[ad_1]

Inventory Market Outlook coming into the Week of November twenty third = Downtrend

ANALYSIS

The inventory market outlook shifted to a downtrend final Monday, placing equities right into a correction after a acquire of greater than 20% from the April lows.

The S&P500 ( $SPX ) fell 1.9% final week. The index sits ~2% beneath the 50-day transferring common and ~7% above the 200-day transferring common.

The ADX is bearish. Institutional promoting ramped up, including 3 distribution days to the depend. But it surely was Monday’s excessive quantity transfer by means of the 50-day transferring common that shifted the indicator to bearish and the outlook to a downtrend.

SPX Value & Quantity Chart for Nov 23 2025

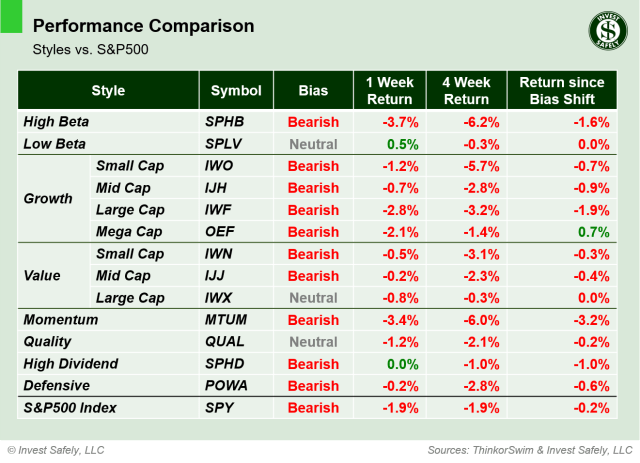

PERFORMANCE COMPARISONS

Healthcare ( $XLV ) led sectors larger for the third straight week; the one sector exhibiting any actual resilience. Power ( $XLE ) is the opposite bullish sector, nevertheless it’s nonetheless discovering its footing. Expertise ( $XLK ) underperformed considerably and dropped to bearish bias. Utilities ( $XLU ) eased again to impartial.

S&P Sector Efficiency from Week 47 of 2025

Low Beta ( $SPLV ) outperformed different sector kinds, however nonetheless misplaced steam through the week and moved to impartial bias. Momentum ( $MTUM ) led to the draw back. Excessive Beta, Giant and Mega Cap Progress ( $SPHB, $IWF, $OEF ) moved to bearish bias; Giant Cap Worth and High quality ( $IWX, $QUAL ) moved to impartial.

Sector Type Efficiency from Week 47 of 2025

Bonds ( $IEF ) outperformed final week, however all property have been weaker versus the greenback. The crypto area continues to expertise deleveraging, so no shock that Bitcoin ( $IBIT ) was the laggard once more.

Asset Class Efficiency from Week 47 2025

COMMENTARY

Establishments have been undoubtedly lowering their exposures final week, particularly on Thursday. Market members dumped risk-on performs, such because the Expertise sector, Excessive Beta/Momentum sector kinds, and cryptocurrency property. Excluding crypto, these classes are nonetheless inside 10% of their all time highs, in order that they’re not priced at a reduction simply but ( $SPHB was up ~80% from the April low ).

Final week’s launch of FOMC minutes confirmed that members are divided on the best way to proceed on rates of interest: decrease them to assist the job market or maintain them regular to struggle inflation. Fairness market members have been pricing in a December price lower. A lower than sure lowered that chance, which can have influenced capital flows final week.

Though they’re fewer and farther between nowadays, corrections are regular and truly a welcome facet of investing. After they happen, traders get an opportunity to search out property which can be “really” oversold, or on the very least now not overbought.

Corrections aren’t usually “one and finished”, which means there’s normally a retest after which one other transfer decrease. We noticed this play out earlier within the 12 months, when shares offered off in February, consolidated in March, then bottomed in April. Maybe we right in November, get that Santa Claus rally in December, and backside in January nearer to the 200-day transferring common.

Whatever the narrative, risk-on property are bearish throughout a variety of classes proper now. Whereas there are pockets of energy for short-term performs ( e.g. Healthcare ), you’ll wish to broader participation earlier than making strikes. Or no less than see the Magazine 7 flip round, since they’re so closely weighted inside indexes.

Over the approaching periods, mud off these watchlists, decide corporations with top quality fundamentals with top quality chart patterns, after which search for indicators that establishments are again on the purchase facet: accumulation days ( giant each day strikes larger on rising quantity ) and worth regaining/remaining above key transferring averages ( 21 day and 50 day ).

Subsequent week begins the vacation buying and selling season, with Thursday market closures for thanksgiving within the US. PPI and retail gross sales on Tuesday, Sturdy Items on Wednesday. The Bureau of Financial Evaluation (BEA) initially scheduled PCE for Wednesday, however the launch has been delayed.

Finest to Your Week!

P.S. Should you discover this analysis useful, please inform a good friend.

Should you don’t, inform an enemy.

Sources: Bloomberg, CNBC, Federal Reserve Financial institution of St. Louis, Hedgeye, Stockcharts.com, TradingEconomics.com, U.S. Bureau of Financial Evaluation, U.S. Bureau of Labor Statistics, TradingEconomics.com

Make investments Safely, LLC is an unbiased funding analysis and on-line monetary media firm. Use of Make investments Safely, LLC and another merchandise out there by means of invest-safely.com is topic to our Phrases of Service and Privateness Coverage.

Not a suggestion to purchase or promote any safety

[ad_2]