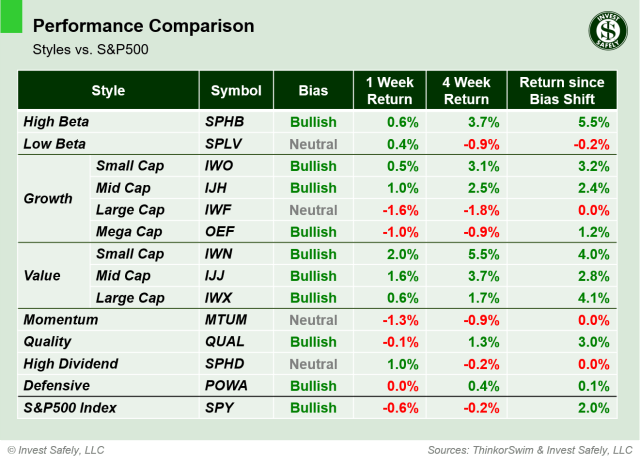

The Small Cap Worth ( $IWN ) investing type was the most important gainer. Massive Cap Progress ( $IWF ) was the most important loser, once more because of AI worries. In a reversal of final week’s modifications, Massive Cap Progress and Momentum ( $IWF & $MTUM ) shifted again to impartial bias; Low Beta and Excessive Dividend ( $SPLV & $SPHD ) kinds moved as much as impartial from bearish.

Sector Fashion Efficiency from Week 50 of 2025

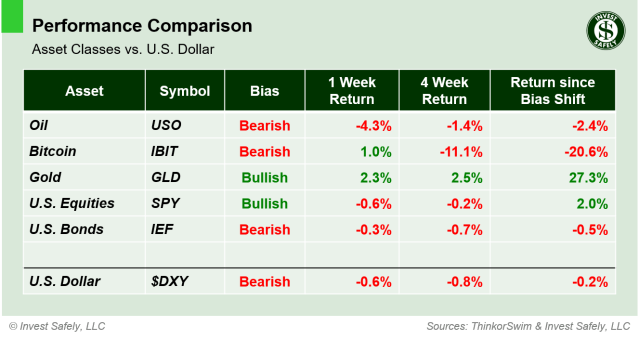

Oil ( $USO ) was the worst asset class final week, giving again a lot of the prior week’s enchancment. Gold ( $GLD ) underperformed. Oil, U.S. Bonds and the U.S. greenback ( $USO, $IEF, $DXY ) all moved to bearish bias.

Asset Class Efficiency from Week 50 2025

COMMENTARY

The FOMC the in a single day rate of interest by 0.25%. No shock there. In addition they introduced the “buy of shorter-term Treasury securities, as wanted, to keep up an ample provide of reserves”. Some speaking heads say that is quantitative easing, however that’s not fairly proper.

Throughout quantitative tightening, which simply ended, the Fed decreased its stability sheet by $2.4 trillion {dollars}. Now, they’ll let the stability sheet develop, as wanted, to make sure our monetary plumbing operates easily. That is mainly the coverage that was in place previous to the Nice Recession. So it’s “easing” within the sense they’re shifting from tightening to sustaining. However don’t have any illusions; if/when the financial system/jobs weaken sufficient, the following spherical of QE will probably be unleashed in spectacular trend.

A number of macro tickers have moved forwards and backwards between bias classes over the previous 2 weeks, which might make for pissed off buyers. Given the dearth of affirmation from institutional exercise, it pays to attend for a affirmation earlier than scaling up any positions.

Trying forward, a giant week of macroeconomic information is on faucet. On Tuesday, we get the primary NFP report for the reason that authorities shutdown, together with October retail gross sales. The market will get an opportunity to digest these numbers Wednesday, earlier than the November CPI launch Thursday. Exiting residence gross sales for November hits the wire Friday.

It’s additionally a quadruple witching day; the ultimate choices expiration of the yr, in addition to the roll-over of fairness futures contracts.

Greatest to Your Week!

P.S. In case you discover this analysis useful, please inform a pal.

In case you don’t, inform an enemy.

Sources: Bloomberg, CNBC, Federal Reserve Financial institution of St. Louis, Hedgeye, Stockcharts.com, TradingEconomics.com, U.S. Bureau of Financial Evaluation, U.S. Bureau of Labor Statistics, TradingEconomics.com

Make investments Safely, LLC is an unbiased funding analysis and on-line monetary media firm. Use of Make investments Safely, LLC and every other merchandise out there by means of invest-safely.com is topic to our Phrases of Service and Privateness Coverage.

Not a advice to purchase or promote any safety

[ad_2]